Passenger Vehicle Telematics Market Size 2024-2028

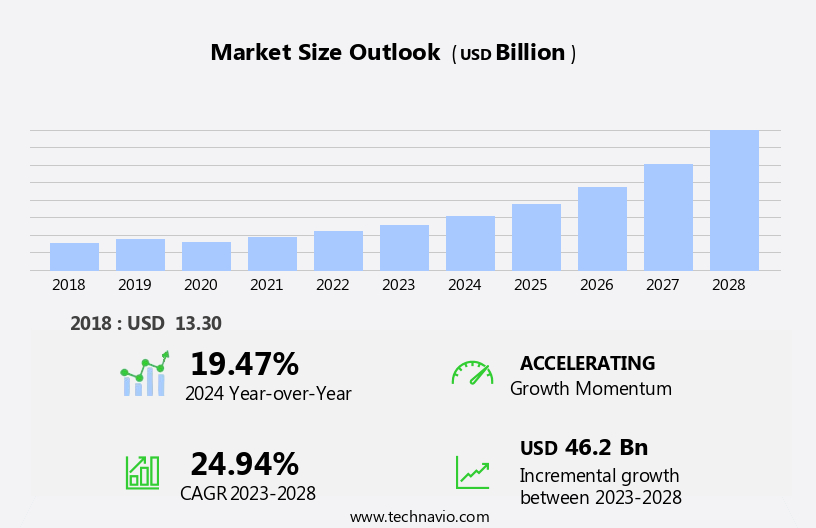

The passenger vehicle telematics market size is forecast to increase by USD 46.2 billion at a CAGR of 24.94% between 2023 and 2028.

- The market is experiencing significant growth, driven by key factors such as the increasing push from Original Equipment Manufacturers (OEMs) to embed telematics systems in vehicles, particularly in BRIC nations. Another trend influencing market expansion is the adoption of video telematics to meticulously monitor driver behavior. Enhanced safety and improved operational efficiency are the primary benefits of this technology. These systems provide real-time alerts for critical situations, such as accidents or engine malfunctions, ensuring prompt response and improved road safety. Furthermore, data security is a critical concern In the telematics industry, necessitating strong cybersecurity measures to protect sensitive information. These factors collectively contribute to the market's growth and innovation In the passenger vehicle telematics sector.

What will be the Size of the Passenger Vehicle Telematics Market During the Forecast Period?

- The market encompasses connected cars and IoT devices that facilitate in-vehicle connectivity and enhance driver safety. Telematics technology also enables fleet managers to optimize service levels through vehicle location tracking, operation monitoring, and dispatching. In addition, it offers client delivery time and driver productivity enhancements, as well as fuel usage insights.

- Moreover, technology advancements, including 5G, GPS tracking, artificial intelligence (AI), and telecommunication, are driving market growth. External sensors and IoT devices provide valuable data, allowing decision-makers to make informed choices regarding vehicle maintenance, driver behavior, and fleet optimization. The integration of AI and telematics systems further enhances safety by predicting potential accidents and offering proactive solutions. The market continues to evolve, with a focus on enhancing passenger safety features and enabling autonomous driving capabilities.

How is this Passenger Vehicle Telematics Industry segmented and which is the largest segment?

The passenger vehicle telematics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Smartphone integration

- Tethered

- Embedded

- Type

- Remote message processing system

- Brake system

- Transmission control system

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- South America

- Middle East and Africa

- APAC

By Product Insights

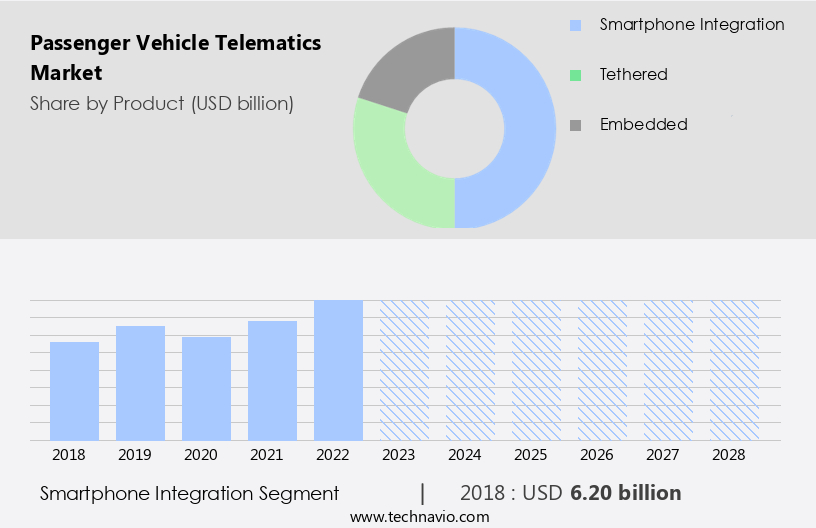

- The smartphone integration segment is estimated to witness significant growth during the forecast period.

The integration of smartphones with automotive telematics is gaining significant traction due to the rising penetration of smartphones and the increasing preference for in-vehicle connectivity. This trend is driving the demand for advanced human-machine interaction (HMI) systems that can seamlessly integrate with smartphones, providing access to a wide range of applications. Ford SYNC 3 AppLink and Toyota Entune are prime examples of successful smartphone integration solutions In the automotive industry. The availability of a strong application base is a crucial factor In the popularity of these systems. Telematics systems, including connected cars, IoT devices, tablets, alerts, and driver safety features, are increasingly being used to enhance road safety, optimize fleet management, and provide real-time vehicle tracking and monitoring.

Fleet operators, insurance companies, and vehicle owners are leveraging these solutions to improve uptime, reduce costs, and ensure better safety performance. The telematics market is expanding to include Intelligent Transportation Systems, autonomous driving, and passenger safety features. Telematics devices and cloud technologies are enabling real-time navigation capabilities, maintenance requirements, and vehicle performance analysis. The market is expected to grow significantly due to the increasing adoption of connected cars, fleet management solutions, and the integration of advanced safety communications, emergency systems, and automatic driver assistance systems. Cybersecurity concerns and logistical strain are key challenges In the market.

Get a glance at the Passenger Vehicle Telematics Industry report of share of various segments Request Free Sample

The smartphone integration segment was valued at USD 6.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

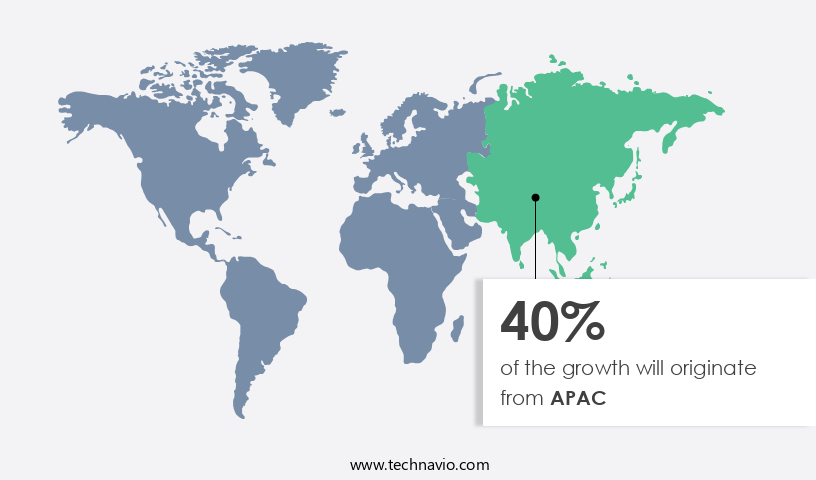

- APAC is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The telematics market in APAC is projected to experience moderate growth, driven by the increasing demand for connected cars and IoT devices in emerging markets like India, China, Malaysia, and Indonesia. With the rise of relatively stable economies, the ownership of passenger vehicles equipped with in-vehicle connectivity, safety communications, emergency systems, and GPS navigation is on the rise. Telematics services, including fleet management and real-time vehicle tracking, are expected to contribute significantly to market revenue growth. Prominent OEMs in APAC are also integrating telematics solutions into their commercial offerings to differentiate their products. These solutions encompass driver safety features, critical situation alerts, and automatic driver assistance systems.

Moreover, the integration of cloud technologies, AI, and external sensors further enhances the capabilities of these systems, catering to the needs of fleet managers, vehicle operators, and insurance companies. Key areas of focus include vehicle location, operation tracking, service levels, dispatching, client delivery times, driver productivity, fuel usage, emissions, navigation, logistics tools, risk assessments, safety performance, maintenance, repairs, and market expansion. Cybersecurity concerns and logistical strain are potential challenges for market growth.

Market Dynamics

Our passenger vehicle telematics market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Passenger Vehicle Telematics Industry?

OEM push for embedded telematics systems in BRIC nations is the key driver of the market.

- The market is witnessing significant growth, driven by the increasing adoption of connected cars and IoT devices. Telematics systems enable in-vehicle connectivity through telecommunication devices, GPS navigation, safety communications, and emergency systems. These advanced technologies offer automatic driver assistance, fleet management solutions, real-time tracking, and remote control monitoring, enhancing driver safety and road safety. Telematics devices provide critical alerts during critical situations, such as vehicle thefts or road accidents. Embedded telematics, which includes factory-fitted telematics equipment, offers the advantage of reliable, 24x7 connectivity. In contrast, tethered and smartphone integration solutions depend on the user's connectivity. Regulatory bodies are encouraging the installation of embedded telematics in passenger vehicles through legislation, such as electronic logging device (ELD) mandates In the US and Canada. Telematics systems offer various benefits, including fleet management, Intelligent Transportation System integration, smartphone applications, and autonomous driving. They provide fleet operators with uptime solutions, vehicle location, operation tracking, service levels, dispatching, client delivery times, driver productivity, fuel usage, emissions, navigation, logistics tools, risk assessments, safety performance, maintenance, repairs, and market expansion opportunities.

- Moreover, telematics platforms offer real-time navigation capabilities, maintenance requirements, vehicle performance, and collision avoidance systems. They also provide infotainment systems, lane keeping assistance, and cruise control. Telematics devices collect and transmit vehicle data, enabling decision-makers to optimize fuel routing, identify maintenance warnings, and recover stolen cars. However, cybersecurity concerns, such as hacking and user data privacy, pose challenges to the telematics market. Market revenue growth is expected due to the increasing adoption of 5G, artificial intelligence (AI), and cloud technologies. The telematics market caters to both business and personal vehicles, with technology advancements influencing consumer purchasing habits. Insurance companies offer insurance plans with automatic crash assistance, digital claim services, and autonomous vehicles. In summary, the market is a dynamic and growing industry, offering various benefits, including improved safety, increased efficiency, and cost-saving opportunities. Market expansion is expected through the adoption of advanced technologies, such as 5G, AI, and cloud technologies, and regulatory mandates encouraging the installation of embedded telematics in passenger vehicles.

What are the market trends shaping the Passenger Vehicle Telematics Industry?

The adoption of video telematics to precisely track driver behavior is the upcoming market trend.

- The market has witnessed significant growth due to the integration of IoT devices, connected cars, and telematics systems in modern vehicles. These advancements enable real-time tracking, fleet management solutions, and driver safety features, including automatic crash assistance, digital claim services, and autonomous vehicles. Telematics devices and cloud technologies facilitate fuel routing optimization, vehicle maintenance warnings, and stolen-car recovery. Fleet operators benefit from uptime solutions, corrective actions, and cost-saving opportunities. Telematics platforms offer safety performance data, risk assessments, and maintenance requirements, enhancing vehicle performance and productivity. Market revenue growth is driven by technology advancements, including 5G, GPS tracking, and artificial intelligence (AI). Connected cars equipped with infotainment systems, real-time navigation capabilities, and driver assistance systems like lane keeping assistance, cruise control, and collision avoidance systems are transforming the automobile telematics market.

- In-vehicle connectivity, such as smartphone applications, digital cockpits, and Intelligent Transportation Systems, further expand the market's scope. However, concerns regarding cybersecurity, user data privacy, and hacking remain significant challenges. Despite these challenges, the telematics market continues to expand its global footprint, catering to both business and personal vehicles. The aftermarket segment and installation, troubleshooting, and periodic replacement services provide opportunities for growth. In summary, the market is poised for growth, driven by advancements in telematics systems, connected cars, and IoT devices. These innovations offer numerous benefits, including improved safety, increased efficiency, and enhanced fleet management solutions. Despite challenges, the market's future looks promising, with continued expansion and the integration of new technologies.

What challenges does the Passenger Vehicle Telematics Industry face during its growth?

Data security in the telematics industry is a key challenge affecting the industry's growth.

- The market is experiencing significant growth due to the increasing integration of IoT devices, connected cars, and in-vehicle connectivity. Telematics systems are becoming an essential component of modern vehicles, offering features such as real-time tracking, automatic driver assistance, and emergency systems. These systems use GPS navigation, safety communications, and telecommunication devices to enhance driver safety and improve road safety. Telematics devices provide fleet management solutions, enabling fleet operators to monitor vehicle location, operation tracking, service levels, dispatching, client delivery times, driver productivity, fuel usage, emissions, navigation, logistics tools, risk assessments, safety performance, maintenance, repairs, and market expansion. Intelligent Transportation Systems and Smartphone Applications are also leveraging telematics data to optimize fuel routing and provide vehicle maintenance warnings. Advancements in technology, including 5G, GPS tracking, and artificial intelligence (AI), are driving the market's growth. Telematics platforms offer features such as lane keeping assistance, cruise control, collision avoidance systems, and infotainment systems with real-time navigation capabilities. However, there are concerns regarding data security, cybersecurity, and hacking, as malware can pass through in-vehicle infotainment systems to other networks, potentially compromising vehicle functions. Telematics devices offer cost-saving opportunities, such as corrective actions for fuel efficiency and maintenance requirements, as well as uptime solutions for vehicle operators.

- Moreover, the market expansion includes the OEM market category, with factory-fitted telematics equipment, and the aftermarket segment, with installation, troubleshooting, periodic replacement, and logistical strain. The market encompasses a global footprint, serving both business and personal vehicles. Telematics systems offer significant benefits, including automatic crash assistance, digital claim services, and autonomous driving technology. Insurance companies are also leveraging telematics data to offer customized insurance plans based on commute risk and driving behavior. In summary, the market is a dynamic and evolving industry, driven by technology advancements and the growing demand for in-vehicle connectivity. The market's growth is fueled by the integration of IoT devices, connected cars, and telematics systems, offering various benefits to fleet operators, vehicle owners, and insurance companies. However, data security and cybersecurity concerns remain significant challenges that must be addressed to ensure the safe and effective implementation of telematics systems.

Exclusive Customer Landscape

The passenger vehicle telematics market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the passenger vehicle telematics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, passenger vehicle telematics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agero Inc.

- Airbiquity Inc.

- AT and T Inc.

- Bridgestone Corp.

- Bynx Ltd.

- Continental AG

- Danaher Corp.

- BorgWarner Inc.

- DXC Technology Co.

- Fleet Complete

- Garmin Ltd.

- OCTO Telematics S.p.A

- Robert Bosch GmbH

- Telefonaktiebolaget LM Ericsson

- Telenav Inc.

- Trimble Inc.

- Valeo SA

- Verizon Communications Inc.

- Visteon Corp.

- Vodafone Group Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of technologies and applications that enable in-vehicle connectivity and data exchange between passenger vehicles and external networks. This market is driven by the increasing demand for enhanced driver safety, improved road safety, and optimized fleet management solutions. Connected cars, equipped with telematics devices, offer real-time alerts for critical situations, enabling quick response to road accidents or other emergencies. These systems provide essential information for fleet operators, enabling them to optimize service levels, dispatching, and client delivery times. In-vehicle connectivity also enhances driver productivity by providing navigation, logistics tools, and fuel usage data. Telematics systems extend beyond the vehicle, integrating with external sensors and cloud technologies to provide comprehensive data on vehicle performance, maintenance requirements, and emissions. This data can be used for risk assessments, safety performance analysis, and cost-saving opportunities. The market for telematics systems is expanding beyond the realm of fleet management and commercial vehicles. Personal vehicles are increasingly adopting these technologies, with automakers integrating telematics systems into their digital cockpits to provide advanced driver assistance systems, real-time navigation capabilities, and infotainment systems. Technology advancements, such as 5G and artificial intelligence (AI), are revolutionizing the market. These technologies enable faster data transfer and processing, allowing for more advanced applications, such as automatic crash assistance, digital claim services, and autonomous vehicles.

However, the market also faces challenges, including cybersecurity concerns and logistical strain. As more data is collected and transmitted, the risk of hacking and data breaches increases. Additionally, the installation, troubleshooting, and periodic replacement of telematics devices can place a strain on fleet operators and vehicle operators. Despite these challenges, the market for telematics systems continues to grow, driven by the increasing demand for safer, more efficient, and more connected vehicles. The market is expected to see significant revenue growth In the coming years, with opportunities for hardware manufacturers, software developers, and service providers. The telematics market is diverse, encompassing a range of applications, from automobile telematics systems for personal vehicles to fleet management solutions for commercial fleets.

Thus, the market is also global in scope, with a growing footprint in both developed and emerging markets. In summary, the telematics market is a dynamic and evolving industry, driven by the increasing demand for safer, more efficient, and more connected vehicles. The market offers opportunities for innovation and growth, as well as challenges related to cybersecurity and logistical strain. As technology continues to advance, the telematics market is poised to transform the way we use and interact with our vehicles.

|

Passenger Vehicle Telematics Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24.94% |

|

Market growth 2024-2028 |

USD 46.2 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

19.47 |

|

Key countries |

China, US, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Passenger Vehicle Telematics Market Research and Growth Report?

- CAGR of the Passenger Vehicle Telematics industry during the forecast period

- Detailed information on factors that will drive the Passenger Vehicle Telematics growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the passenger vehicle telematics market growth of industry companies

We can help! Our analysts can customize this passenger vehicle telematics market research report to meet your requirements.

RIA -

RIA -