Ready To Drink (RTD) Alcoholic Beverages Market Size 2026-2030

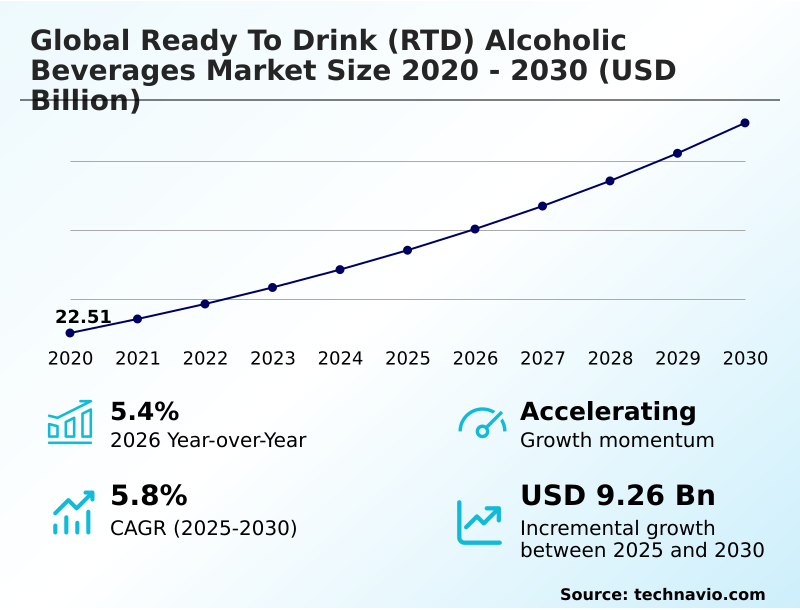

The ready to drink (rtd) alcoholic beverages market size is valued to increase by USD 9.26 billion, at a CAGR of 5.8% from 2025 to 2030. Institutionalization of premiumization and craft oriented spirit infusions will drive the ready to drink (rtd) alcoholic beverages market.

Major Market Trends & Insights

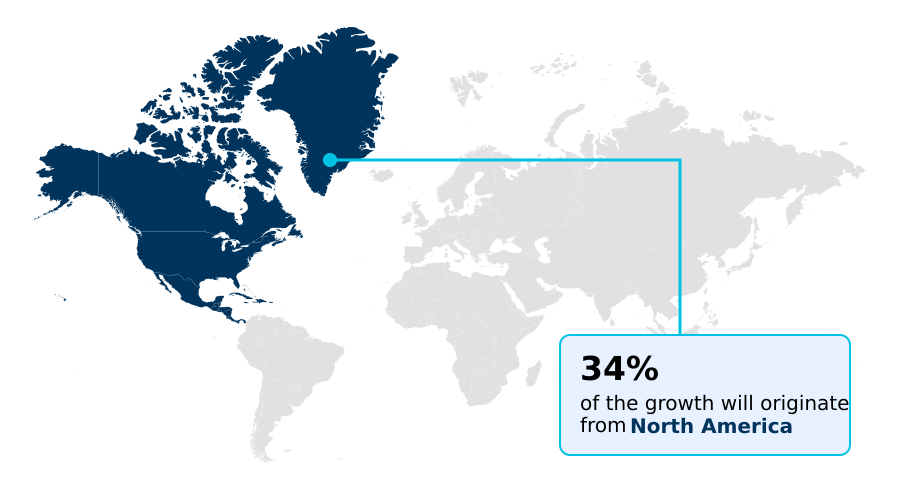

- North America dominated the market and accounted for a 33.7% growth during the forecast period.

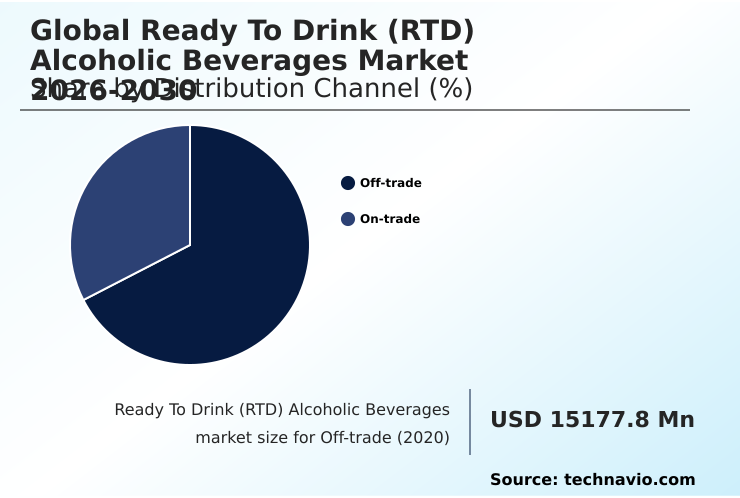

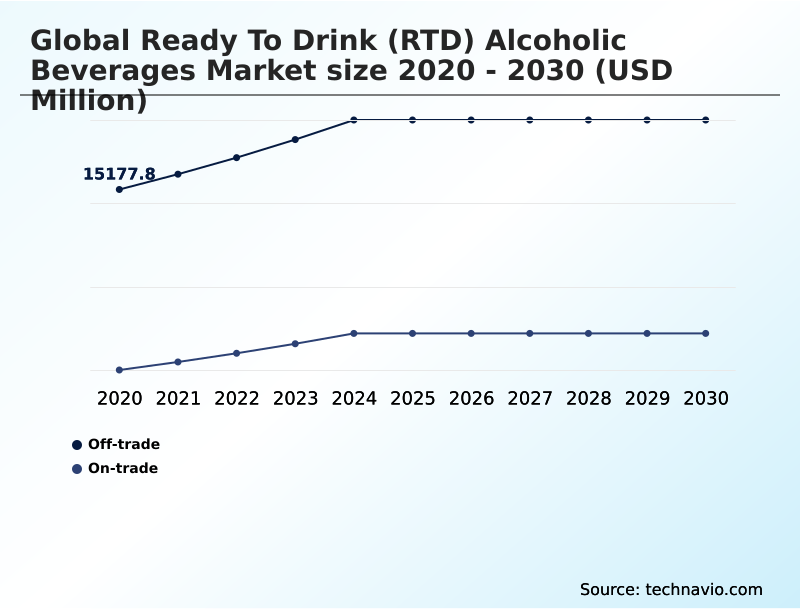

- By Distribution Channel - Off-trade segment was valued at USD 18.20 billion in 2024

- By Packaging - Bottles segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 15.28 billion

- Market Future Opportunities: USD 9.26 billion

- CAGR from 2025 to 2030 : 5.8%

Market Summary

- The ready to drink (rtd) alcoholic beverages market is undergoing a significant transformation, driven by consumer demand for convenience and high-quality ingredients. This evolution is marked by a structural shift from traditional malt-based beverages to sophisticated spirit-based cocktails and hard seltzers. The trend reflects a broader cultural move toward mindful consumption, where low-calorie options and functional ingredients are increasingly prioritized.

- In this competitive landscape, manufacturers focus on innovation in flavor and format, introducing everything from exotic fruits and botanical infusions to single-serve packaging designed for active lifestyles. For instance, a supply chain manager must now navigate the complexities of sourcing authentic tequila and small-batch whiskey while simultaneously managing the logistics of high-speed canning lines and sustainable packaging solutions.

- This dual focus on product quality and operational efficiency is critical for capitalizing on the demand for premium, portable beverage formats. The market's dynamism is fueled by this constant balancing act, catering to a discerning consumer base that expects both a bar-quality experience and on-the-go convenience.

What will be the Size of the Ready To Drink (RTD) Alcoholic Beverages Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ready To Drink (RTD) Alcoholic Beverages Market Segmented?

The ready to drink (rtd) alcoholic beverages industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Off-trade

- On-trade

- Packaging

- Bottles

- Cans

- Others

- Type

- Hard seltzers

- Canned cocktails

- Flavored malt beverages

- Hard ciders

- Hard kombucha

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The off-trade segment is estimated to witness significant growth during the forecast period.

The off-trade segment, encompassing supermarkets and convenience stores, is the primary force in the ready to drink (rtd) alcoholic beverages market. This channel thrives on providing on-the-go convenience and ready-to-drink solutions for home consumption and social events.

The expansion of spirit-based compositions and hard seltzers has broadened the product assortment, leveraging eye-catching single-serve packaging to attract consumers. North America's market dynamics show this channel contributes over 33% of incremental growth, underscoring its importance.

The success within this segment relies on efficient distribution and the availability of chilled, portable beverage formats. As the mindful drinking trend evolves, the demand for low-alcohol products and clean labeling continues to shape purchasing decisions within these retail environments.

The Off-trade segment was valued at USD 18.20 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ready To Drink (RTD) Alcoholic Beverages Market Demand is Rising in North America Get Free Sample

The geographic landscape of the ready to drink (RTD) alcoholic beverages market is characterized by diverse regional dynamics and growth rates.

APAC is set to expand at the fastest pace, with a projected rate of 6.2%, driven by the popularity of hyper-localized flavors and modern social drinking habits.

North America, growing at a strong 6.0%, remains a hub for premiumization, with a focus on spirit-based RTDs and ultra-premium formulations. Europe is shaped by the mindful drinking trend, with demand for low-alcohol products and non-alcoholic spirits expanding.

These regional distinctions necessitate tailored strategies, from leveraging yuzu flavor in Asia to promoting organic botanicals and rescued orchard fruit in Western markets, ensuring relevance in a globally competitive environment.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the ready to drink (RTD) alcoholic beverages market will be defined by strategic navigation of its complex landscape, moving beyond broad trends to capture niche opportunities. A key battleground remains spirit-based vs malt-based RTDs, where the premiumization impact on profit margins is significant for companies investing in authentic spirit bases in cocktails.

- Success demands a sophisticated approach to rtd flavor innovation strategies and marketing nostalgic flavors in adult beverages to maintain consumer engagement. However, regulatory hurdles in rtd market and the tax implications of spirit-based rtds create significant barriers, requiring expert navigation.

- Operationally, the logistics of rtd supply chains are under pressure from demand for sustainable packaging for canned cocktails, with the geopolitical impact on aluminum supply adding another layer of risk. The impact of e-commerce on rtd sales is transforming distribution, making farm-to-bottle transparency and direct-to-consumer models more viable.

- Meanwhile, the on-trade channels represent a growth area, where a brand’s ability to offer consistent, high-quality serves can create a strong competitive advantage, with off-trade channels accounting for more than twice the sales volume. Ultimately, balancing quality and convenience in rtds while managing rapid rtd product lifecycles and consumer preference for clean labels will separate market leaders from followers.

What are the key market drivers leading to the rise in the adoption of Ready To Drink (RTD) Alcoholic Beverages Industry?

- The institutionalization of premiumization and the infusion of craft-oriented spirits are key drivers of market growth.

- Key drivers for the ready to drink (RTD) alcoholic beverages market are rooted in premiumization and convenience. A structural shift toward sophisticated, craft-oriented spirit infusions is underway, as consumers prioritize the quality of ingredients over volume.

- This is evident in the preference for authentic spirit bases and complex flavor profiles featuring botanical infusions. Concurrently, the proliferation of portable, single-serve beverage formats caters to mobile, fast-paced lifestyles, eliminating the need for mixology skills.

- The transition to lightweight packaging has improved portability and sustainability, with some manufacturers reducing packaging weight by 10%. This focus on high-fidelity flavor and effortless consumption ensures the segment captures market share from traditional alcohol categories.

What are the market trends shaping the Ready To Drink (RTD) Alcoholic Beverages Industry?

- A strategic shift toward ultra-premium, spirit-based formulations is redefining the market. This trend highlights a growing consumer preference for convenient, bar-quality experiences.

- The ready to drink (RTD) alcoholic beverages market is defined by a significant trend toward ultra-premium, spirit-based formulations, representing a departure from traditional malt-based offerings. Consumers increasingly seek a bar-quality experience in convenient formats, driving demand for pre-mixed cocktails featuring high-end spirits.

- This shift is supported by the rapid expansion of e-commerce, where premium products often outperform due to detailed brand storytelling. The integration of functional ingredients and health-conscious attributes, such as zero residual sugar, is now a primary competitive advantage.

- The success of these products depends on balancing a familiar alcoholic profile with genuine nutritional transparency, with some brands achieving a 15% lower caloric content than their predecessors. This evolution underscores a strategic pivot toward quality and brand heritage.

What challenges does the Ready To Drink (RTD) Alcoholic Beverages Industry face during its growth?

- Stringent regulatory environments and complex taxation frameworks present a key challenge to industry growth.

- The ready to drink (RTD) alcoholic beverages market confronts significant challenges from stringent regulations and intense competition. Complex taxation frameworks, which differ based on the alcohol base, complicate multi-regional expansion and can extend product launch timelines by several months.

- This regulatory fragmentation is compounded by a saturated competitive landscape where brand loyalty is low, and the desire for novelty is high. The short lifespan of flavor trends forces companies to manage rapid product lifecycles, risking inventory obsolescence.

- Furthermore, the rising demand for sustainable packaging solutions adds logistical complexities, with the administrative overhead for environmental documentation increasing operational costs by over 20% for some distributors.

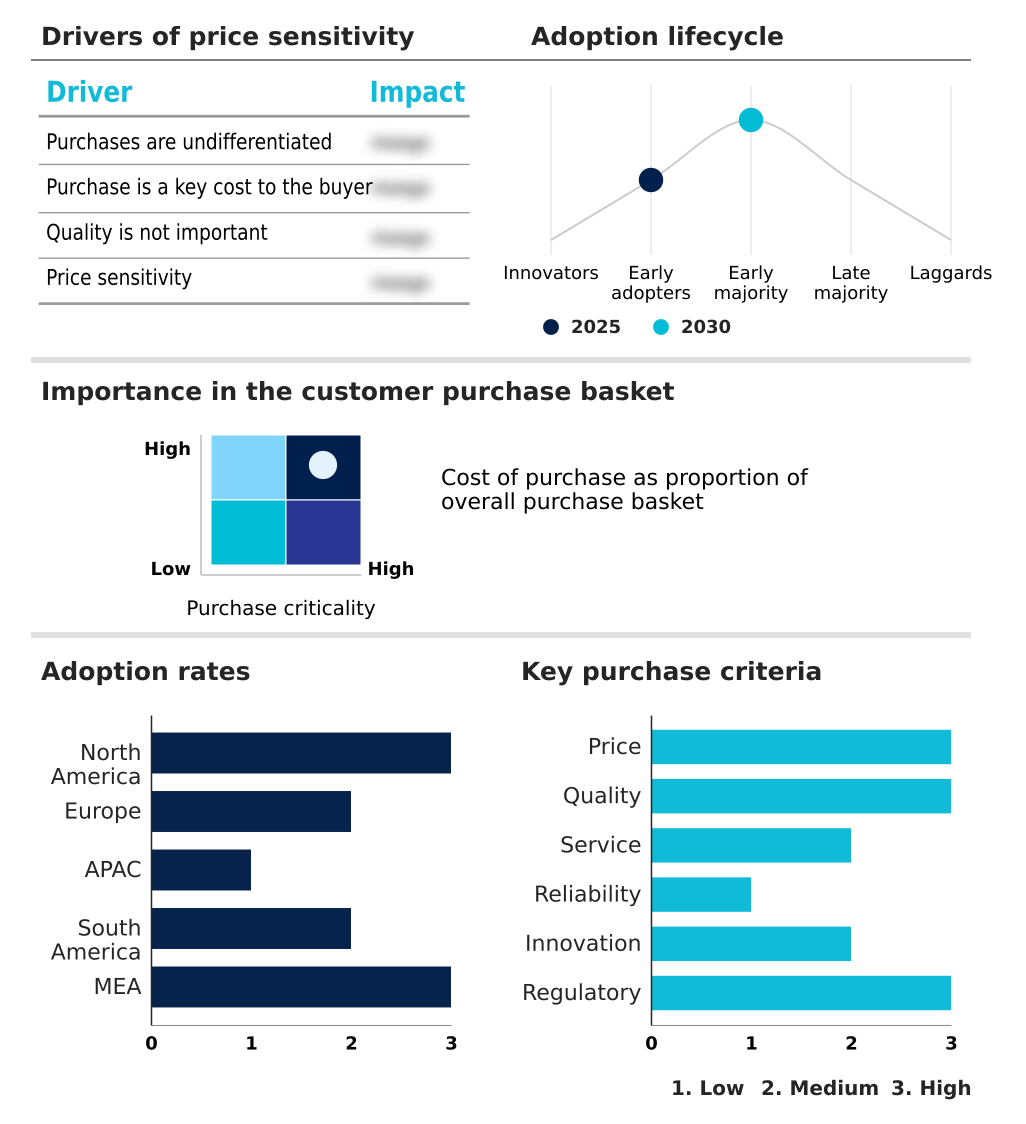

Exclusive Technavio Analysis on Customer Landscape

The ready to drink (rtd) alcoholic beverages market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ready to drink (rtd) alcoholic beverages market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ready To Drink (RTD) Alcoholic Beverages Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ready to drink (rtd) alcoholic beverages market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - The company provides a diverse portfolio of ready-to-drink alcoholic beverages, including spirit-based cocktails and flavored malt-based options designed for consumer convenience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Brown Forman Corp.

- BuzzBallz LLC

- Campari Group

- Carlsberg Breweries AS

- Constellation Brands Inc.

- Diageo PLC

- Fishers Island Lemonade

- Heineken NV

- Kirin Holdings Co. Ltd.

- Lion Pty Ltd

- Loverboy Inc.

- Mark Anthony Brands Inc.

- Molson Coors Beverage Co.

- Pernod Ricard SA

- Spirit of Gallo

- Suntory Beverage and Food Ltd.

- The Asahi Shimbun Co.

- The Boston Beer Co. Inc.

- Treasury Wine Estates Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ready to drink (rtd) alcoholic beverages market

- In September 2024, a leading global spirits company announced the acquisition of a fast-growing artisanal gin brand known for its botanical infusions, signaling a strategic move to capture the ultra-premium segment of the market.

- In November 2024, a major beverage conglomerate expanded its partnership with a soft drink giant to launch a new line of co-branded, spirit-based canned cocktails across several key North American markets.

- In February 2025, Brown-Forman Corporation announced it would assume full in-house control of the production, sales, and distribution for its Jack Daniel's Country Cocktails portfolio, ending a long-term third-party partnership to centralize its RTD strategy.

- In April 2025, Asahi Group Holdings launched Asahi Clear Highball, a new ready-to-drink product specifically tailored for the South Korean market, featuring a localized yuzu flavor profile to meet regional consumer preferences.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ready To Drink (RTD) Alcoholic Beverages Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.8% |

| Market growth 2026-2030 | USD 9256.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.4% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ready to drink (RTD) alcoholic beverages market is characterized by a rapid evolution toward premiumization and portfolio diversification. A structural shift is underway as consumers favor spirit-based cocktails and canned cocktails over traditional malt-based beverages. This has led to a surge in demand for authentic tequila, artisanal gin, and small-batch whiskey as foundational ingredients.

- The market's 5.4% year-over-year growth underscores the consumer appetite for convenience without compromising on quality. This trend compels boardroom decisions to pivot R&D budgets toward developing sophisticated, ultra-premium formulations featuring real fruit juices and organic botanicals.

- Key industry players are increasingly focused on acquiring or developing hard seltzers, hard ciders, and even hard kombucha to meet the demand for low-calorie options. The emphasis on mindful consumption is also driving innovation in non-alcoholic spirits and sugar-free series, forcing a re-evaluation of product strategy to align with health-conscious consumer values and capture a broader market share.

What are the Key Data Covered in this Ready To Drink (RTD) Alcoholic Beverages Market Research and Growth Report?

-

What is the expected growth of the Ready To Drink (RTD) Alcoholic Beverages Market between 2026 and 2030?

-

USD 9.26 billion, at a CAGR of 5.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Off-trade, and On-trade), Packaging (Bottles, Cans, and Others), Type (Hard seltzers, Canned cocktails, Flavored malt beverages, Hard ciders, and Hard kombucha) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of premiumization and craft oriented spirit infusions, Stringent regulatory environments and complex taxation frameworks

-

-

Who are the major players in the Ready To Drink (RTD) Alcoholic Beverages Market?

-

Anheuser Busch InBev SA NV, Brown Forman Corp., BuzzBallz LLC, Campari Group, Carlsberg Breweries AS, Constellation Brands Inc., Diageo PLC, Fishers Island Lemonade, Heineken NV, Kirin Holdings Co. Ltd., Lion Pty Ltd, Loverboy Inc., Mark Anthony Brands Inc., Molson Coors Beverage Co., Pernod Ricard SA, Spirit of Gallo, Suntory Beverage and Food Ltd., The Asahi Shimbun Co., The Boston Beer Co. Inc. and Treasury Wine Estates Ltd.

-

Market Research Insights

- The market dynamics for ready-to-drink alcoholic beverages are increasingly influenced by the better-for-you movement and the demand for health-conscious formats. The sober curious movement has fueled a market for low-ABV beverages that allow for social participation, with some new product lines achieving a 20% reduction in sugar content compared to previous formulations.

- This pivot toward wellness is not uniform globally; North America is responsible for over 33% of incremental growth, driven by premium canned cocktails, while APAC's contribution of 31% is fueled by flavor-forward beverages and the adoption of modern social drinking habits.

- The ability to deliver functional ingredients and align with active lifestyles is becoming a key differentiator, influencing both product development and regional growth strategies.

We can help! Our analysts can customize this ready to drink (rtd) alcoholic beverages market research report to meet your requirements.

RIA -

RIA -