Saudi Arabia Retail Market Size 2026-2030

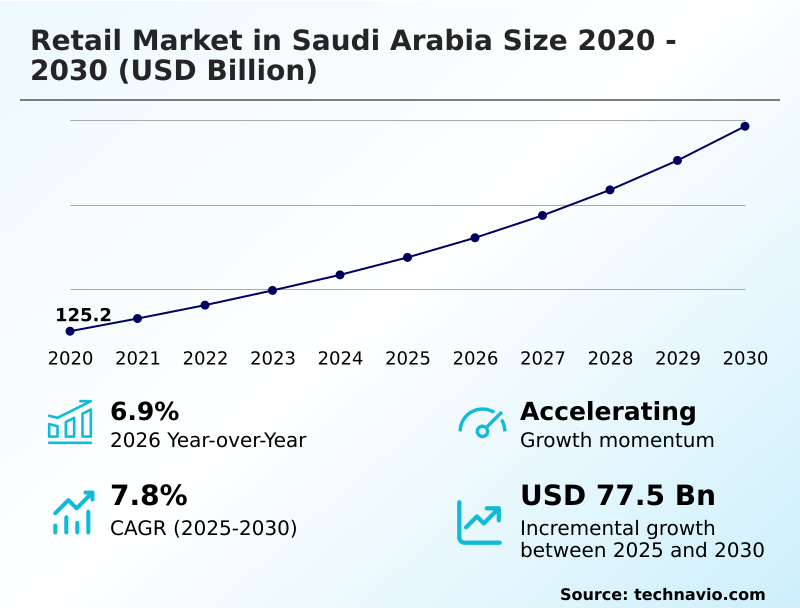

The Saudi Arabia Retail Market size was valued at USD 168.8 billion in 2025, growing at a CAGR of 7.8% during the forecast period 2026-2030.

Major Market Trends & Insights

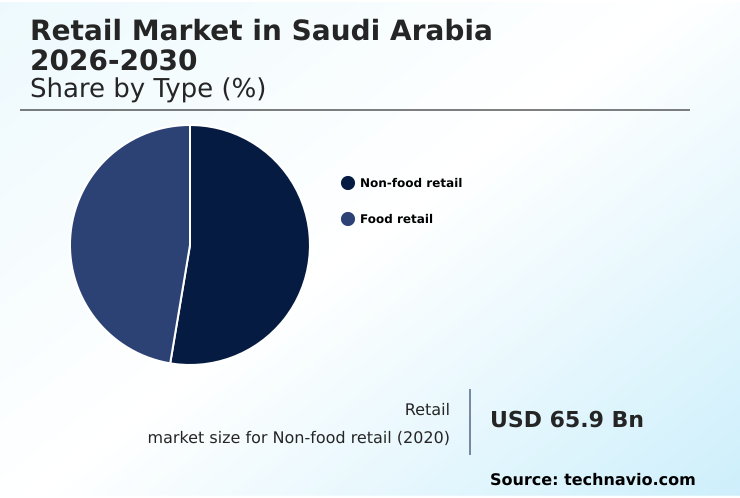

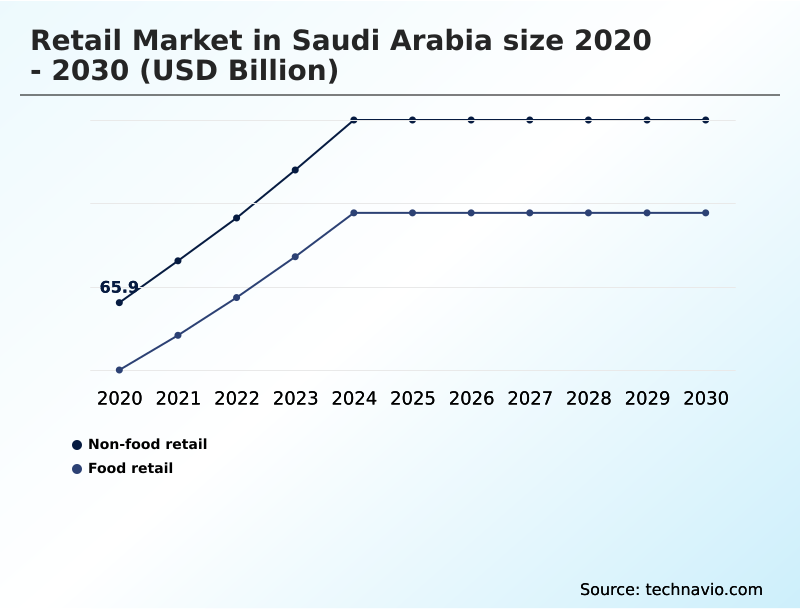

- By Type - Non-food retail segment was valued at USD 83.8 billion in 2024

- By Distribution Channel - Bakalas segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 121.1 billion

- Market Future Opportunities 2025-2030: USD 77.5 billion

- CAGR from 2025 to 2030 : 7.8%

Market Summary

- The retail market in saudi arabia is experiencing a profound transformation, with retailers that adopt an omnichannel model reporting a customer lifetime value that is 30% higher than single-channel operators. The implementation of AI-driven demand forecasting has also enabled businesses to reduce inventory holding costs by up to 15%.

- A key business scenario involves leveraging data analytics to unify online and offline shopping experiences, providing personalized promotions based on real-time consumer behavior analysis. This shift is primarily driven by economic diversification efforts under Vision 2030, which boosts consumer spending power and encourages investment in modern retail infrastructure.

- However, the market faces significant challenges related to regulatory compliance, as evolving legal frameworks for data protection and Saudization policies require constant adaptation and investment in new systems, which can strain operational resources, particularly for smaller enterprises.

What will be the Size of the Saudi Arabia Retail Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Saudi Arabia Retail Market Segmented?

The saudi arabia retail industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Non-food retail

- Food retail

- Distribution channel

- Bakalas

- Super markets

- Hyper markets

- Online

- Product

- Food and beverages

- Apparel

- Electronics and appliances

- Others

- Geography

- Middle East and Africa

- Saudi Arabia

- Middle East and Africa

How is the Saudi Arabia Retail Market Segmented by Type?

The non-food retail segment is estimated to witness significant growth during the forecast period.

The non-food retail segment, where adoption of augmented reality for virtual try-ons has increased customer engagement by over 20%, is rapidly evolving.

This sector, encompassing consumer electronics and apparel, undergoes constant transformation driven by dynamic consumer behavior analysis and a demand for personalization, with retailers using AI seeing a 15% uplift in conversion rates.

The integration of advanced technologies like AI in inventory management is critical for optimizing stock levels and minimizing carrying costs. Omnichannel retailing strategies are standard, blending physical and digital storefronts to create a seamless customer journey.

The emphasis on the circular economy also influences product strategies, as resale and rental models gain traction, reflecting a shift in consumer values.

The Non-food retail segment was valued at USD 83.8 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Saudi Arabia Retail Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning within the retail market in Saudi Arabia 2026-2030 increasingly focuses on understanding the long-term impact of vision 2030 on retail. Consequently, developing a robust omnichannel retail strategy in Saudi Arabia has become a key priority, with companies that successfully integrate digital and physical channels observing a customer conversion rate that is nearly double that of their brick-and-mortar-only counterparts.

- Addressing the persistent challenges in Saudi Arabia's e-commerce logistics, particularly for last-mile delivery, remains a critical operational hurdle. The pace of technology adoption in saudi retail stores is accelerating as businesses seek to enhance efficiency and customer experience. Simultaneously, ensuring Saudi Arabia retail market compliance, including adherence to Saudization and data protection laws, is a non-negotiable aspect of operations.

- Across the region, a growing emphasis on sustainable retail practices Middle East is shaping brand perception and influencing consumer choice, pushing companies to rethink their supply chains and product offerings.

What are the key market drivers leading to the rise in the adoption of Saudi Arabia Retail Industry?

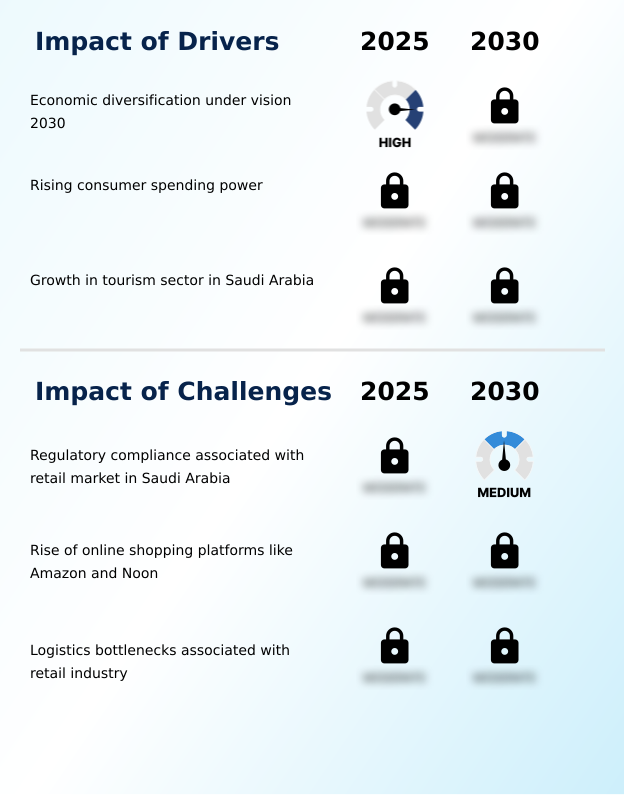

- Economic diversification under Vision 2030 is a key driver for the retail market in Saudi Arabia.

- Economic diversification under Vision 2030 is the principal driver of growth in the retail market in saudi arabia, stimulating a rise in consumer spending power.

- Government investments in new commercial and entertainment mega-projects are expected to increase retail footfall by more than 20% in key urban centers. This initiative not only creates jobs but also fosters a more dynamic and competitive retail environment.

- Another key driver is the growth in the tourism sector, which directly boosts sales in categories such as luxury goods, souvenirs, and dining.

- The influx of international visitors, projected to rise significantly, introduces new consumer segments and demands, compelling retailers to broaden their product offerings and service standards.

What are the market trends shaping the Saudi Arabia Retail Industry?

- The integration of technology is a defining trend in the retail market in Saudi Arabia. This is driven by rapid digital adoption and evolving consumer expectations.

- A significant trend shaping the retail market in saudi arabia is the rapid integration of advanced technology into both online and offline operations. The adoption of omnichannel retailing is a primary focus, with retailers reporting that offering a click-and-collect service increases foot traffic by over 20%.

- The use of AI-powered personalization engines is also on the rise, enabling businesses to achieve a 5-15% uplift in average transaction value by delivering tailored recommendations. Furthermore, there is a growing emphasis on sustainable retail, driven by consumer demand for ethical sourcing and environmentally friendly products.

- This shift is compelling retailers to re-evaluate their supply chain management and operational practices to enhance transparency and reduce their carbon footprint.

What challenges does the Saudi Arabia Retail Industry face during its growth?

- Navigating regulatory compliance associated with the retail market in Saudi Arabia poses a key challenge to industry growth.

- Navigating the complex and evolving regulatory landscape is a primary challenge for the retail market in saudi arabia. Adherence to Saudization policies, which mandate employment quotas for nationals, can increase labor costs by 10-15% for certain job categories compared to expatriate labor.

- Furthermore, strict compliance with the Personal Data Protection Law (PDPL) requires significant investment in data governance and security infrastructure, challenging retailers that rely on customer data for personalization. Logistics bottlenecks, especially in last-mile delivery to remote areas, continue to be a hurdle, impacting customer satisfaction and adding to operational costs for e-commerce platforms.

Exclusive Technavio Analysis on Customer Landscape

The saudi arabia retail market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the saudi arabia retail market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Saudi Arabia Retail Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, saudi arabia retail market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abdullah Al Othaim Markets Co. - Offerings are characterized by diversified portfolios, leveraging franchise agreements to provide a mix of food, fashion, and electronics through integrated omnichannel retailing platforms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abdullah Al Othaim Markets Co.

- Ali Hassan AI Dahan Co.

- Alsadhan Trading Co

- Arabian Stores Co. Ltd.

- Azadea Group

- Bindawood Holding Co.

- Cenomi Retail

- Chalhoub Group

- Jarir Marketing Co.

- Lulu Group International

- M. H. Alshaya Co. WLL

- Majid Al Futtaim Holding LLC

- Nahdi Medical Co.

- SACO

- Savola Group

- Tamimi Markets

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the broadline retail industry, the integration of artificial intelligence and machine learning for dynamic pricing and personalization is now standard, directly impacting the retail market by compelling local players to adopt similar technologies to maintain a competitive edge and improve customer retention by up to 15%.

- A significant investment in warehouse automation and advanced logistics platforms has occurred to support the exponential growth of e-commerce, which challenges the retail market to upgrade its last-mile delivery infrastructure to meet consumer expectations of delivery within 24-48 hours.

- There is a growing end-user and regulatory push towards sustainable retail and circular economy models, including product take-back and resale programs, forcing the retail market to innovate in its supply chain management and product lifecycle tracking to comply with emerging ESG standards.

- The widespread adoption of digital payment solutions and fintech innovations is accelerating the shift to a cashless economy, which fundamentally supports the growth of online marketplace platforms within the retail market by reducing transaction friction and enhancing security.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Saudi Arabia Retail Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 179 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.8% |

| Market growth 2026-2030 | USD 77.5 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The retail ecosystem in Saudi Arabia involves a complex interplay of stakeholders, where international suppliers provide over 60% of non-food retail goods. This reliance on global brands creates a competitive dynamic for local manufacturers and retailers like Abdullah Al Othaim Markets and Jarir Marketing Co.

- Regulatory bodies, including the Ministry of Commerce and the Saudi Arabian Monetary Authority (SAMA), enforce standards for everything from product authenticity to digital payments, impacting operational workflows. Compliance with mandates such as Saudization can increase operational costs by an estimated 5-8%.

- The value chain is completed by a developing logistics network and a young, digitally-native consumer base whose preferences are rapidly shifting towards e-commerce platforms and omnichannel experiences.

What are the Key Data Covered in this Saudi Arabia Retail Market Research and Growth Report?

-

What is the expected growth of the Saudi Arabia Retail Market between 2026 and 2030?

-

The Saudi Arabia Retail Market is expected to grow by USD 77.5 billion during 2026-2030, registering a CAGR of 7.8%. Year-over-year growth in 2026 is estimated at 6.9%%. This acceleration is shaped by economic diversification under vision 2030, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Non-food retail, and Food retail), Distribution Channel (Bakalas, Super markets, Hyper markets, and Online), Product (Food and beverages, Apparel, Electronics and appliances, and Others) and Geography (Middle East and Africa). Among these, the Non-food retail segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Middle East and Africa. Country-level analysis includes Saudi Arabia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is economic diversification under vision 2030, which is accelerating investment and industry demand. The main challenge is regulatory compliance associated with retail market in saudi arabia, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Saudi Arabia Retail Market?

-

Key vendors include Abdullah Al Othaim Markets Co., Ali Hassan AI Dahan Co., Alsadhan Trading Co, Arabian Stores Co. Ltd., Azadea Group, Bindawood Holding Co., Cenomi Retail, Chalhoub Group, Jarir Marketing Co., Lulu Group International, M. H. Alshaya Co. WLL, Majid Al Futtaim Holding LLC, Nahdi Medical Co., SACO, Savola Group and Tamimi Markets. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the retail market in saudi arabia is fragmented, with the top five players accounting for less than 40% of the total market share. Major companies, including Majid Al Futtaim and Lulu Group International, are expanding their physical and digital footprints, focusing on experiential retail to attract and retain customers.

- These firms are actively investing in technology to enhance the shopping experience, with loyalty programs boosting customer retention by over 10% in some cases. Innovation is centered around integrating e-commerce platforms with brick-and-mortar stores, creating a seamless omnichannel retailing experience.

- A primary challenge remains adapting to Saudization policies, which requires significant investment in training and development to meet workforce quotas while maintaining service quality and operational efficiency.

We can help! Our analysts can customize this saudi arabia retail market research report to meet your requirements.

RIA -

RIA -