Server Motherboard Market Size 2024-2028

The server motherboard market size is forecast to increase by USD 4.97 billion at a CAGR of 17.51% between 2023 and 2028.

As businesses strive to store and process more data, the demand for data centers and server farms is skyrocketing. At the same time, the rise of affordable motherboards for server systems is opening the door for small and medium-sized businesses to access cutting-edge server technology. The market is experiencing strong growth, driven by the increasing demand for data center servers and the subsequent expansion of network infrastructure. However, global economic uncertainties and supply chain disruptions pose challenges to market growth.

Despite these challenges, the market is expected to continue expanding due to the growing importance of digital transformation and the need for reliable and efficient server technology. The market analysis report provides a comprehensive overview of these trends and the factors influencing market growth.

What will be the Server Motherboard Market Size During the Forecast Period?

- Key components of server motherboards include memory modules, processors, expansion slots for PCI-express graphics cards and network adapters, and various hardware connections for hard drives and video cards. Miniaturization is a significant trend In the market, with mid-range motherboards becoming increasingly popular due to their compact size and cost-effectiveness. Central processing units from both AMD and Intel platforms dominate the market, with Intel's offerings maintaining a slight edge in market share.

- Additionally, data center services continue to fuel demand for server motherboards, with data servers requiring high-density, high-performance motherboards to support storage controllers, RAID controllers, and gigabit ethernet ports. Memory and processor capabilities remain critical factors In the purchasing decision, with the latest DDR4 memory modules and multi-core processors offering significant performance gains. Desktop and laptop motherboards continue to evolve, with advancements in PCI-express technology enabling faster data transfer and improved connectivity options. Overall, the market is expected to continue its growth trajectory, driven by the increasing importance of data processing and storage in various industries.

How is this Server Motherboard Industry segmented and which is the largest segment?

The server motherboard industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- RISC

- CISC

- VLIW

- End-user

- Enterprise

- Personal

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- South America

- Middle East and Africa

- APAC

By Type Insights

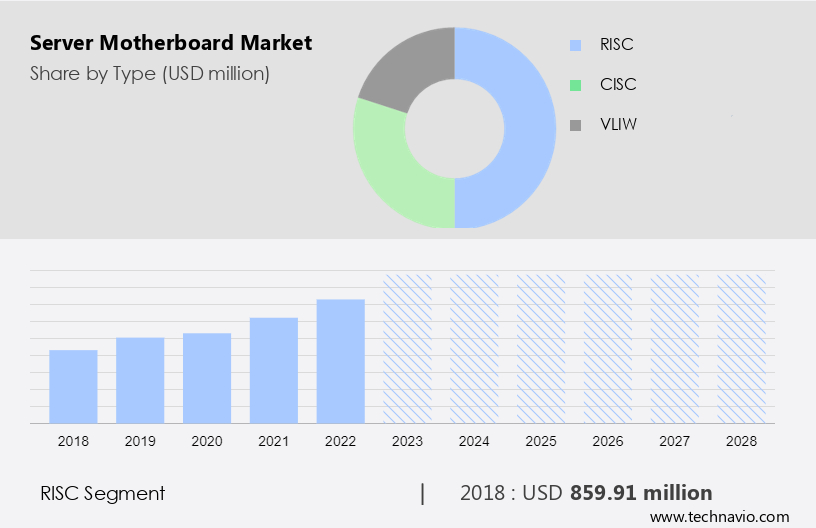

- The RISC segment is estimated to witness significant growth during the forecast period.

The market is driven by various factors, including the adoption of RISC architecture. RISC processors, such as those based on ARM, Power, and SPARC architectures, offer power efficiency, quick instruction execution, and tailored processing capabilities, making them suitable for edge computing and IoT applications. While x86 architecture remains dominant, RISC solutions are gaining traction in specific use cases.

Additionally, the RISC segment's growth will contribute to the overall expansion of the market during the forecast period. Power efficiency and performance requirements are key considerations In the market, with RISC architectures offering a streamlined instruction set for quick execution and reduced power consumption. As RISC processors become increasingly relevant in edge computing and IoT environments, the market for server motherboards is poised for growth.

Get a glance at the Server Motherboard Industry report of share of various segments Request Free Sample

The RISC segment was valued at USD 859.91 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

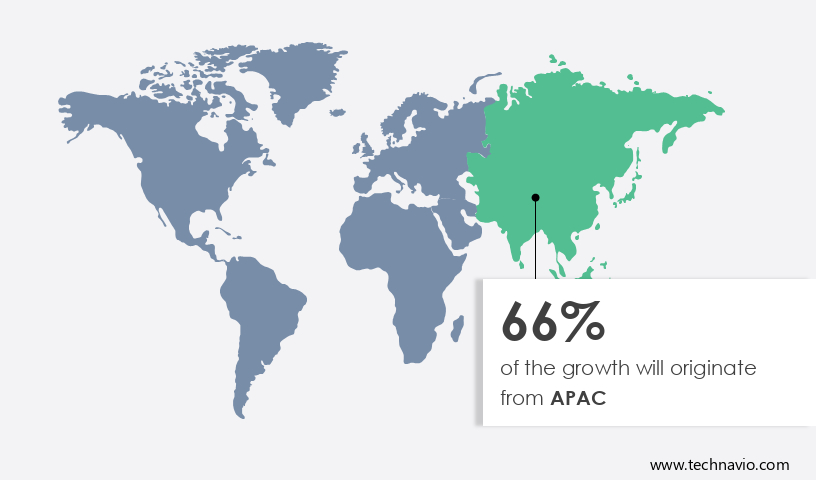

- APAC is estimated to contribute 66% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The motherboard market in APAC held a substantial share of the global server motherboard industry in 2023. China, Taiwan, South Korea, and Japan emerged as the leading revenue generators in this market. The region is projected to experience rapid growth during the forecast period due to increasing industrialization and rising disposable incomes. In APAC, the demand for motherboards is driven by the automotive and electronics sectors, which are undergoing significant growth. Industrial development in countries like China, India, South Korea, Indonesia, and Taiwan necessitates automation, further boosting the motherboard market. Key components of a motherboard include processors, memory modules, expansion slots, and system boards, which are essential for the functioning of computers, desktops, laptops, and data centers.

Market Dynamics

Our server motherboard market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Server Motherboard Industry?

Increasing demand for data centers and server farms is the key driver of the market.

- The market has experienced significant growth due to the increasing demand for data processing and storage in today's digital landscape. Data centers and server farms are essential infrastructures for handling the massive amounts of data generated by online applications, connected devices, and big data analytics. Server motherboards are a critical component of these systems, as they support high-performance processors, expansive memory modules, and various expansion slots for network adapters, storage controllers, and RAID controllers. The server motherboard industry caters to various system components, including data center servers, enterprise servers, and commercial motherboards. These boards prioritize durability, connection reliability, and industry-standard architecture, such as Micro Channel, AMD, and Intel platforms. The market also offers mid-range motherboards for cost-effective server systems and motherboards for desktop and laptop computers. The proliferation of edge computing has led to the establishment of edge data centers, further expanding the market for server motherboards.

- Additionally, edge data centers require motherboards that can handle the unique demands of decentralized processing, such as vibration resistance and miniaturization. Server motherboards are essential for server virtualization, enabling multi-tasking and multi-processing capabilities. They support various hardware components, including central processing units, memory, PCI-Express slots, and Gigabit Ethernet ports. Server motherboards also cater to the needs of various industries, such as gaming PCs, cloud services, and data centers, offering performance-per-watt ratios and hardware-software optimizations. Thus, the market is a dynamic and evolving industry that plays a crucial role In the digital infrastructure of businesses and organizations. With the increasing demand for data processing and storage, server motherboards will continue to be a vital component in data center environments and edge computing applications.

What are the market trends shaping the Server Motherboard Industry?

The popularity of low-cost motherboards in server systems is the upcoming market trend.

- The market encompasses the production and sale of mainboards and system boards used in data center servers, computers, and various other computing systems. These boards house essential system components such as processors, memory modules, expansion slots, and various connectors for network adapters, storage controllers, RAID controllers, and Gigabit Ethernet ports. The server motherboard industry caters to diverse applications, from commercial enterprise servers to miniaturized microservers, gaming PCs, and desktop and laptop computers. The popularity of low-cost motherboards in server systems is driven by factors beyond cost. Performance, reliability, and scalability are also essential considerations. Small businesses, startups, and budget-conscious organizations often opt for these entry-level motherboards to build their server infrastructure. These boards offer basic functionality, making them suitable for non-critical applications and workloads that do not demand advanced features or extensive processing power.

- Additionally, major players In the market adhere to industry standard architectures, such as AMD and Intel platforms, ensuring compatibility with a wide range of hardware and software. These motherboards come in various form factors, including microchannel, mid-range, and high-end models. The server board industry's focus on board durability, capacity, and connection reliability caters to the demands of data centers, server farms, and cloud services. Motherboards' internal components, including processors, memory, and PCI-Express slots, are continually evolving to enhance performance-per-watt ratios and support multi-tasking, multi-processing, virtualization, and system architecture advancements. The market's growth is fueled by the increasing adoption of big data, cloud services, and the integration of hardware components like hard drives, video cards, and MSI motherboards.

What challenges does the Server Motherboard Industry face during its growth?

Global economic uncertainties and supply chain disruptions are key challenges affecting the industry's growth.

- The market is a critical component of the data center industry, encompassing main boards and system boards for both commercial and enterprise servers. These motherboards serve as the backbone of server systems, accommodating various system components such as processors, memory modules, expansion slots, and network adapters. The market is influenced by industry-standard architectures like AMD and Intel platforms, with a focus on board durability and connection reliability. Data centers, server farms, and cloud services are significant consumers of server motherboards.

- However, economic uncertainties and supply chain disruptions can impact data center expansion plans, leading to market growth challenges. Component shortages and increased prices due to disruptions can also affect the production cost of server motherboards. Miniaturization and the integration of advanced features like PCI-Express slots, RAID controllers, and Gigabit Ethernet ports are trends shaping the market. Additionally, the market caters to various applications, including data servers, server virtualization, and gaming PCs. The server motherboard industry faces the complexities of a global supply chain, with components sourced from various regions. Natural disasters, geopolitical events, and pandemics can disrupt the supply chain, leading to component shortages and increased prices. These factors, coupled with the need for high-performance, low-cost motherboards, contribute to the market's growth dynamics.

Exclusive Customer Landscape

The server motherboard market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the server motherboard market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, server motherboard market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASRock Inc.

- ASUSTeK Computer Inc.

- BIOSTAR Group.

- EVGA Corp.

- Gigabyte Technology Co. Ltd.

- Intel Corp.

- Micro Star International Co. Ltd.

- MiTAC Holdings Corp.

- Sahasra

- Super Micro Computer Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses the production and sale of main boards designed specifically for data center servers. These systems serve as the foundation for the various components and technologies that enable the processing, storage, and transmission of vast amounts of data. At the heart of a server motherboard lies the system architecture, which adheres to industry standards such as micro channel. This architecture facilitates the integration of various components, including processors, memory modules, expansion slots, and network adapters. Data centers rely on server systems to maintain high capacity and workflow efficiency. Connection reliability and durability are essential factors In the selection of server motherboards. Vibrations, a common issue in data centers, can impact the performance and longevity of internal components. To mitigate this, motherboards undergo rigorous testing and adhere to stringent industry standards. Server motherboards cater to various market segments, from commercial applications to enterprise servers. The industry continues to evolve, with trends such as server virtualization, miniaturization, and the integration of AMD and Intel platforms driving innovation.

Additionally, the server board industry is characterized by a focus on performance-per-watt ratios and the integration of advanced hardware and software features. These include multi-tasking, multi-processing, virtualization, and system architecture optimized for PCs, laptops, tablets, smartphones, and other computing devices. Memory, storage devices, and other hardware components play a crucial role In the functionality and efficiency of server motherboards. PCI-Express slots, RAID controllers, and gigabit ethernet ports are just a few examples of the technologies that enable high-speed data transfer and processing. The integration of advanced hardware and software features necessitates a strong focus on hardware and software compatibility. Motherboards must be able to support a wide range of processors, memory types, and expansion cards to accommodate diverse workloads and applications. The market is driven by the growing demand for data center services, cloud services, big data, and other data-intensive applications.

As a result, the industry continues to innovate, with trends such as microservers and gaming PCs emerging to meet the evolving needs of businesses and consumers alike. Thus, the market is a dynamic and innovative industry that plays a crucial role In the data processing and transmission landscape. Motherboards are designed to meet the unique demands of data center servers, with a focus on performance, reliability, and compatibility. The industry continues to evolve, driven by advancements in hardware, software, and industry trends.

|

Server Motherboard Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

144 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.51% |

|

Market growth 2024-2028 |

USD 4.97 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

17.35 |

|

Key countries |

US, Taiwan, China, Japan, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Server Motherboard Market Research and Growth Report?

- CAGR of the Server Motherboard industry during the forecast period

- Detailed information on factors that will drive the Server Motherboard growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the server motherboard market growth of industry companies

We can help! Our analysts can customize this server motherboard market research report to meet your requirements.

RIA -

RIA -