Testing, Inspection, And Certification Market Size 2024-2028

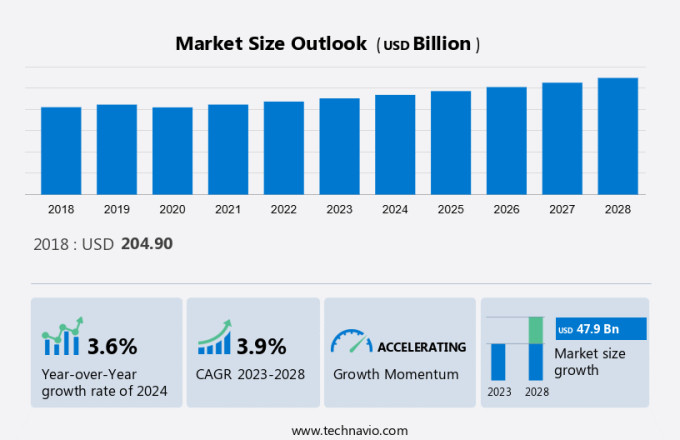

The testing, inspection, and certification market size is forecast to increase by USD 47.9 billion at a CAGR of 3.9% between 2023 and 2028.

- The market is experiencing significant growth due to several key drivers. Stringent regulations in various industries, such as logistics, healthcare services, consumer goods, renewable energy, energy and utilities, oil and gas, and CSR, necessitate rigorous testing and certification processes. companies are responding to this demand by launching innovative solutions to streamline and optimize these processes. However, the high costs associated with testing, inspection, and certification services remain a challenge for many organizations. In the logistics sector, for instance, intelligent logistics and Compression Stress Relaxation testing are becoming increasingly important to ensure the safe and efficient transportation of goods. Similarly, in the healthcare services sector, certification for medical devices and pharmaceuticals is crucial for patient safety and regulatory compliance.

- In the renewable energy sector, testing and certification are essential to ensure the reliability and safety of renewable energy systems. In the consumer goods industry, certification for product safety and quality is a must to maintain consumer trust and confidence. In the oil and gas industry, testing and certification are necessary to ensure the safety and efficiency of operations. CSR initiatives also require certification to demonstrate a company's commitment to ethical business practices. Overall, the market is a critical enabler for various industries to ensure safety, quality, and regulatory compliance.

What will be the Size of the Market During the Forecast Period?

- The inspection, testing, and certification (ITC) market plays a crucial role in ensuring the quality, safety, and compliance of various products and services across numerous industries. This market encompasses a range of activities, including testing laboratories, certification bodies, and inspection services. ITC is essential for various sectors, including transportation, logistics, healthcare services, consumer goods, renewable energy, energy and utilities, waste management, oil and gas, consumer electronics, agriculture, and food and beverage. These industries rely on ITC to maintain the integrity of their products and processes, protect the environment, and adhere to mandatory inspection laws.

- Inspection services are an integral part of the ITC market. These services involve physical examination of products, processes, and facilities to ensure they meet specific standards and regulations. For instance, in the transportation industry, collision avoidance systems undergo rigorous inspection to ensure they function correctly and safely. In the food and beverage sector, routine inspections help maintain food safety and quality. Certification is another critical aspect of the ITC market. It involves the granting of a certificate or accreditation to products or services that meet specific standards or regulations. For example, Element Materials Technology certifies materials used in various industries to ensure they meet the required specifications.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Service

- Testing

- Inspection

- Certification

- Sourcing

- In-house

- Outsourced

- Geography

- APAC

- China

- India

- Japan

- South Korea

- North America

- US

- Europe

- Germany

- UK

- France

- Italy

- Middle East and Africa

- South America

- Brazil

- APAC

By Service Insights

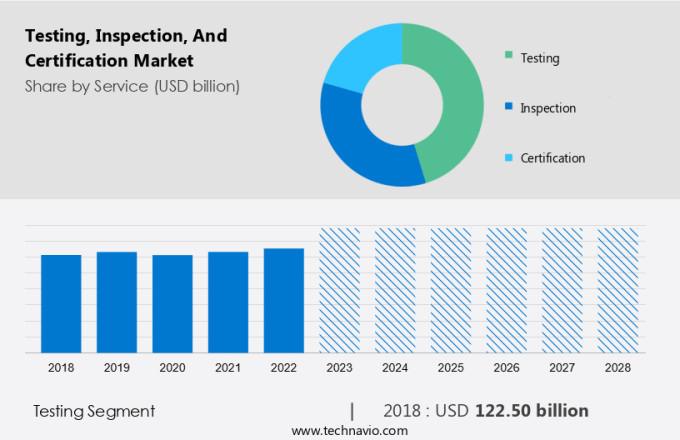

- The testing segment is estimated to witness significant growth during the forecast period.

Testing services are an indispensable part of manufacturing processes and supply chain activities, ensuring that goods meet safety, quality, and regulatory standards. This is essential for protecting consumers from potentially hazardous or substandard products, as well as mitigating risks for manufacturers related to product recalls, legal issues, and reputational damage due to non-compliance. In the global trade process, testing is a critical component, enabling products to meet local or international standards for legal marketing in various regions. Bureau Veritas is a leading provider of testing services, offering comprehensive analysis and inspections to ensure that products and commodities conform to required properties and regulatory specifications.

With expertise in various industries, including agriculture and food, chemicals, mining, aerospace and defense, waste management, and routine inspection, Bureau Veritas caters to a diverse range of clients. By outsourcing testing to professionals like Bureau Veritas, manufacturers can focus on their core competencies while ensuring that their products meet the necessary standards and regulations. This not only enhances product quality but also strengthens consumer trust and brand reputation.

Get a glance at the market report of share of various segments Request Free Sample

The Testing segment was valued at USD 122.50 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

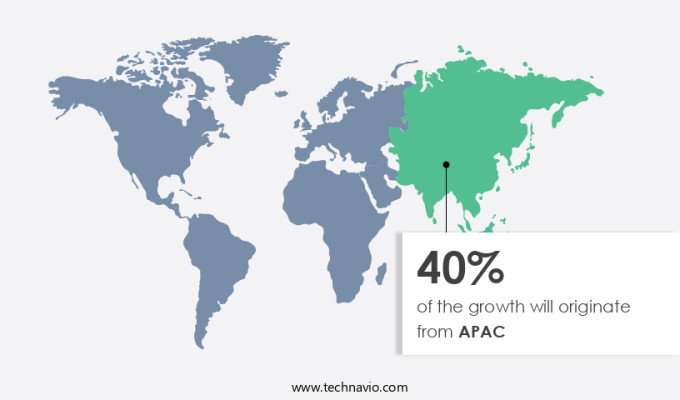

- APAC is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The Asia-Pacific (APAC) region plays a pivotal role in the global Testing, Inspection, and Certification (TIC) market due to its extensive manufacturing sector and rapid industrial advancement. With China being the world's leading manufacturing hub, there exists immense potential for TIC services to ensure product quality, regulatory compliance, and international certification. In 2023, China's equipment manufacturing sector experienced a 6.8% year-on-year growth, surpassing the average industrial production increase. Particularly noteworthy is the significant expansion in the production of solar batteries, new energy vehicles, and power generation equipment, which grew by 54%, 30.3%, and 28.5%, respectively. India's growing automotive and electronics industries, coupled with increasing demands for food safety and pharmaceuticals, further necessitate comprehensive TIC solutions.

Smart sensors, cloud services, blockchain technology, and safety testing services are increasingly being integrated into various industries to enhance product quality and environmental protection. For instance, food packaging companies are adopting smart sensors to monitor CO2 emissions and maintain optimal temperature conditions. In the automotive sector, collision avoidance systems are being certified to ensure road safety. TIC companies are leveraging these technological advancements to offer more value-added services and maintain their competitive edge. The need for TIC services extends beyond manufacturing industries. For example, environmental protection regulations are driving the demand for CO2 emissions testing and certification in various sectors, including energy, transportation, and manufacturing.

As the world transitions towards sustainable energy sources, the importance of TIC services in ensuring the safety and efficiency of renewable energy systems will continue to grow. In conclusion, the TIC market in the APAC region is poised for significant growth, driven by the manufacturing sector's expansion, increasing regulatory requirements, and technological advancements. TIC companies that can offer innovative solutions incorporating the latest technologies, such as smart sensors, cloud services, and blockchain technology, will be well-positioned to capitalize on the opportunities presented by this dynamic market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the healthcare sector, certification of medical devices and facilities is essential for patient safety. Testing services are a third essential component of the ITC market. These services involve the evaluation of products, processes, or systems to determine their performance, safety, and compliance with regulations. For instance, testing for CO2 emissions in the energy and utilities sector helps assess the environmental impact of power generation. In the consumer electronics industry, testing for safety and performance is crucial to ensure consumer protection. The ITC market continues to evolve, with advancements in technology driving innovation. For example, the integration of blockchain technology in ITC can enhance transparency, traceability, and security.

This technology can be particularly useful in industries such as food packaging and smart sensors, where ensuring the authenticity and integrity of products is crucial. In conclusion, the inspection, testing, and certification market plays a vital role in ensuring the quality, safety, and compliance of various products and services across diverse industries. It encompasses inspection services, certification, and testing services, and continues to evolve with technological advancements. By maintaining rigorous standards and regulations, the ITC market helps protect consumers, the environment, and the integrity of industries.

What are the key market drivers leading to the rise in adoption of Testing, Inspection, And Certification Market ?

Stringent regulatory requirements is the key driver of the market.

- In the testing, inspection, and certification (TIC) market, stringent regulations play a crucial role in driving growth. These regulations prioritize product safety, quality, and environmental compliance, safeguarding consumers and the environment. On November 9, 2022, the European Commission proposed the Euro 7 emissions standard, which aims to decrease air pollution from new vehicles, including light- and heavy-duty models. This standard expands vehicle emissions regulations, introduces global tire and brake emissions standards, and sets new procedures and battery durability limits to facilitate the transition to electrification. Given the comprehensive nature of these regulations, TIC services are essential to ensure compliance and maintain vehicle safety and performance.

- Advancements in technology are also transforming the TIC market. Blockchain technology is being integrated into TIC processes to enhance data security and traceability. Robotic process automation, machine learning, and artificial intelligence are streamlining certification processes and improving efficiency. Digital twins are being utilized to simulate and test products in a virtual environment, reducing the need for physical testing and minimizing costs. These technological innovations are revolutionizing the TIC industry, making it more efficient and effective. In conclusion, the TIC market is experiencing significant growth due to stringent regulatory requirements and technological advancements. The Euro 7 emissions standard is a prime example of the comprehensive regulations driving the need for rigorous TIC services.

What are the market trends shaping the Testing, Inspection, And Certification Market?

New testing, inspection, and certification solutions launches by vendors is the upcoming trend in the market.

- The Testing, Inspection, and Certification (TIC) market is experiencing a notable trend as companies introduce innovative products and offerings to cater to industry requirements. This trend is fueled by the increasing emphasis on quality, safety, and regulatory compliance in sectors such as logistics, healthcare services, consumer goods, renewable energy, energy and utilities, oil and gas, and Compression Stress Relaxation. On January 3, 2024, SGS, a leading TIC services provider, unveiled its new Rail Services webpage. This platform highlights a wide range of solutions designed for manufacturers, operators, and suppliers within the rail industry's supply chain. SGS's extensive expertise encompasses quality, safety, and sustainability, providing services for rolling stock, signaling systems, energy, and infrastructure.

- The webpage offers in-depth information on services like NOBO/DEBO, RAMS, and cybersecurity, enabling stakeholders to effectively manage intricate rail projects from inception to maintenance, ensuring optimal performance and safety.

What challenges does Testing, Inspection, And Certification Market face during the growth?

High costs of testing, inspection, and certification services is a key challenge affecting the market growth.

- The testing, inspection, and certification (TIC) market plays a crucial role in ensuring the quality, safety, and compliance of various industries, including computing, cybersecurity, and transportation. However, the high cost of these services can pose a challenge, especially for small and medium-sized enterprises (SMEs). For instance, quarterly certification fees in countries like Germany, France, and the United States can range from USD500 to USD1000. In Australia, SGS SA, a leading TIC service provider, offers electrical product certification services, with fees ranging from USD370 to USD700 for different types of applications and modifications. These costs can be a significant financial burden for companies seeking to ensure regulatory compliance.

- Element Materials Technology, another prominent TIC service provider, offers a range of services, including non-destructive testing, material testing, and calibration services. In the realm of computing, TIC services are essential for ensuring the security and reliability of hardware and software. Cybersecurity testing is crucial in the digital age to protect sensitive data and prevent cyber-attacks. In the emerging fields of augmented reality and virtual reality, TIC services are vital for ensuring the safety and quality of these technologies. QR code inspection is another application of TIC services, ensuring the authenticity and accuracy of product information. In conclusion, the TIC market plays a vital role in various industries, from computing and cybersecurity to transportation and emerging technologies like augmented reality and virtual reality.

- The high cost of these services can be a challenge, particularly for SMEs, but the importance of ensuring regulatory compliance and product quality cannot be overstated. TIC service providers like SGS SA and Element Materials Technology offer a range of services to meet the diverse needs of industries, from electrical product certification to non-destructive testing and cybersecurity testing.

Exclusive Customer Landscape

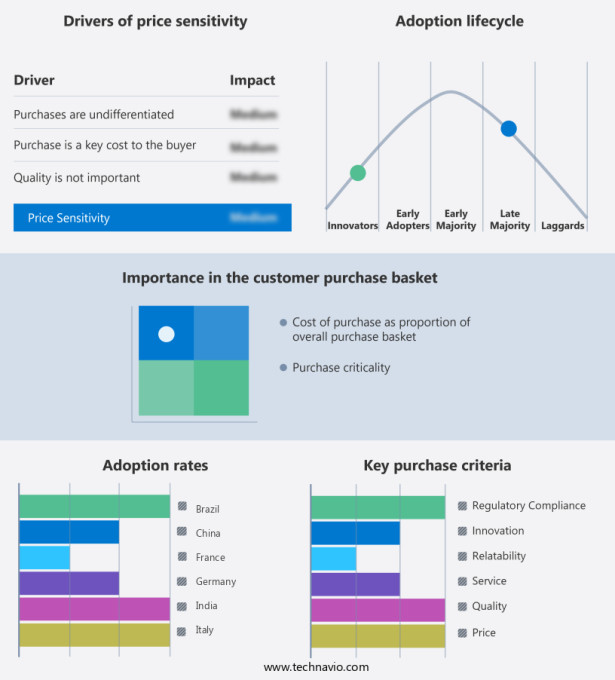

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ALS Ltd. - Our company provides comprehensive testing, inspection, and certification solutions for various industries. These services encompass environmental testing, non-destructive testing, and certification for sectors such as mining, industrial equipment, and consumer products in the United States. By ensuring adherence to stringent quality standards, we help businesses mitigate risks, enhance safety, and maintain regulatory compliance. Our expertise lies in delivering accurate and reliable results, enabling our clients to bring their products to market with confidence. With a focus on precision and efficiency, we contribute to the success of businesses in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALS Ltd.

- Applus Services Technologies SL

- ATIC Co. Ltd.

- British Standards Institution

- Bureau Veritas SA

- CIS Commodity Inspection Services

- Cotecna Inspection SA

- DEKRA SE

- Element Materials Technology Group Ltd.

- Eurofins Scientific SE

- Intertek Group Plc

- Mistras Group Inc.

- Mitra S.K Pvt Ltd.

- OCA Global Corporate Services S.A.

- Peterson and Control union

- QIMA Ltd.

- SGS SA

- TUV NORD AG

- TUV SUD AG

- UL Solutions Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses various industries and applications, ensuring safety, quality, and compliance. This market plays a crucial role in protecting consumers and the environment. Safety testing services cover various sectors, including transportation and logistics, where collision avoidance systems and CO2 emissions are essential. In the realm of food and beverage, food safety and digital inspection using integrated sensors are paramount. Environmental protection is another significant aspect, with certification processes for renewable energy and energy and utilities, as well as chemicals and mining, ensuring sustainable practices. In the healthcare sector, consumer goods, and pharmaceuticals, certification is essential for health safety measures and consumer confidence.

Technological advancements, such as blockchain supply chain technology, robotics, machine learning, and artificial intelligence, are revolutionizing the testing, inspection, and certification landscape. Applications include data security, cybersecurity, and QR codes. The use of digital twins, computing, and augmented reality/virtual reality enhances quality monitoring and complex logistics management. In-house testing and outsourced services cater to industries like agriculture and food, consumer electronics, aerospace and defense, and waste management. Routine inspection and certification are essential for maintaining supply chain activity and ensuring CSR initiatives in various sectors.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

211 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.9% |

|

Market growth 2024-2028 |

USD 47.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.6 |

|

Key countries |

US, China, Germany, Japan, UK, India, South Korea, France, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -