US Automotive Service Market Size 2026-2030

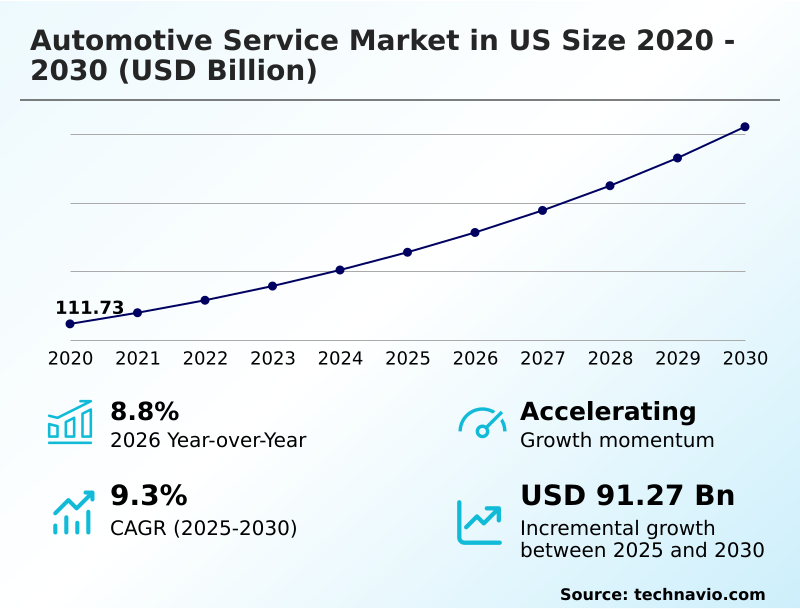

The us automotive service market size is valued to increase by USD 91.27 billion, at a CAGR of 9.3% from 2025 to 2030. Mainstreaming of vehicle longevity and industrialization of maintenance protocols for aging domestic fleet will drive the us automotive service market.

Major Market Trends & Insights

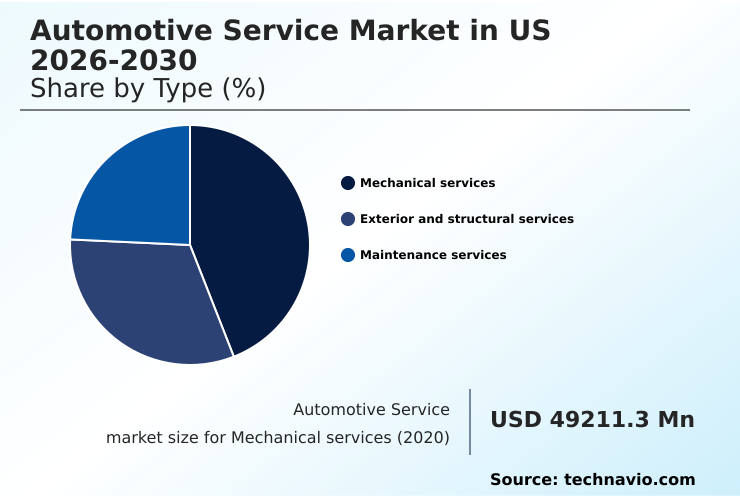

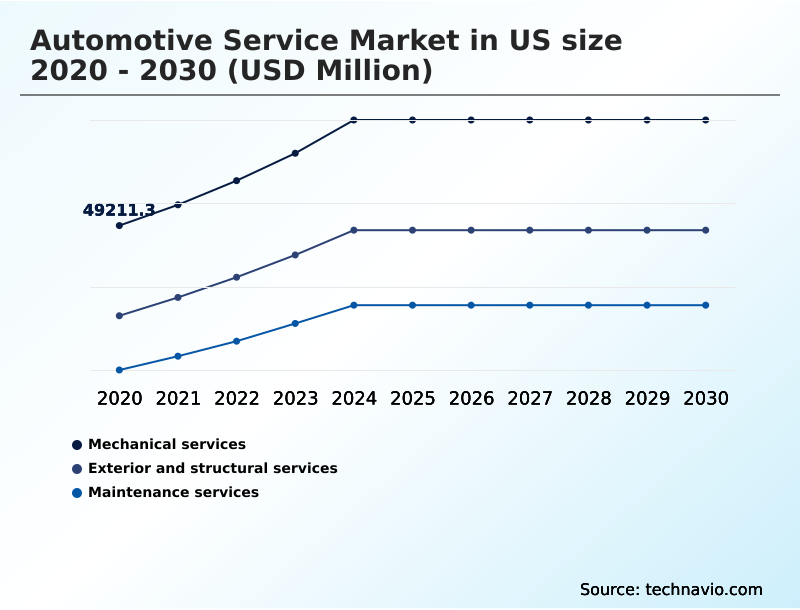

- By Type - Mechanical services segment was valued at USD 65.37 billion in 2024

- By Vehicle Type - Passenger cars segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 143.36 billion

- Market Future Opportunities: USD 91.27 billion

- CAGR from 2025 to 2030 : 9.3%

Market Summary

- The automotive service market in US is undergoing a significant transformation, driven by the dual pressures of an aging vehicle fleet and the rapid technological evolution of modern cars. The extension of vehicle lifecycles necessitates a greater focus on preventative maintenance and complex mechanical repairs, creating steady demand for both independent shops and OEM dealership networks.

- Concurrently, the proliferation of software-defined vehicles requires a fundamental shift in service capabilities. Technicians must now possess software-centric proficiency to perform tasks ranging from advanced driver-assistance systems (ADAS) calibration to electronic control unit (ECU) flashing. The rise of electric vehicles introduces further complexity, demanding expertise in high-voltage battery management and thermal runaway risk management to ensure safety.

- This technical evolution is creating a notable skills gap, challenging the industry's capacity to meet demand. For instance, a service center managing a fleet of connected vehicles can leverage on-board sensor data for predictive mechanical interventions, scheduling repairs before a component fails.

- This approach minimizes vehicle downtime and improves operational efficiency, showcasing the strategic importance of investing in both diagnostic technology and continuous technician training to maintain a competitive edge in a dynamic service landscape.

What will be the Size of the US Automotive Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Automotive Service Market Segmented?

The us automotive service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Mechanical services

- Exterior and structural services

- Maintenance services

- Vehicle type

- Passenger cars

- Light commercial vehicles

- Two wheelers

- Heavy commercial vehicles

- Propulsion

- Internal combustion engine

- Electric

- Geography

- North America

- US

- North America

By Type Insights

The mechanical services segment is estimated to witness significant growth during the forecast period.

The mechanical services segment is defined by a dual focus on extending the life of an aging vehicle fleet and mastering the complexities of modern vehicle architectures.

Effective aging fleet maintenance protocols necessitate a shift toward intensive preventative maintenance programs, moving beyond simple routine vehicle maintenance.

This trend benefits both franchise general repair centers and independent repair facilities that offer specialized powertrain specialized service and general auto repair.

The integration of advanced driver assistance systems demands significant investment in OEM diagnostic tools for calibration and repair, distinct from traditional collision repair services.

Service providers that leverage these tools report a notable increase in customer satisfaction, with some achieving a 5% improvement in first-time repair success rates by accurately diagnosing wear-and-tear component lifecycles.

The Mechanical services segment was valued at USD 65.37 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the automotive service market increasingly revolves around balancing operational costs with technological investment. The impact of ADAS calibration on repair costs is a significant factor, as it requires specialized equipment and training, affecting profitability for both dealerships and independent shops.

- A key debate is the comparison of mobile vs shop-based wheel repair services, where mobile units offer lower overhead but may have limitations in handling complex structural jobs.

- For fleet operators, implementing predictive maintenance for commercial vehicle fleets using telematics data is proving essential, with some fleets reporting up to a 20% reduction in unplanned downtime compared to those using reactive service models. The choice between OEM vs aftermarket parts for structural repairs remains a critical consideration, balancing cost against warranty and fitment guarantees.

- Furthermore, the high cost of technician training for high-voltage DC isolation procedures is a barrier to entry for many smaller businesses wanting to service electric vehicles. Securing data access rights for independent repairers is a pivotal regulatory issue influencing the competitive landscape.

- Finally, evaluating the ROI of digital shop management software and understanding software-defined vehicle diagnostic tool costs are crucial for ensuring long-term viability in a rapidly evolving market.

What are the key market drivers leading to the rise in the adoption of US Automotive Service Industry?

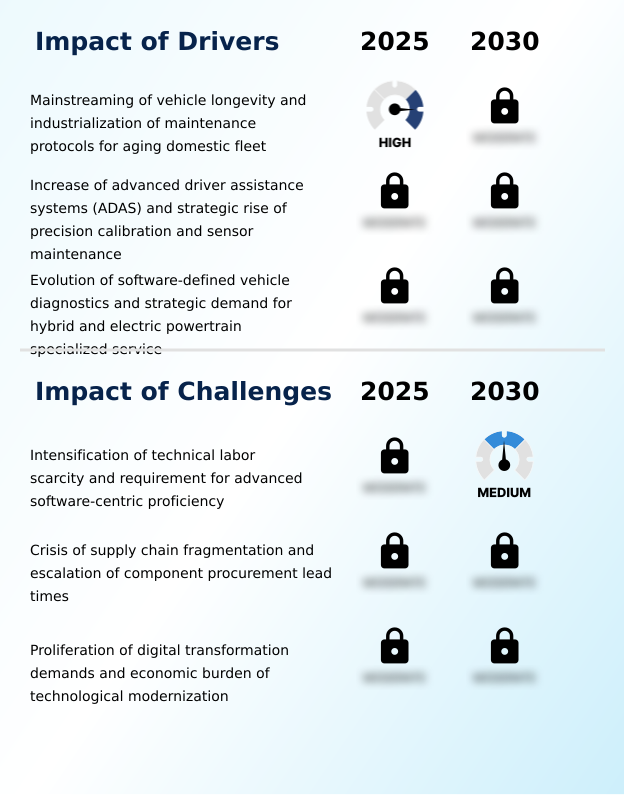

- The mainstreaming of vehicle longevity, driven by consumer behavior, is industrializing maintenance protocols for the aging domestic fleet.

- Market growth is primarily driven by the extended longevity of vehicles, which has industrialized maintenance protocols.

- The average vehicle age reaching a new record compels owners to seek out-of-warranty vehicle repairs, fueling growth for providers of independent aftermarket (IAM) parts and tire replacement services.

- The rise of connected car telematics and remote diagnostic monitoring allows for predictive mechanical interventions based on real-time on-board sensor data, improving customer service index (CSI) scores by over 5% for proactive shops.

- Furthermore, the convenience offered by mobile service fleets and digital service scheduling platforms is reshaping consumer expectations, forcing traditional service centers to adapt their business models to maintain market share against more agile competitors.

What are the market trends shaping the US Automotive Service Industry?

- A primary market trend is the standardization of specialized xEV safety certifications. This move establishes a baseline for high-voltage technical competency across the service industry.

- Key market trends are centered on the electrification and digitalization of vehicle service. The institutionalization of high-voltage safety standards is driving demand for technician safety certifications and advanced competency in high-voltage battery management and EV battery diagnostics. This structural realignment creates a divide between shops equipped for the future and those limited to legacy repairs.

- Concurrently, the adoption of digital shop management ecosystems is streamlining operations, enabling a shift from reactive to proactive service models. The integration of software-defined vehicle diagnostics is becoming standard, requiring shops to invest in tools capable of handling complex electronic systems.

- This evolution, which includes the strategic integration of mobile repair firm operations, is transforming service technicians into high-voltage systems architects, future-proofing the domestic service infrastructure.

What challenges does the US Automotive Service Industry face during its growth?

- A key industry challenge is the intensifying scarcity of technical labor, compounded by the rising requirement for advanced, software-centric proficiency.

- The primary market challenge is a critical human capital crisis, where the demand for software-centric proficiency outpaces the available talent pool. Servicing modern vehicles requires expertise in advanced driver-assistance systems (ADAS) calibration and electronic control unit (ECU) flashing, skills that are scarce.

- This technician shortage, affecting 37% of the sector, is exacerbated by the technological modernization burden and prolonged component procurement lead times. The ongoing debate over vehicle data sovereignty and access to proprietary telematics further complicates operations for independent shops.

- Without a significant investment in ASE-certified mechanical repairs training programs that emphasize digital literacy and access to vehicle-generated data, service providers face reduced capacity and margin compression.

Exclusive Technavio Analysis on Customer Landscape

The us automotive service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us automotive service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Automotive Service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us automotive service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alloy Wheel Repair Specialists - Analyzes mobile and shop-based wheel repair, refinishing, and custom coloring, offering specialized solutions for the automotive aftermarket and fleet management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alloy Wheel Repair Specialists

- AutoNation Inc.

- Belle Tire Distributors Inc.

- Bridgestone Corp.

- Caliber Collision

- D Ieteren Group SA NV

- Driven Brands Holdings Inc.

- Drivers Tire and Service Center

- Hyundai Motor Co.

- Icahn Automotive Group LLC

- Mavis Tires and Brakes

- Michelin

- Monro Inc.

- Nissan Motor Co. Ltd.

- Shell plc

- The Goodyear Tire and Rubber Co.

- Toyota Motor Corp.

- USA Automotive

- Walmart Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us automotive service market

- In October 2024, The Right to Equitable and Professional Auto Industry Repair (REPAIR) Act was advanced by the House Energy and Commerce Committee, aiming to mandate OEM data access for independent repairers.

- In January 2025, Driven Brands Holdings Inc. announced a strategic restructuring of its service segments, including Take 5 Oil Change and Meineke, to enhance operational transparency across its North American network.

- In February 2025, Caliber Collision appointed an interim Chief Financial Officer to guide its national expansion strategy following the recent integration of mobile repair firm Car Body Lab.

- In April 2025, Toyota Motor Corp. launched an enhanced certified pre-owned program that includes a comprehensive two-year maintenance plan, aiming to boost service retention at its dealership network.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Automotive Service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 187 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.3% |

| Market growth 2026-2030 | USD 91267.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.8% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive service market in US is defined by the need to manage increasingly complex vehicle technologies. Proficiency in software-defined vehicle diagnostics and advanced driver-assistance systems (ADAS) is no longer optional but a core competency.

- A critical boardroom decision involves allocating capital toward OEM diagnostic tools and continuous training to address the industry's talent gap, where over one-third of shops cite labor shortages as a primary challenge. Expertise in high-voltage battery management and EV battery diagnostics is becoming a key differentiator, as is the ability to manage thermal runaway risk management protocols.

- Service portfolios are expanding to include everything from general auto repair and routine vehicle maintenance to specialized powertrain specialized service and collision repair services. Providers are leveraging mobile service fleets and digital shop management ecosystems to improve efficiency and customer access.

- The debate over vehicle data sovereignty and access to proprietary telematics and on-board sensor data will continue to shape the competitive landscape for those offering wheel alignment services, auto glass replacement, and tire replacement services.

What are the Key Data Covered in this US Automotive Service Market Research and Growth Report?

-

What is the expected growth of the US Automotive Service Market between 2026 and 2030?

-

USD 91.27 billion, at a CAGR of 9.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Mechanical services, Exterior and structural services, and Maintenance services), Vehicle Type (Passenger cars, Light commercial vehicles, Two wheelers, and Heavy commercial vehicles), Propulsion (Internal combustion engine, and Electric) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Mainstreaming of vehicle longevity and industrialization of maintenance protocols for aging domestic fleet, Intensification of technical labor scarcity and requirement for advanced software-centric proficiency

-

-

Who are the major players in the US Automotive Service Market?

-

Alloy Wheel Repair Specialists, AutoNation Inc., Belle Tire Distributors Inc., Bridgestone Corp., Caliber Collision, D Ieteren Group SA NV, Driven Brands Holdings Inc., Drivers Tire and Service Center, Hyundai Motor Co., Icahn Automotive Group LLC, Mavis Tires and Brakes, Michelin, Monro Inc., Nissan Motor Co. Ltd., Shell plc, The Goodyear Tire and Rubber Co., Toyota Motor Corp., USA Automotive and Walmart Inc.

-

Market Research Insights

- Market dynamics are shaped by the convergence of aging fleet maintenance protocols and the need for high-voltage technical competency. As over 78% of new vehicle sales remain internal combustion models, the demand for out-of-warranty vehicle repairs at independent repair facilities continues to grow. These shops leverage specialized diagnostic schedules to service a complex mechanical repair landscape.

- However, the industry is undergoing a structural realignment toward servicing electric vehicles, with a push for xEV electrical safety standards. This shift creates a challenge, as nearly 37% of service providers report that a lack of software-centric proficiency is a primary operational hurdle, impacting their ability to compete with franchise general repair centers on advanced diagnostics.

We can help! Our analysts can customize this us automotive service market research report to meet your requirements.

RIA -

RIA -