Advertising Technology (Ad Tech) Software Market Size 2024-2028

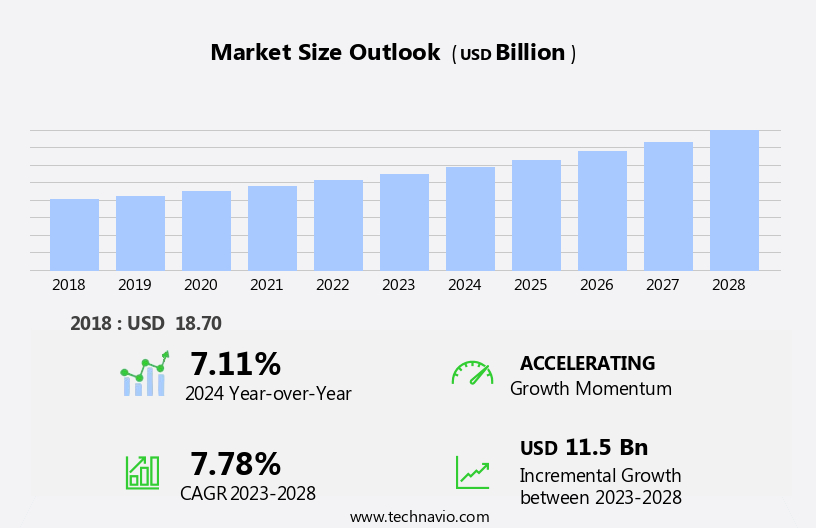

The advertising technology (ad tech) software market size is forecast to increase by USD 11.5 billion at a CAGR of 7.78% between 2023 and 2028.

What will be the Size of the Advertising Technology (Ad Tech) Software Market During the Forecast Period?

How is this Advertising Technology (Ad Tech) Software Industry segmented and which is the largest segment?

The advertising technology (ad tech) software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Retail and consumer goods

- IT and telecom

- BFSI

- Media and entertainment

- Others

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Middle East and Africa

- South America

- North America

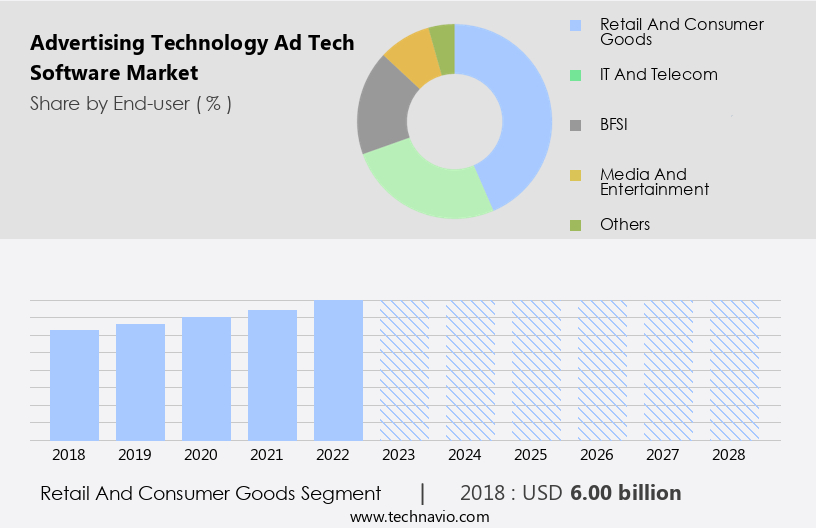

By End-user Insights

- The retail and consumer goods segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, particularly In the retail and consumer goods sector. Online advertising through programmatic platforms, such as Demand-side platforms (DSPs) and Supply-side platforms (SSPs), enables marketers to target consumers based on their behavior and preferences. Ad formats like Display advertising, Digital marketing, and Social media advertising are popular choices for reaching audiences across multiple channels. Technological innovations, including Ad servers, Ad exchanges, and Real-time bidding (RTB), facilitate automated ad buying and selling, increasing efficiency and reducing costs. Publisher platforms and Data management platforms (DMPs) help manage and analyze consumer data for effective audience segmentation, contextual targeting, retargeting, and attribution modeling.

Ad networks and Ad creative optimization tools further enhance campaign performance. Key drivers for the market include the increase in digital ad spend, reach, frequency, and cost-per-click (CPC), as well as the growing importance of viewability, ad targeting, cross-device tracking, and cost-per-action (CPA). However, challenges such as ad fraud detection, ad blocking, and privacy compliance (GDPR, CCPA) necessitate robust Ad Tech solutions. The Ad Tech ecosystem includes various components, such as Ad analytics, Ad measurement, Ad performance, Multichannel advertising, Mobile advertising, Video advertising, Native advertising, and Search engine advertising, all working together to deliver effective advertising solutions.

Get a glance at the Advertising Technology (Ad Tech) Software Industry report of share of various segments Request Free Sample

The Retail and consumer goods segment was valued at USD 6.00 billion in 2018 and showed a gradual increase during the forecast period.

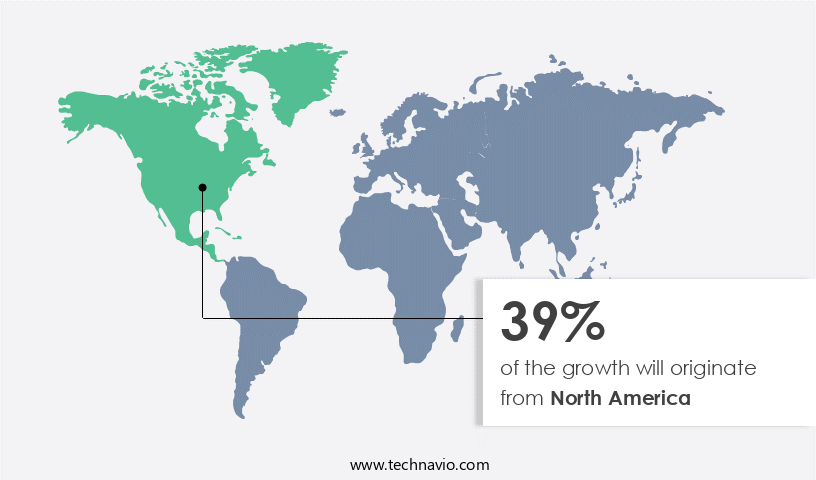

Regional Analysis

- North America is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Ad tech software is experiencing significant growth in North America due to the increasing use of smartphones and robust broadband infrastructure. Mobile and TV advertising saturation In the region is driving market expansion, with mobile ad spending being a major contributor. As consumers spend more time on mobile devices for daily activities and content consumption, marketers are increasingly integrating marketing efforts onto these platforms. US digital advertising investment reached approximately USD209 billion in 2021. Programmatic advertising, including Demand-side platforms (DSPs) and Supply-side platforms (SSPs), are key components of the ad tech ecosystem, enabling real-time bidding (RTB), contextual targeting, audience segmentation, retargeting, and behavioral targeting.

Ad servers, ad exchanges, and ad networks facilitate ad inventory management, conversion tracking, and ad optimization. Marketers utilize Data management platforms (DMPs) for data integration and privacy compliance with regulations such as GDPR and CCPA. Ad tech innovation continues to advance with multichannel advertising, mobile advertising, video advertising, native advertising, social media advertising, search engine advertising, rich media ads, and ad creative optimization. Ad performance measurement and attribution modeling are essential for understanding campaign effectiveness and ROI. Ad spend, reach, frequency, ad budget, and ad analytics are critical metrics for marketers. Ad measurement and performance tracking are crucial for continuous ad optimization and cost management.

Ad fraud detection, cost-per-click (CPC), cost-per-mille (CPM), cost-per-action (CPA), ad blocking, cost-per-acquisition (CPA), ad verification, click-through rate (CTR), impressions, and ad placement are essential aspects of the ad tech ecosystem.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Advertising Technology (Ad Tech) Software Industry?

Increasing internet and smartphone penetration is the key driver of the market.

What are the market trends shaping the Advertising Technology (Ad Tech) Software Industry?

Integration of AI and machine learning is the upcoming market trend.

What challenges does the Advertising Technology (Ad Tech) Software Industry face during its growth?

Growing adoption of ad-blocker solutions is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The advertising technology (ad tech) software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the advertising technology (ad tech) software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, advertising technology (ad tech) software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Adform - Ad Tech software, such as Adform DSP, offers advanced solutions for programmatic advertising. This technology enables campaign planning, audience targeting, and creative optimization tools. By utilizing these features, advertisers can effectively reach their desired audience and maximize campaign performance. Ad Tech software streamlines the digital advertising process, making it more efficient and data-driven. Advertisers can leverage real-time data and insights to inform their ad buying decisions, resulting in more effective and targeted campaigns. Adform DSP is just one example of the innovative Ad Tech software available to advertisers, providing them with the tools they need to succeed in today's digital advertising landscape.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adform

- Adobe Inc.

- Alphabet Inc.

- Amazon.com Inc.

- Criteo SA

- InMobi Pte. Ltd.

- Integral Ad Science Holding Corp.

- Magnite Inc.

- MediaMath Inc.

- Mediaocean LLC

- Meta Platforms Inc.

- Microsoft Corp.

- NextRoll Inc.

- OpenX Technologies Inc.

- PubMatic Inc.

- Skai

- The Trade Desk Inc.

- Tremor International Ltd.

- Twitter Inc.

- WebFX

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Advertising technology, or ad tech, refers to the software and platforms used by advertisers and publishers to buy, sell, and manage digital advertising campaigns. This market is characterized by its constant evolution, driven by advancements in technology and shifting consumer behaviors. At the core of ad tech are two primary components: demand-side platforms (DSPs) and supply-side platforms (SSPs). DSPs enable advertisers to manage and optimize their digital ad campaigns in real-time, while SSPs help publishers sell their ad inventory more efficiently. Programmatic advertising, facilitated by these platforms, has revolutionized the way digital ads are bought and sold. It allows for automated, real-time bidding (RTB) on ad inventory, enabling advertisers to target specific audiences and optimize their ad spend based on real-time data.

The ad tech ecosystem also includes other key players such as ad exchanges, ad servers, and data management platforms (DMPs). Ad exchanges act as marketplaces where buying and selling of ad inventory takes place, while ad servers manage the delivery of ads to the appropriate websites or applications. DMPs help collect, manage, and analyze data to inform targeted advertising strategies. Ad targeting is a critical aspect of ad tech, with various methods such as contextual targeting, audience segmentation, retargeting, and behavioral targeting. Contextual targeting involves serving ads based on the content of the webpage, while audience segmentation targets specific demographics or interests.

Retargeting focuses on reaching users who have previously engaged with a brand, and behavioral targeting uses user data to deliver personalized ads. Another essential aspect of ad tech is ad measurement and analytics. Advertisers use these tools to assess the performance of their campaigns, track conversions, and optimize ad spend. Key performance indicators (KPIs) such as impressions, reach, frequency, click-through rate (CTR), and cost-per-click (CPC) are commonly used to evaluate campaign success. The ad tech market is also influenced by various trends and innovations. Multichannel advertising, which involves delivering consistent brand messages across various channels, is becoming increasingly important.

Mobile advertising, video advertising, native advertising, and social media advertising are all growing areas withIn the market. Ad tech also faces challenges, such as ad fraud detection, ad blocking, and privacy compliance. Ad fraud refers to the use of deceptive practices to generate fraudulent ad impressions or clicks, while ad blocking is a growing concern for advertisers as more users employ ad-blocking software to avoid unwanted ads. Privacy compliance, particularly with regards to regulations like GDPR and CCPA, is a critical issue for ad tech companies to navigate. In conclusion, the ad tech market is a dynamic and complex ecosystem that is constantly evolving to meet the needs of advertisers and publishers.

With a focus on programmatic advertising, ad targeting, and measurement and analytics, ad tech plays a crucial role In the digital advertising landscape. However, it also faces challenges related to ad fraud, ad blocking, and privacy compliance, which require ongoing innovation and adaptation.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.78% |

|

Market growth 2024-2028 |

USD 11.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.11 |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Advertising Technology (Ad Tech) Software Market Research and Growth Report?

- CAGR of the Advertising Technology (Ad Tech) Software industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the advertising technology (ad tech) software market growth of industry companies

We can help! Our analysts can customize this advertising technology (ad tech) software market research report to meet your requirements.

RIA -

RIA -