AI Workflow Orchestration Market Size 2026-2030

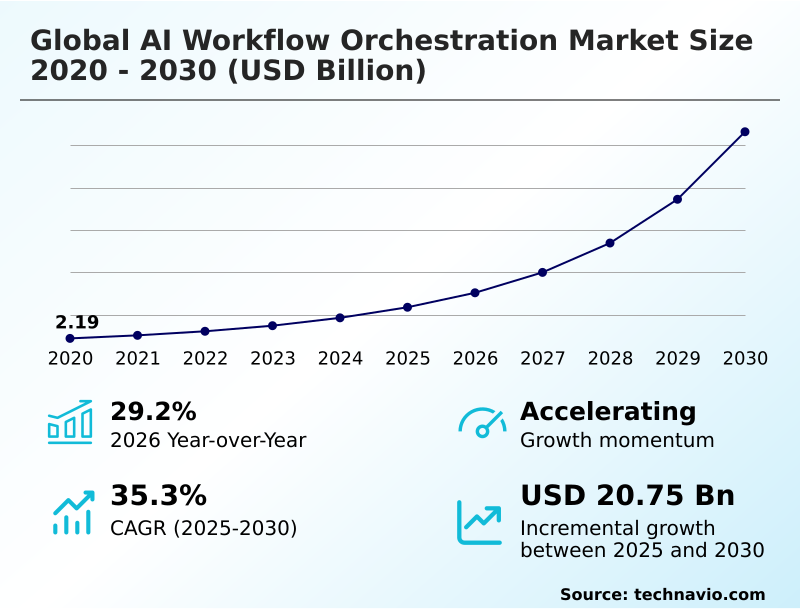

The ai workflow orchestration market size is valued to increase by USD 20.75 billion, at a CAGR of 35.3% from 2025 to 2030. Rise of agentic AI and multi-agent orchestration will drive the ai workflow orchestration market.

Major Market Trends & Insights

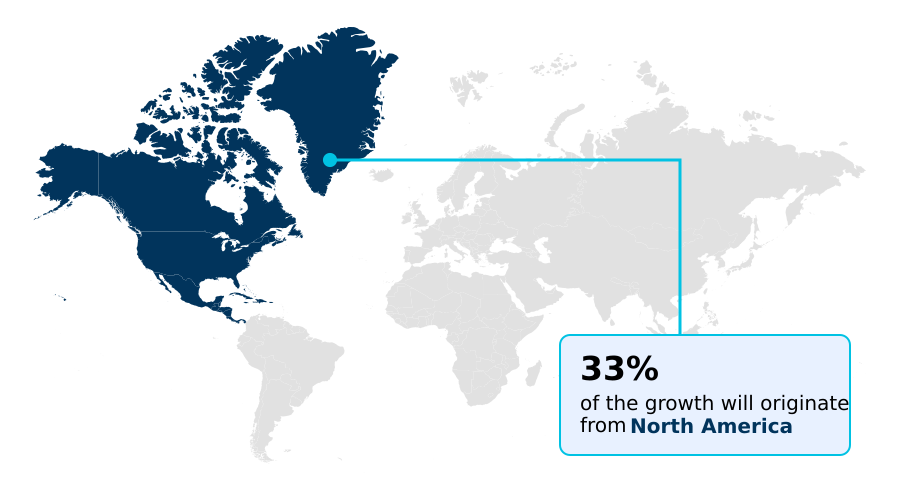

- North America dominated the market and accounted for a 32.6% growth during the forecast period.

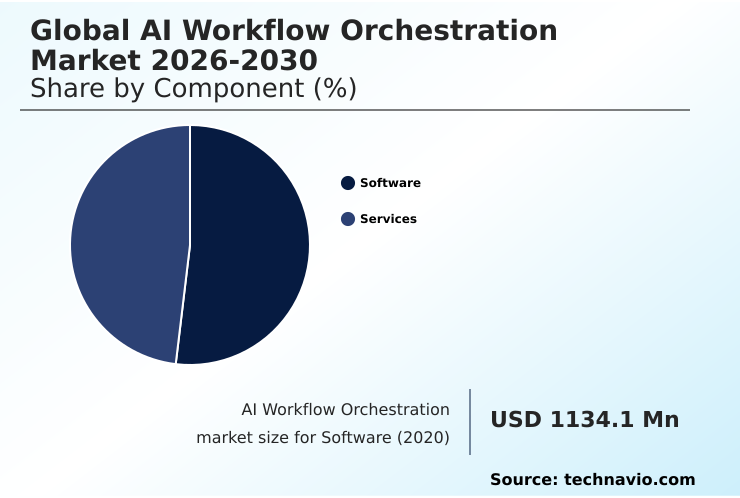

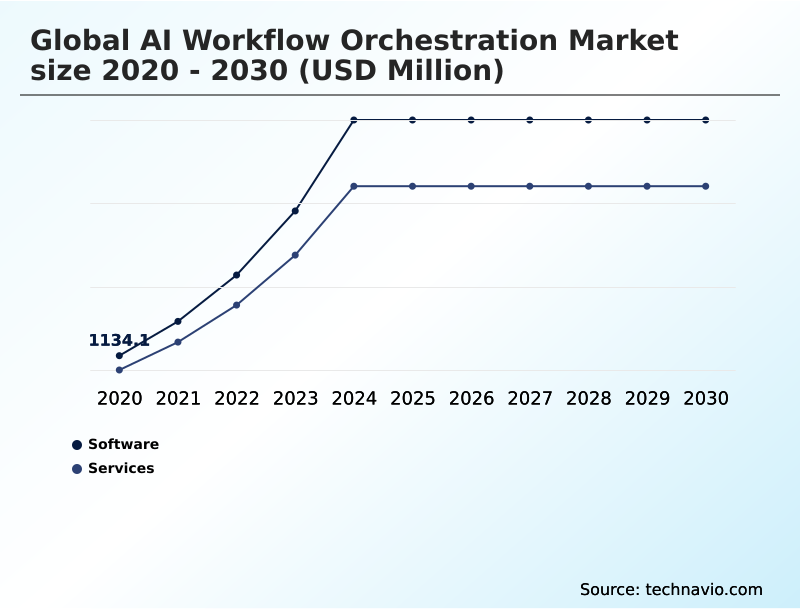

- By Component - Software segment was valued at USD 2.50 billion in 2024

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 24.43 billion

- Market Future Opportunities: USD 20.75 billion

- CAGR from 2025 to 2030 : 35.3%

Market Summary

- The AI workflow orchestration market is undergoing a significant transformation, moving beyond basic automation to manage the end-to-end lifecycle of intelligent systems. This evolution is driven by the need for scalable, reproducible, and governable AI deployments in complex enterprise environments.

- Organizations are adopting these frameworks to coordinate disparate data sources, machine learning models, and computational resources, creating a cohesive operational pipeline. A key trend is the shift toward agentic AI, where autonomous agents perform multi-step reasoning and task execution, necessitating sophisticated orchestration layers for management.

- For instance, in supply chain management, orchestration platforms coordinate predictive models for demand forecasting with automated inventory management systems, ensuring seamless adjustments to market fluctuations without manual intervention. However, the market faces challenges related to integrating modern orchestration tools with legacy infrastructures and a persistent shortage of skilled professionals.

- The increasing regulatory scrutiny, particularly in Europe and North America, also drives demand for platforms with built-in compliance, model governance, and explainability features, ensuring automated decisions remain transparent and ethically sound. This makes orchestration a critical component for institutionalizing AI securely and effectively.

What will be the Size of the AI Workflow Orchestration Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Workflow Orchestration Market Segmented?

The ai workflow orchestration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud-based

- On-premises

- Application

- MT and HT

- MD and I

- DP and FE

- Monitoring and maintenance

- Automated decision-making

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the technological core of the AI workflow orchestration market, offering platforms for managing the entire lifecycle of machine learning models and automated processes.

These solutions provide a centralized, unified control plane for designing and monitoring complex algorithmic pipelines, featuring robust AI governance solutions. The shift toward agentic AI, where autonomous delegation of tasks is common, is a key driver.

Platforms increasingly integrate features for model governance and data lineage tracking. This ensures that even complex multimodal models operate transparently across hybrid cloud orchestration environments.

With tools like kubeflow pipelines for ML workflow orchestration and scalable AI workflow automation, organizations are seeing a more than 15% improvement in deployment speeds, enabling enterprise AI orchestration to move from experiment to production safely and efficiently.

The Software segment was valued at USD 2.50 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Workflow Orchestration Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI workflow orchestration market is diverse, with North America commanding over 32% of the market opportunity, driven by early adoption of advanced automation. This region leads in deploying production-grade AI agents and autonomous AI systems.

Europe's market is shaped by stringent regulations, creating strong demand for solutions emphasizing data sovereignty and compliance, with a focus on hybrid cloud AI workflows and open-source orchestration to avoid vendor lock-in.

The APAC region is the fastest-growing segment, characterized by a focus on mobile-first enterprise workflow orchestration and edge orchestration in manufacturing.

Countries like China are investing heavily in intelligent automation services and AI-native development lifecycles, while India is a hub for AI engineering services.

South America is an emerging market, with adoption accelerating in the financial and agricultural sectors, where intelligent business processes are being modernized.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The AI workflow orchestration market is expanding as organizations implement specialized solutions tailored to specific business functions. For instance, AI workflow orchestration for financial services is crucial for automating fraud detection and algorithmic trading with high precision.

- In parallel, the democratization of development through low-code AI workflow design for business users is empowering departments to create bespoke automation without deep technical expertise. The strategic importance of agentic AI orchestration in supply chain is growing, where it optimizes logistics and inventory in real time, delivering efficiency gains nearly double that of legacy automation systems.

- As regulatory pressures mount, AI workflow orchestration for regulatory compliance becomes non-negotiable, providing auditable data lineage and transparent reporting. In customer-facing roles, multi-agent orchestration for customer service is transforming support centers into proactive, intelligent operations. A major hurdle is integrating AI orchestration with legacy systems, a complex task that requires careful planning and investment.

- The push toward generative AI workflow orchestration at scale is driving demand for platforms that can manage large language models efficiently. To achieve flexibility, AI orchestration for hybrid cloud environments is becoming standard practice, allowing seamless workload management. The operational phase depends on real-time AI workflow monitoring and maintenance to ensure model accuracy and system health.

- Foundational to this is the effective process of managing data pipelines with AI orchestration. Ultimately, the goal is automated decision-making using AI orchestration, while securing AI workflows with automated guardrails ensures these autonomous actions remain safe and aligned with business policies.

What are the key market drivers leading to the rise in the adoption of AI Workflow Orchestration Industry?

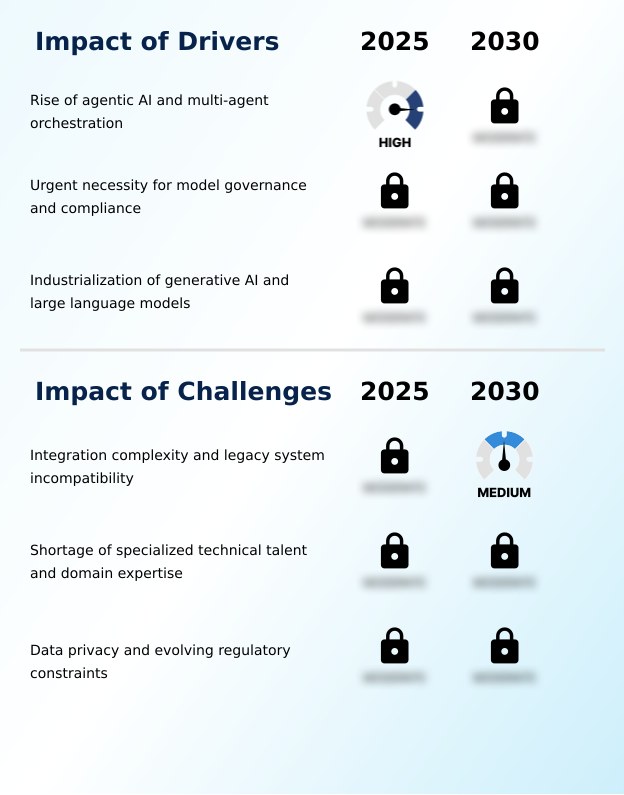

- The rise of agentic AI and the need for multi-agent orchestration are primary drivers, creating demand for platforms that can manage dynamic, non-linear, and autonomous workflows at scale.

- The industrialization of generative AI is a major driver, pushing organizations to adopt solutions for managing retrieval-augmented generation and complex interactions with vector databases. This shift toward production-ready AI agents necessitates platforms that can handle scalable AI workflow automation.

- Another significant driver is the urgent need for model governance and regulatory compliance.

- Orchestration platforms that provide comprehensive data lineage and explainable AI capabilities are in high demand, as they enable companies to meet stringent legal requirements and generate audit reports, reducing compliance risk by over 30%.

- The implementation of automated guardrails within these agent-based workflow systems ensures models operate within safe parameters.

- As enterprises build out AI-native development lifecycles, the ability to automate hyperparameter tuning and manage autonomous AI systems becomes essential for maintaining a competitive edge and operational resilience.

What are the market trends shaping the AI Workflow Orchestration Industry?

- The market is evolving from static, sequential pipelines toward agentic orchestration frameworks. These advanced systems are defined by autonomous delegation capabilities, enabling self-directed adaptation to real-time variables.

- A primary trend is the evolution toward agentic orchestration and multi-agent systems, which enable autonomous delegation of complex tasks. Unlike traditional AI workflow automation, these frameworks allow for dynamic, self-directed processes, with early adopters reporting a 25% increase in operational agility.

- This trend is accompanied by the deep convergence of MLOps integration and DevSecOps convergence, creating unified pipelines for enterprise AI orchestration. The rise of low-code workflow design and natural language interfaces is also democratizing access to ML workflow orchestration, allowing non-technical users to build and manage automated processes.

- Organizations using these intuitive tools for intelligent workflow automation have seen project initiation times drop by up to 40%. The focus on advanced prompt engineering is further refining the capabilities of these systems, making AI pipeline orchestration more precise and effective.

What challenges does the AI Workflow Orchestration Industry face during its growth?

- A key challenge affecting industry growth is the integration complexity and incompatibility of modern orchestration frameworks with entrenched legacy systems, which creates significant technical friction.

- A primary challenge is the technical complexity of integrating modern orchestration platforms with legacy systems, which can increase project timelines by up to 50% for large enterprises. Effective end-to-end AI lifecycle management requires seamless inference engine coordination and state persistence, which is difficult across fragmented IT environments.

- Another constraint is the global shortage of specialized talent capable of managing sophisticated AI-driven orchestration and automated decision-making systems. This skills gap hinders the ability to implement continuous retraining loops and effective model versioning. Furthermore, as organizations adopt serverless computing and multi-modal AI models, ensuring tool-use capabilities and data consistency becomes more complex.

- Many are turning to AI-powered orchestration services and synthetic data generation to accelerate development, yet a lack of unified standards for automated model evaluation remains a significant hurdle to achieving scalable and reliable operations.

Exclusive Technavio Analysis on Customer Landscape

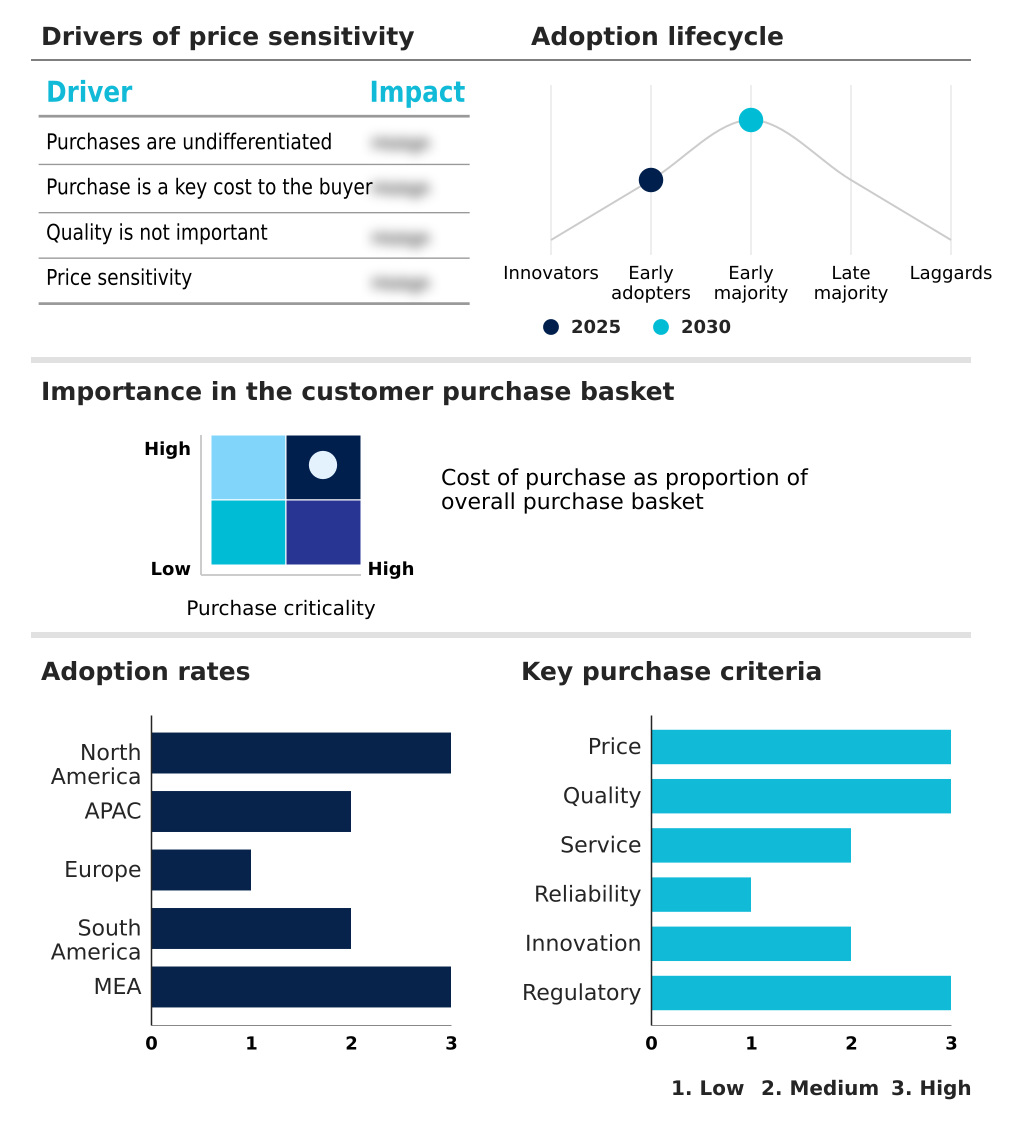

The ai workflow orchestration market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai workflow orchestration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Workflow Orchestration Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai workflow orchestration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Offers scalable AI workflow automation and complete model lifecycle orchestration through a suite of integrated platforms and services for enterprise-wide deployment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Capgemini SE

- Cisco Systems Inc.

- Databricks Inc.

- DataRobot Inc.

- ElixirClaw AI

- Google LLC

- H2O.ai Inc.

- Hewlett Packard Enterprise Co.

- IBM Corp.

- Inngest Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- Oracle Corp.

- Orkes Inc.

- Prefect Technologies Inc.

- SAP SE

- SAS Institute Inc.

- SuperAGI

- Tredence.Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai workflow orchestration market

- In May 2025, IBM Corp. unveiled next-generation agentic AI orchestration capabilities for its watsonx Orchestrate platform, introducing multi-agent coordination and a no-code Agent Builder to simplify agent creation.

- In April 2025, Google LLC launched the Agent2Agent Protocol (A2A) as an open standard to enable AI agents across different platforms to discover, communicate, and coordinate actions, backed by over 50 technology partners.

- In March 2025, Microsoft introduced major updates to Copilot Studio, including the general availability of autonomous agents capable of monitoring events and executing workflows based on natural language instructions without manual intervention.

- In February 2025, SAP SE and Databricks Inc. announced a strategic partnership to embed Databricks technology within the SAP ecosystem, launching the SAP Business Data Cloud to streamline data engineering and AI workloads.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Workflow Orchestration Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 35.3% |

| Market growth 2026-2030 | USD 20746.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 29.2% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI workflow orchestration market is rapidly maturing as organizations institutionalize AI, moving from isolated models to interconnected, multi-agent systems. This shift necessitates sophisticated frameworks that ensure model governance and complete data lineage. A key trend is the convergence of MLOps integration with DevSecOps convergence, creating a unified approach to the AI lifecycle.

- For boardroom decisions, this means prioritizing platforms that offer robust, automated guardrails and policy-based security to mitigate regulatory risk. The technology is evolving toward an agentic AI platform model, where autonomous delegation is standard. We see a clear move to retrieval-augmented generation and advanced prompt engineering managed through kubeflow pipelines and vector databases.

- This has led to a 20% improvement in the accuracy of outputs for complex tasks. This industrialization demands continuous retraining, hyperparameter tuning, and seamless inference engine coordination with state persistence, all while ensuring explainable AI. The rise of low-code workflow design and natural language orchestration is democratizing access, supported by serverless computing, synthetic data generation, and tool-use capabilities for multimodal models.

- The demand for data sovereignty is driving adoption of hybrid cloud orchestration and edge orchestration, with vendors competing via offerings like an AI agent marketplace for production-grade AI agents and open-source orchestration solutions featuring intelligent automation services and cross-application agent logic for enterprise-grade agentic AI.

What are the Key Data Covered in this AI Workflow Orchestration Market Research and Growth Report?

-

What is the expected growth of the AI Workflow Orchestration Market between 2026 and 2030?

-

USD 20.75 billion, at a CAGR of 35.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (Cloud-based, and On-premises), Application (MT and HT, MD and I, DP and FE, Monitoring and maintenance, and Automated decision-making) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rise of agentic AI and multi-agent orchestration, Integration complexity and legacy system incompatibility

-

-

Who are the major players in the AI Workflow Orchestration Market?

-

Amazon.com Inc., Capgemini SE, Cisco Systems Inc., Databricks Inc., DataRobot Inc., ElixirClaw AI, Google LLC, H2O.ai Inc., Hewlett Packard Enterprise Co., IBM Corp., Inngest Inc., Meta Platforms Inc., Microsoft Corp., Oracle Corp., Orkes Inc., Prefect Technologies Inc., SAP SE, SAS Institute Inc., SuperAGI and Tredence.Inc.

-

Market Research Insights

- Market dynamics are shaped by a strategic shift from experimental AI to industrialized intelligent workflow automation. This transition is evident as enterprises implementing end-to-end AI lifecycle management report up to a 30% reduction in model deployment times compared to traditional MLOps approaches. The demand for AI-driven automation tools is intensifying, with adoption of enterprise AI orchestration platforms growing significantly.

- These platforms are becoming unified control planes for both AI pipeline orchestration and broader digital transformation services. Furthermore, organizations leveraging AI-powered orchestration services see a notable improvement in resource optimization, with some achieving a 15% decrease in computational costs through better model and data pipeline management.

- The focus on AI governance solutions and scalable AI workflow automation is critical for navigating compliance and achieving reliable, enterprise-wide AI model lifecycle orchestration.

We can help! Our analysts can customize this ai workflow orchestration market research report to meet your requirements.

RIA -

RIA -