Native Starches Market Size 2024-2028

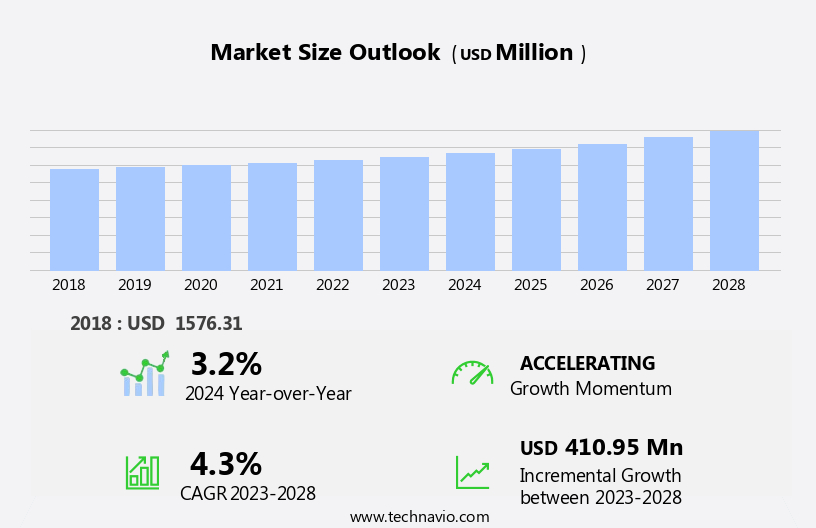

The native starches market size is forecast to increase by USD 410.95 billion at a CAGR of 4.3% between 2023 and 2028.

- The market is driven by the high demand for cost-effective starches derived from plants, such as corn and tapioca. Corn starch, in particular, is widely used due to its affordability and versatility. Another trend in the market is the utilization of native starches in the production of chemical additives and bioplastics, particularly tapioca starch. However, the market faces challenges due to the constant fluctuations in raw material prices, which can impact the profitability of manufacturers. The market for native starches is witnessing significant growth due to the rising demand for cost-effective starches derived from plants like corn and tapioca. Corn starch, which is widely used for its affordability and versatility, is a major contributor to this growth. In addition, the usage of native starches in the production of chemical additives and bioplastics, particularly tapioca starch, is on the rise. However, the market faces challenges due to the constant fluctuations in raw material prices, which can impact the profitability of manufacturers. Producers must closely monitor these price fluctuations and adapt their strategies accordingly to maintain competitiveness.

What will be the Size of the Market During the Forecast Period?

- Native starches, derived from various plants such as corn, wheat, rice, and potato, play a crucial role in the food and non-food industries. These starches, which are unaltered and free from chemical additives, offer several functional qualities that make them an essential ingredient in numerous applications. In the food industry, native starches are widely used in processed goods due to their ease of storage and longer shelf life. The changing lifestyles and rising income levels have led to an increased demand for convenience foods, further boosting the market growth. In the non-food industry, native starches are used as thickening agents, binders, and coating materials in various applications. Organic elements and functional qualities are key drivers for the market. The demand for organic and natural food products is on the rise, and native starches fit perfectly into this trend. Moreover, the ability of native starches to improve texture, provide stability, and enhance the overall quality of food products makes them an attractive option for manufacturers. The carbohydrate content of starches is primarily made up of polysaccharides, which are long chains of glycosidic bonds. The unique properties of these polysaccharides make native starches a versatile ingredient in various industries.

For instance, in the food industry, they are used as thickening agents in sauces, gravies, and desserts. In the non-food industry, they are used as binding agents in adhesives, coatings, and paper sizing. Future trends in the market include the development of new applications in various industries. For example, in the pharmaceutical industry, native starches are used as excipients in tablet coating and capsule filling. In the textile industry, they are used as sizing agents to improve fabric strength and texture. The dominance of corn, wheat, rice, and potato in the market can be attributed to their availability, ease of processing, and functional properties. Corn starch, for instance, is widely used due to its high yield and excellent binding properties. Wheat starch, on the other hand, is known for its high viscosity and is widely used in the food industry as a thickener. The transportation and logistics sector also plays a crucial role in the market. The ability to transport these starches over long distances without deterioration is essential to ensure a consistent supply to various industries. In conclusion, the market is driven by the increasing demand for organic and natural food products, changing lifestyles, and rising income levels. The versatility of native starches, coupled with their ease of storage and longer shelf life, makes them an attractive option for various industries.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Dry

- Liquid

- Application

- Food and beverages

- Industrial

- Feed

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- APAC

By Type Insights

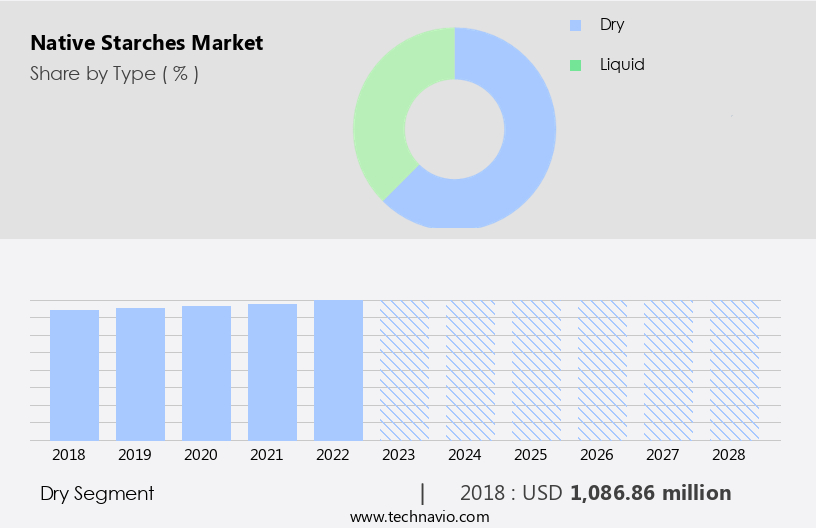

- The dry segment is estimated to witness significant growth during the forecast period.

The market is predicted to expand substantially in the upcoming years, with dry native starches holding the largest market share in 2023. Dry starches are a vital ingredient used in the production of various foods. Native starches, derived from natural sources like corn, wheat, rice, potato, cassava, and others, offer numerous advantages and are widely employed across industries, including food, paper, cosmetics, personal care, and textiles. In the personal hygiene and cosmetics sector, native starches serve as a versatile additive, enhancing texture and improving product performance. The increasing consumer preference for processed foods and the growing demand for natural ingredients are key factors driving the growth of the market.

Get a glance at the market report of share of various segments Request Free Sample

The Dry segment was valued at USD 1.08 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

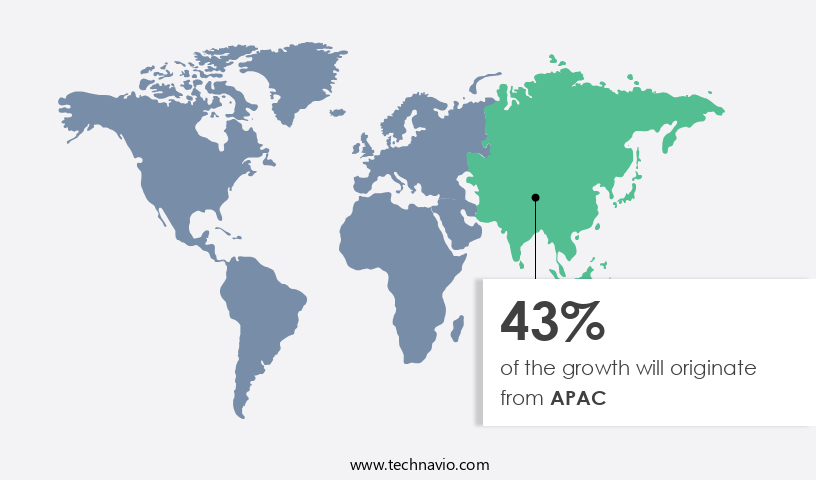

- APAC is estimated to contribute 43% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The native starch market in the Asia Pacific region is poised for significant growth in the coming years. Two key countries, India and China, are driving this progress due to their high demand for native starch. India, with its strong agricultural sector, presents a promising market for the global native starch industry. The Indian food processing industry offers ample opportunities for native starch utilization, thanks to increasing government initiatives. For instance, the Ministry of Food Processing Industries (MoFPI), a government body in India, has assigned projects to local companies to establish starch-based food parks. These initiatives are expected to boost the demand for native starch in the region.

According to quantitative analysis, the market is projected to expand at a steady pace, offering investment pockets for businesses looking to capitalize on these opportunities. Future estimations suggest that the native starch market in APAC will continue to be a significant contributor to the global market. Key players in the industry include Market Research Store, TechSci Research, and Fact.MR, among others. Companies are advised to keep abreast of market trends and opportunities to maximize their growth potential in this sector.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Native Starches Market?

High demand for corn starch as less expensive starch is the key driver of the market.

- The market is experiencing significant growth due to the increasing demand for corn starch in both the food products sector and the non-food industry. Corn starch's functional qualities, including its ability to thicken and bind, make it a popular choice for various applications. In the food industry, corn starch is frequently used as a replacement for wheat in gluten-free food products. This is because corn starch contains less gluten than wheat, making it a preferred option for those with gluten sensitivities. Furthermore, the abundance of corn, particularly in North America, contributes to the growth of the market.

- Additionally, the price of corn starch is generally lower than that of other starches, such as tapioca, making it a cost-effective choice for manufacturers. Looking ahead, future trends in the market include the increasing demand for organic elements and modified food starches. Organic starches are gaining popularity due to their health benefits, while modified food starches offer improved functional qualities for various industries. Overall, the market is expected to continue growing as demand for these versatile carbohydrates increases.

What are the market trends shaping the Native Starches Market?

The usage of tapioca in bioplastics is the upcoming trend in the market.

- Native starches, derived from various plants, serve as the foundation for the production of biodegradable bioplastics. These bioplastics are eco-friendly alternatives to traditional plastics, as they can be decomposed by microorganisms. Among the different types of bioplastics, starch-based bioplastics are the most widely used. These bioplastics are manufactured from natural or modified starches, such as potato, corn, wheat, and tapioca. Tapioca, a common starch source, enhances the degradability of bioplastics due to its stable granules that decompose at elevated temperatures.

- The granules maintain their structure when mixed with polymers at high temperatures and pressure. Consequently, bioplastics derived from tapioca are odorless, smooth, and transparent. Chemical additives may be incorporated into these starch-based bioplastics to improve their properties, such as water resistance and heat stability. The transportation and application of these native starch-derived bioplastics can contribute significantly to the reduction of carbon emissions and the circular economy.

What challenges does the Native Starches Market face during its growth?

The constant fluctuation in raw material prices is a key challenge affecting market growth.

- The native starch market in the US has experienced price fluctuations for raw materials used in the production of processed starch derivatives. These price changes are not solely influenced by availability but also by natural market conditions. Producers of native starch consider the cost of acquiring raw materials to manufacture native starch derivatives. Native starch serves as a crucial ingredient in the creation of starch derivatives. The unpredictability of raw material prices can cause uncertainty among market companies regarding pricing for their native starch derivatives. Additionally, this volatility may result in increased starch prices to secure substantial profit margins. Category-wise insights reveal that segment dominance varies, with ease of storage and longer shelf life being significant factors.

- Understanding these trends and market dynamics can aid businesses in making informed decisions and staying competitive in the evolving market landscape. The native starch industry's future growth is influenced by changing lifestyles and rising income levels, making it an essential sector for businesses and investors.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMYLCO Group of Companies

- Archer Daniels Midland Co.

- Cargill Inc.

- Euroduna Food Ingredients GmbH

- Everest Starch India Pvt. Ltd.

- Gulshan Polyols Ltd.

- Ingredion Inc.

- KMC

- Manildra Flour Mills Pty. Ltd.

- Roquette Freres SA

- Royal Avebe

- SPAC Starch Products India Pvt. Ltd.

- Sudzucker AG

- Tate and Lyle PLC

- Tereos Participations

- Thai Flour Mill Industry Co. Ltd.

- Universal Biopolymers

- WPPZ S.A.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Native starches are derived from various plants such as corn, wheat, rice, potato, and cassava, and are a crucial component in both the food and non-food industries. In the food sector, they serve as functional qualities like thickening agents, dough-binding agents, and stabilizers in processed goods. In the non-food industry, native starches find applications in various sectors like the pet food industry and the paper industry. The changing lifestyles and rising income levels have led to an increase in demand for convenience food products, driving the market growth. Organic elements and modified starches are gaining popularity due to their ease of storage and longer shelf life, making them preferred choices for manufacturers. Native starches are polysaccharides made up of glycosidic bonds, and their usage extends beyond food applications.

Moreover, they are used as thickening agents, stabilizers, and binders in various industries. Modified starches undergo chemical processes to enhance their functional properties, making them suitable for specific applications. Future trends indicate a shift towards the use of natural and organic starches in response to consumer preferences for healthier food options. The market for native starches is segmented based on sources, applications, and regions. Corn and wheat starches dominate the market due to their ease of availability and versatility. The transportation and logistics sector also contributes significantly to the market, as they are essential for the production of various industrial products. The study of the market provides future estimations, investment pockets, and market opportunities for stakeholders.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

154 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.3% |

|

Market growth 2024-2028 |

USD 410.95 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.2 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -