Paper And Paperboard Container And Packaging Market Size 2026-2030

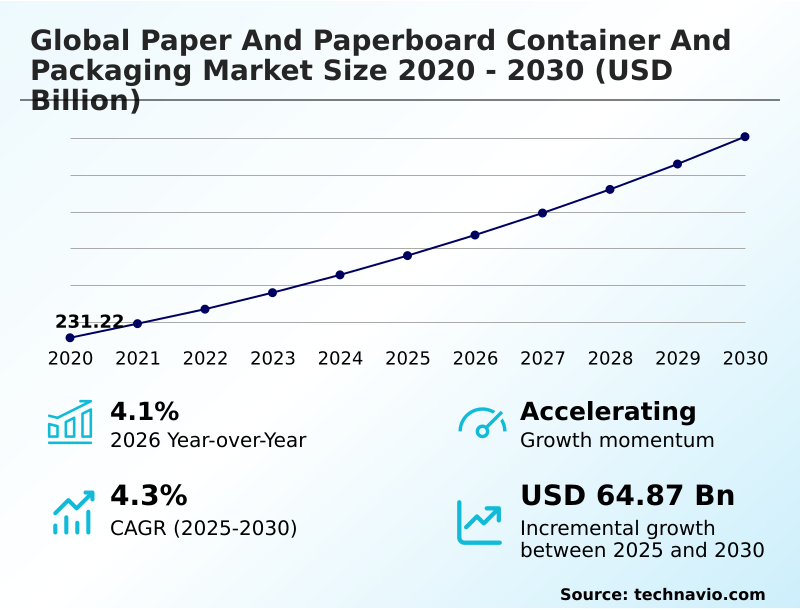

The paper and paperboard container and packaging market size is valued to increase by USD 64.87 billion, at a CAGR of 4.3% from 2025 to 2030. Pervasive shift toward sustainable and circular packaging solutions will drive the paper and paperboard container and packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 39.9% growth during the forecast period.

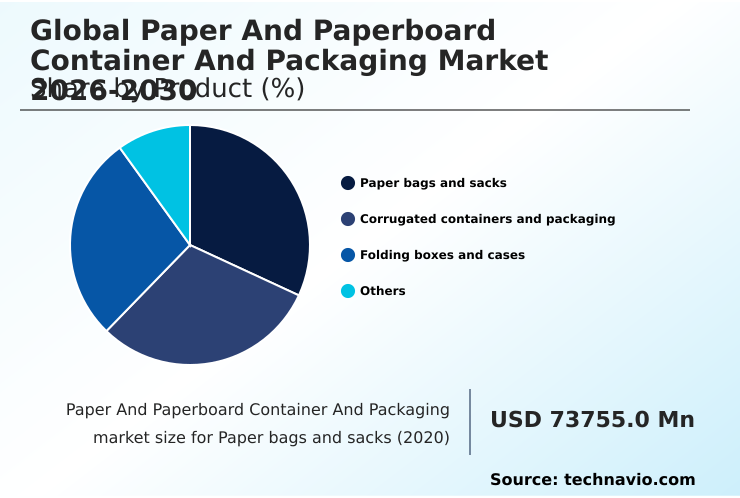

- By Product - Paper bags and sacks segment was valued at USD 85.49 billion in 2024

- By End-user - Food and beverages segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 109.67 billion

- Market Future Opportunities: USD 64.87 billion

- CAGR from 2025 to 2030 : 4.3%

Market Summary

- The paper and paperboard container and packaging market is undergoing a significant structural shift, driven by a global push toward sustainability and the relentless expansion of digital commerce. This transition compels industries to replace conventional plastics with high-performance, fiber-based alternatives that ensure both product protection and environmental responsibility.

- Key trends include the development of advanced bio-based coatings that enhance the barrier properties of food contact materials, making them suitable for perishable goods while maintaining recyclability. Simultaneously, innovations in digital printing are enabling hyper-customization, allowing brands to create a unique unboxing experience.

- For instance, a beverage company can now use lightweight paperboards with high-graphic, on-demand printing for seasonal promotions, reducing material usage and waste. However, the industry grapples with raw material price volatility and competition from flexible plastics, which can offer cost and weight advantages.

- Balancing performance, cost, and ecological impact, particularly in the paperboard converting process for formats like corrugated board and folding cartons, remains a central strategic challenge for all stakeholders. The ongoing development of repulpable materials and molded fiber technology is crucial for expanding applications and solidifying paper's role in a circular economy.

What will be the Size of the Paper And Paperboard Container And Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Paper And Paperboard Container And Packaging Market Segmented?

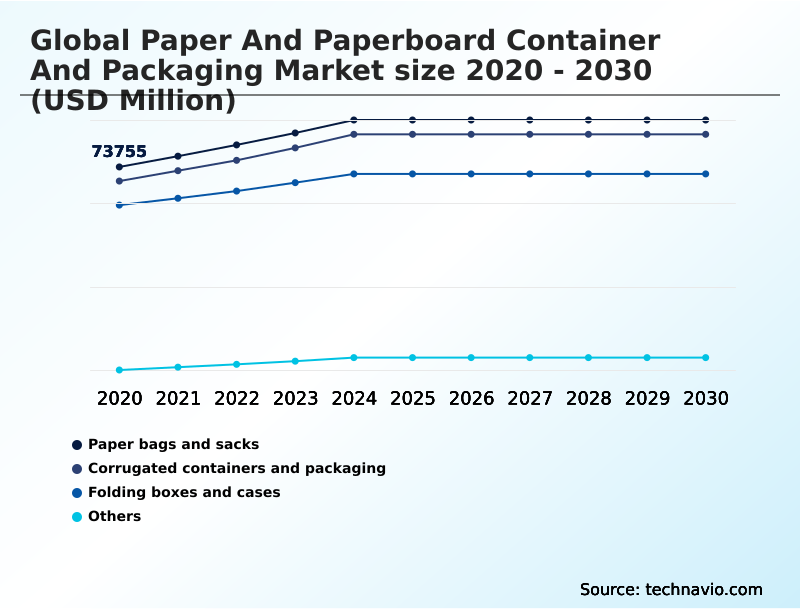

The paper and paperboard container and packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Paper bags and sacks

- Corrugated containers and packaging

- Folding boxes and cases

- Others

- End-user

- Food and beverages

- Industrial products

- Healthcare

- Others

- Material

- Virgin paperboard

- Recycled paperboard

- Packaging

- Primary packaging

- Secondary packaging

- Tertiary packaging

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- Italy

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The paper bags and sacks segment is estimated to witness significant growth during the forecast period.

The paper bags and sacks segment is seeing a significant resurgence, driven by a widespread move away from single-use plastics toward sustainable packaging solutions.

This category, which includes both retail bags and heavy-duty multi-wall paper sacks, is valued for its foundation in renewable cellulose-based materials and inherent biodegradability.

Modern engineering has improved moisture barrier effectiveness by over 30%, enabling these products to deliver superior packaging performance and integrity.

Manufacturers utilize high-strength kraft paper from sources like virgin fiber paperboard and unbleached kraft to create repulpable materials that fit into circular economies.

This focus on renewable packaging materials ensures that paper sacks offer a reliable and ecologically responsible choice for consumers demanding recyclable packaging.

The Paper bags and sacks segment was valued at USD 85.49 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 39.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Paper And Paperboard Container And Packaging Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape is led by the APAC region, which is projected to contribute nearly 40% of incremental growth, driven by demand for e-commerce packaging and plastic-free packaging.

In this region, a focus on sustainable sourcing of pulp and paperboard is paramount. Europe, with a growth rate of 4.4%, emphasizes extended producer responsibility, pushing innovations in recyclable packaging, including high-barrier paper for food contact materials.

North America focuses on recycled paperboard and molded fiber technology to meet sustainability targets.

The demand for consumer board and corrugated board remains strong across all regions, with companies investing in technologies that support the use of eco-friendly packaging and improve recycling infrastructure.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the packaging sector is increasingly focused on specialized applications and material performance. The development of high barrier paper for food is critical for replacing multi-layer plastics, while the market for recyclable paperboard for beverages continues to expand as brands seek sustainable alternatives to plastic packaging.

- The e-commerce boom has solidified the role of corrugated boxes for e-commerce shipping, where lightweight paperboard for cost reduction is a key consideration. Innovations in molded fiber for electronics protection are displacing foams, and the adoption of oven-safe paperboard for frozen meals addresses consumer convenience. For sensitive applications, virgin fiber for pharmaceutical packaging ensures purity and compliance.

- Across the board, increasing recycled content in paperboard containers is a priority, alongside reducing packaging material waste through better design. The effectiveness of paper-based solutions for fresh produce is being proven by materials that offer better paperboard performance in refrigerated supply. This is further supported by the development of custom bio-based coatings for paperboard.

- For industrial needs, multi-wall paper sacks industrial use continues to be a robust segment. In retail, customized folding cartons for retail and fiber-based packaging for cosmetics leverage digital printing on corrugated packaging to enhance brand appeal.

- Central to all these efforts is the goal of improving paper packaging recyclability and demonstrating the overall cost-effectiveness of paperboard packaging, which can lower shipping weights by over 20% compared to rigid alternatives, directly impacting supply chain logistics. The integration of smart packaging for supply chain visibility adds another layer of value.

What are the key market drivers leading to the rise in the adoption of Paper And Paperboard Container And Packaging Industry?

- A pervasive shift toward sustainable and circular packaging solutions is a fundamental driver shaping the market.

- The demand for fiber-based packaging is heavily driven by the expansion of e-commerce packaging, which relies on corrugated board for both secondary packaging and tertiary packaging.

- The growing preference for renewable packaging materials has boosted the use of lightweight paperboards and containerboard, aligning with circular economy packaging goals. This shift has accelerated the adoption of paper-based solutions by 20% in key sectors.

- In the food industry, folding cartons, liquid packaging board, and innovative formats like oven-safe paperboard and paperboard trays are replacing plastics. The move toward shelf-ready packaging has also improved retail efficiency, reducing stocking times by over 25%.

What are the market trends shaping the Paper And Paperboard Container And Packaging Industry?

- The integration of smart technologies is transforming packaging from a simple container into a dynamic tool for communication and enhanced consumer engagement.

- Evolving market dynamics are shaped by the rise of intelligent packaging and smart packaging technologies, which transform containers into platforms for interactive packaging. Advancements in digital printing technology facilitate hyper-customization and on-demand production, allowing for a unique unboxing experience with items like specialty papers and graphic board.

- This trend enables the creation of innovative formats such as paper-based mailers, paper-based blisters, paperboard tubes, and composite cans. The adoption of micro-flute technology in these applications has improved structural integrity by 15%. Furthermore, these on-demand capabilities reduce production lead times by up to 40% compared to conventional methods, enhancing supply chain agility.

What challenges does the Paper And Paperboard Container And Packaging Industry face during its growth?

- Pervasive raw material price volatility and supply chain instability present a key challenge to industry growth.

- Navigating market challenges requires a focus on supply chain optimization and responsible sourcing of raw materials like virgin kraft pulp. Price volatility has compressed margins on products such as solid board and linerboard by up to 10% in recent quarters, complicating efforts toward environmental footprint reduction.

- While materials like coated unbleached kraft and coated recycled paperboard offer sustainability benefits, competition from flexible plastics, which can provide a 30% weight advantage, affects logistical efficiency. The technical complexities of paperboard converting for items like pressed paperboard, ensuring both material efficiency and packaging integrity, remain a hurdle for achieving widespread waste reduction.

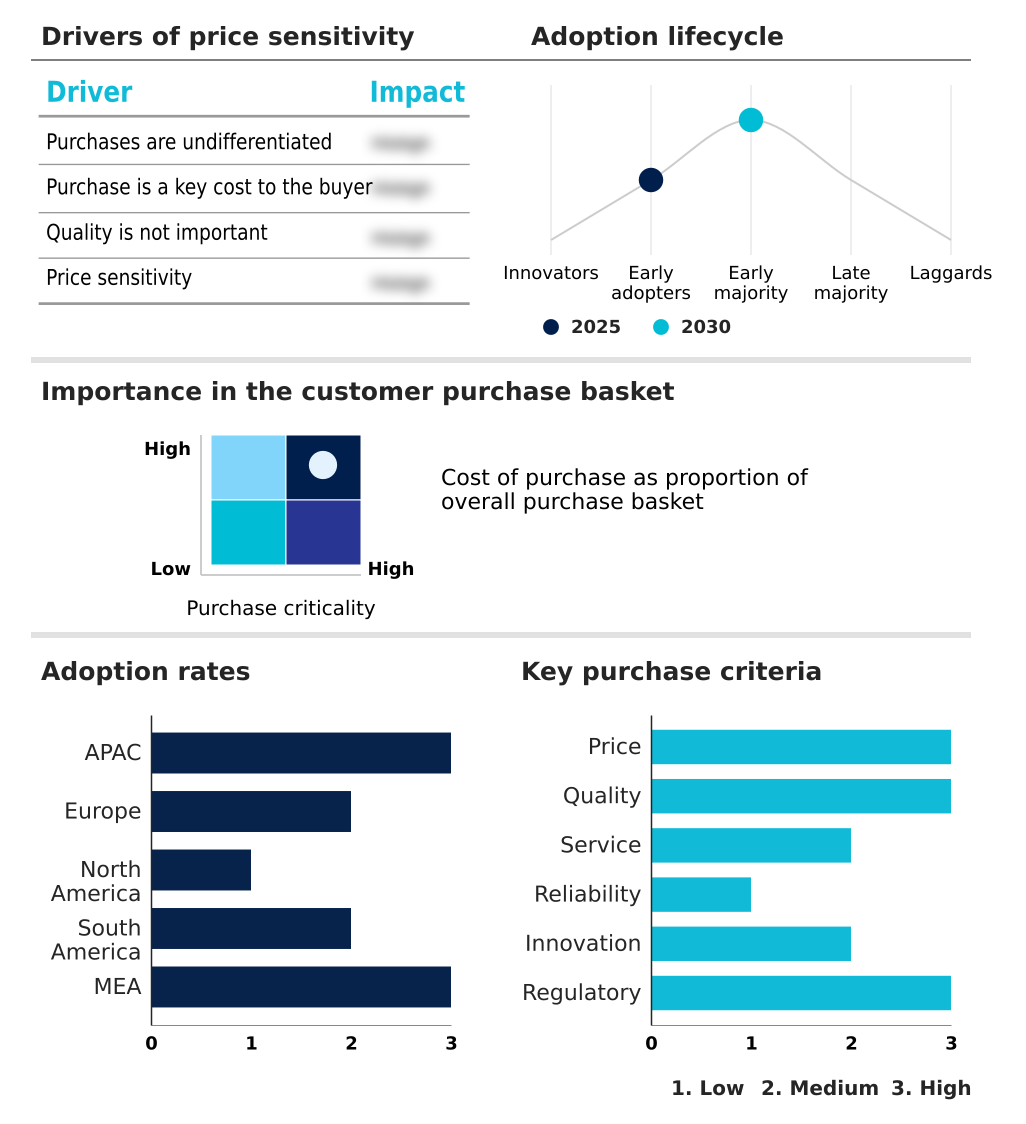

Exclusive Technavio Analysis on Customer Landscape

The paper and paperboard container and packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the paper and paperboard container and packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Paper And Paperboard Container And Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, paper and paperboard container and packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Analysis reveals specialized offerings in paper-based, fiber, and sustainable packaging, addressing a wide spectrum of industrial and consumer applications with innovative solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Cascades Inc.

- Clearwater Paper Corp.

- DS Smith Plc

- Genpak LLC

- Georgia Pacific LLC

- Graphic Packaging Holding Co.

- Hood Packaging Corp.

- International Paper Co.

- ITC Ltd.

- Lee and Man Paper Manufacturing

- Mondi Plc

- Nippon Paper Industries Co Ltd.

- Oji Holdings Corp.

- Rengo Co. Ltd.

- Smurfit Westrock plc

- Sonoco Products Co.

- Stora Enso Oyj

- UFP Technologies Inc.

- UPM Kymmene Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Paper and paperboard container and packaging market

- In March, 2025, Nestle announced a $2 billion strategic investment to accelerate its transition from virgin plastics, partnering with International Paper to develop recyclable, high-barrier paperboard wrappers.

- In February, 2025, The European Union enacted a new directive requiring paper-based packaging with a plastic polymer lining to be labeled as non-recyclable in standard paper waste streams, pushing for innovation in barrier technologies.

- In April, 2025, DS Smith entered a strategic partnership with HP to install a fleet of high-speed PageWide digital presses, enabling on-demand, customized corrugated packaging for e-commerce brands.

- In March, 2025, Amcor launched recyclable paper-based trays for fresh produce in Southeast Asia, expanding its sustainable packaging portfolio to support regional circular economy goals.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Paper And Paperboard Container And Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 327 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2026-2030 | USD 64866.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | China, India, Japan, South Korea, Australia, Thailand, Germany, Italy, France, Spain, UK, Sweden, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The paper and paperboard container and packaging market is defined by a strategic pivot towards functional, sustainable materials. The industry is moving beyond basic containers, with innovations in high-barrier paper and bio-based coatings enabling cellulose-based materials to compete in demanding applications.

- For boardroom consideration, the alignment with ESG mandates is driving significant capital into developing repulpable materials and advancing paperboard converting techniques. Companies are leveraging a diverse portfolio, including virgin fiber paperboard for food contact materials and recycled paperboard for secondary packaging like corrugated board and folding cartons.

- Specialized formats such as liquid packaging board, consumer board, paperboard trays, and oven-safe paperboard are gaining traction. Advanced lightweight paperboards are reducing logistical costs, while molded fiber technology offers plastic-free protective solutions. The production of kraft paper, containerboard, linerboard, solid board, and graphic board from sources like virgin kraft pulp and unbleached kraft is being optimized.

- Materials like coated unbleached kraft and coated recycled paperboard offer enhanced printability. Niche products including pressed paperboard, paper sacks, multi-wall paper sacks, paper-based mailers, paper-based blisters, paperboard tubes, and composite cans highlight the sector's versatility. These advanced materials have improved shelf-life by 15%, directly influencing product strategy and market positioning.

- This focus on material science, including micro-flute technology and specialty papers, is critical for future competitiveness.

What are the Key Data Covered in this Paper And Paperboard Container And Packaging Market Research and Growth Report?

-

What is the expected growth of the Paper And Paperboard Container And Packaging Market between 2026 and 2030?

-

USD 64.87 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Paper bags and sacks, Corrugated containers and packaging, Folding boxes and cases, and Others), End-user (Food and beverages, Industrial products, Healthcare, and Others), Material (Virgin paperboard, and Recycled paperboard), Packaging (Primary packaging, Secondary packaging, and Tertiary packaging) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Pervasive shift toward sustainable and circular packaging solutions, Pervasive raw material price volatility and supply chain instability

-

-

Who are the major players in the Paper And Paperboard Container And Packaging Market?

-

Amcor Plc, Cascades Inc., Clearwater Paper Corp., DS Smith Plc, Genpak LLC, Georgia Pacific LLC, Graphic Packaging Holding Co., Hood Packaging Corp., International Paper Co., ITC Ltd., Lee and Man Paper Manufacturing, Mondi Plc, Nippon Paper Industries Co Ltd., Oji Holdings Corp., Rengo Co. Ltd., Smurfit Westrock plc, Sonoco Products Co., Stora Enso Oyj, UFP Technologies Inc. and UPM Kymmene Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by a focus on material efficiency and supply chain optimization, with the adoption of sustainable packaging solutions accelerating. The push for eco-friendly packaging and waste reduction has led to innovations where right-sizing algorithms for e-commerce packaging have decreased material use by up to 25%.

- Concurrently, the implementation of digital printing technology has improved on-demand production capabilities, cutting lead times by 40% compared to traditional methods. This allows for greater hyper-customization and a more engaging unboxing experience.

- As brand owners prioritize environmental footprint reduction, the demand for fiber-based packaging that meets both performance and circular economy goals continues to intensify, reshaping operational strategies across the board.

We can help! Our analysts can customize this paper and paperboard container and packaging market research report to meet your requirements.

RIA -

RIA -