Sanitary Pumps Market Size 2026-2030

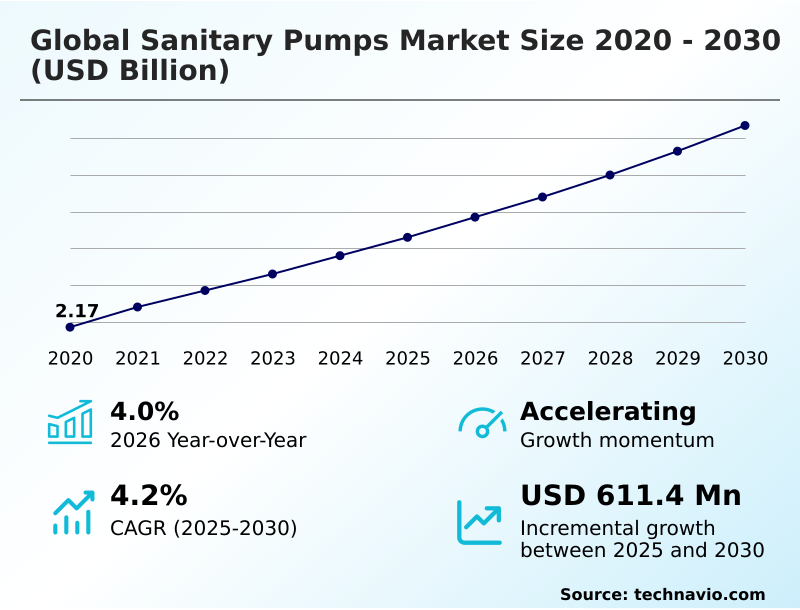

The Sanitary Pumps Market size was valued at USD 2.66 billion in 2025, growing at a CAGR of 4.2% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 57.1% growth during the forecast period.

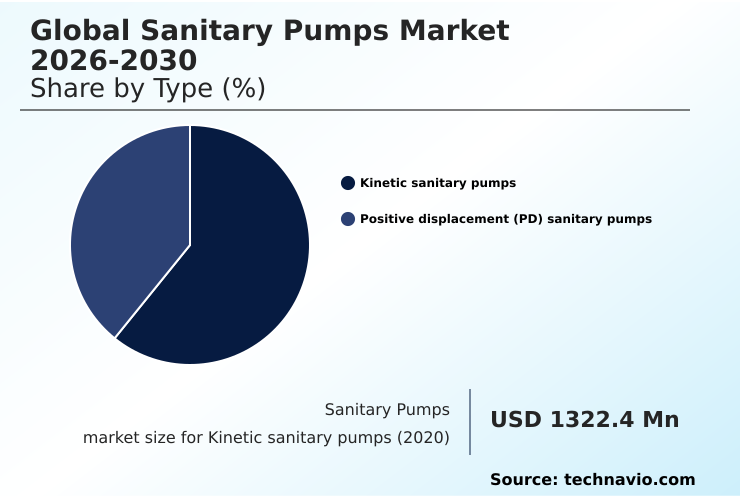

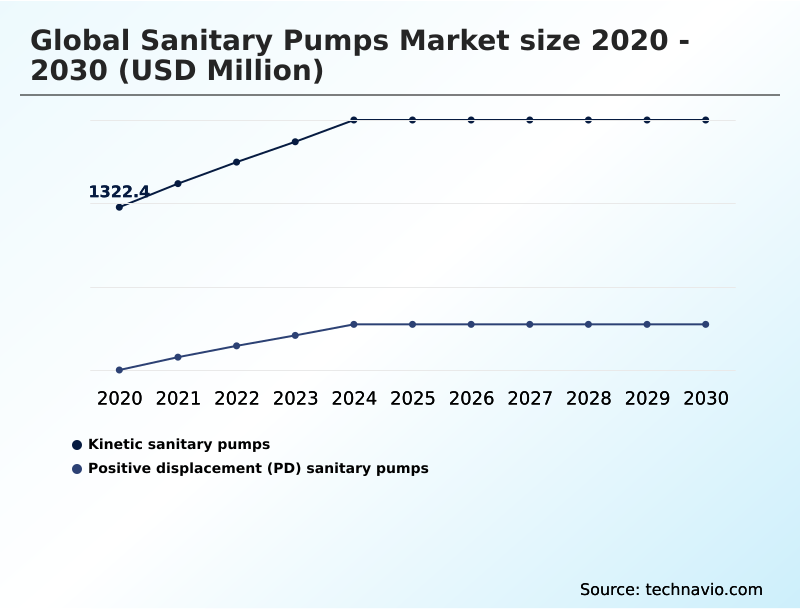

- By Type - Kinetic sanitary pumps segment was valued at USD 1.57 billion in 2024

- By End-user - Food and beverage segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 1.10 billion

- Market Future Opportunities 2025-2030: USD 611.4 million

- CAGR from 2025 to 2030 : 4.2%

Market Summary

- The sanitary pumps market is fundamentally shaped by regulatory pressures, with over 75% of procurement decisions in the biopharmaceutical sector prioritizing compliance certifications over initial equipment cost. This emphasis on risk mitigation drives continuous innovation in hygienic design and material science.

- A primary driver is the sustained expansion of end-use industries, where the demand for processed foods in emerging economies fuels capital investment in new production facilities. For example, a dairy processor needs pumps that support rapid, validated cleaning cycles to switch from milk to yogurt production, minimizing downtime, which can be improved by up to 30% with modern pump designs.

- Conversely, a major challenge is the high total cost of ownership, which includes not only the initial purchase but also energy consumption and maintenance. This high barrier particularly affects smaller enterprises, forcing them to balance upfront costs against long-term operational benefits and compliance risks.

What will be the Size of the Sanitary Pumps Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Sanitary Pumps Market Segmented?

The sanitary pumps industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Kinetic sanitary pumps

- Positive displacement (PD) sanitary pumps

- End-user

- Food and beverage

- Pharmaceutical and biotechnology applications

- Others

- Material

- Stainless steel

- Plastic

- Hastelloy

- Others

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- APAC

How is the Sanitary Pumps Market Segmented by Type?

The kinetic sanitary pumps segment is estimated to witness significant growth during the forecast period.

Kinetic sanitary pumps, which include centrifugal pumps, represent over 60% of installations in high-volume beverage processing and are favored for their operational efficiency in low-viscosity applications.

Their design simplicity translates to lower initial costs and reduced maintenance compared to positive displacement counterparts, making them ideal for bulk fluid transfer and clean-in-place (CIP) systems.

However, their performance diminishes with increasing fluid viscosity, and the high shear from the impeller design can damage delicate products.

Innovations in hydraulic efficiency and impeller design now allow certain models to reduce energy consumption by up to 15% compared to legacy equipment, addressing a key operational cost for processors while maintaining a hygienic design suitable for non-sensitive product streams.

The Kinetic sanitary pumps segment was valued at USD 1.57 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Sanitary Pumps market is rising in the leading region?

APAC is estimated to contribute 57.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Sanitary Pumps Market demand is rising in APAC Request Free Sample

The geographic landscape of the sanitary pumps market shows a distinct divergence between regions, with APAC accounting for 57.1% of the market's incremental growth, significantly outpacing North America's 17.5% contribution.

This disparity is driven by different market dynamics; APAC's growth is fueled by new facility construction in countries like China and India, where the food and beverage processing sector is rapidly expanding.

In contrast, growth in mature markets like North America and Europe is primarily driven by the need to upgrade existing infrastructure for improved operational efficiency and stricter regulatory compliance (FDA, EHEDG).

This leads to differing adoption patterns, with many buyers in APAC prioritizing initial cost, while European and North American customers focus more on total cost of ownership (TCO) and advanced features like smart pump integration, which can improve energy consumption reduction.

What are the key Drivers, Trends, and Challenges in the Sanitary Pumps Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Selecting the optimal fluid handling solution is a complex process, where a single pump type rarely meets more than 70% of all processing needs within a modern facility. For manufacturers, the decision hinges on balancing performance, cost, and compliance across diverse applications.

- A critical consideration is finding the right sanitary pump for high viscosity fluids, which typically requires positive displacement technologies like lobe or twin-screw pumps to ensure consistent flow without damaging the product. For the biopharmaceutical sector, identifying the best pumps for shear-sensitive biologics is paramount, often leading to the adoption of peristaltic or quaternary diaphragm designs that provide gentle handling.

- Furthermore, understanding the distinct cip vs sip pump requirements is essential for ensuring process sterility and material longevity under high temperatures. An equally important aspect is reducing energy costs with sanitary pumps, where implementing variable frequency drives can lower electricity usage by up to 30% in variable-flow applications.

- The strategic choice between a single-use pump vs stainless steel system presents another trade-off; disposable technologies can reduce initial capital outlay by 40% and eliminate cleaning validation, but introduce recurring consumable costs and new supply chain considerations. This highlights the need for a comprehensive evaluation of lifecycle costs and operational flexibility.

What are the key market drivers leading to the rise in the adoption of Sanitary Pumps Industry?

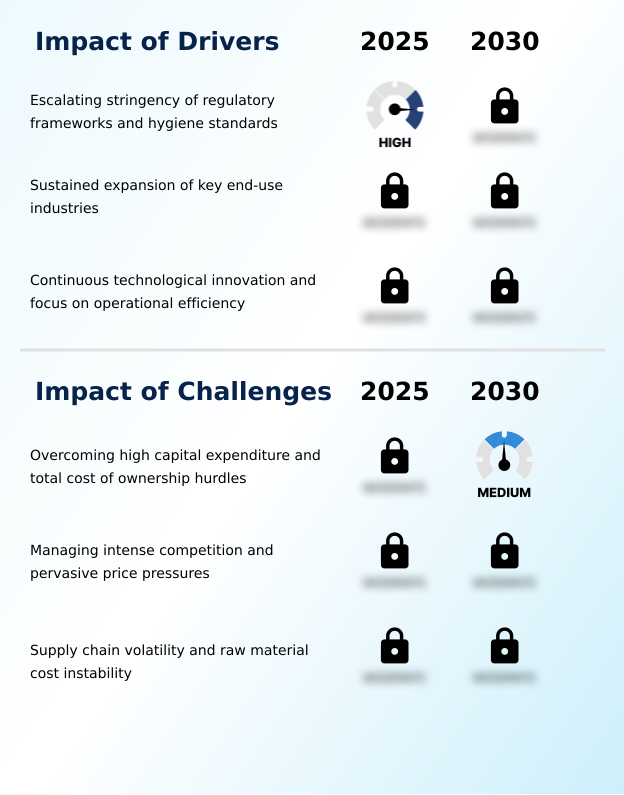

- The escalating stringency of regulatory frameworks and hygiene standards across key end-use industries serves as a primary driver for market growth.

- The primary market driver is the escalating stringency of regulatory frameworks, where a single non-compliance event can result in product recalls and a brand reputation drop of over 20% in consumer trust.

- This forces processors to invest in equipment featuring certified hygienic design and complete material traceability to mitigate risks. This need is compounded by the sustained growth of end-use industries.

- For example, the pharmaceutical and food and beverage processing sectors are expanding at a rate 1.5 times faster in emerging economies than in mature markets.

- This rapid industrialization creates consistent demand for compliant fluid handling solutions like aseptic filling systems to equip new and upgraded production facilities.

What are the market trends shaping the Sanitary Pumps Industry?

- A key market trend is the proliferation of intelligent pumping solutions. This includes the increasing digitalization of fluid handling systems to enhance process control and operational efficiency.

- A dominant trend is the integration of smart technologies, with IIoT-enabled pumps capable of reducing unplanned downtime by over 60% through predictive maintenance sensors. This digitalization facilitates enhanced process validation and is often a key component of process analytical technology (PAT) strategies, providing real-time data for improved consistency and quality control.

- Concurrently, the rapid adoption of single-use pump technology in bioprocessing is reshaping capital expenditure models. This shift is driven by the need to eliminate cross-contamination risk in aseptic fluid transfer and can reduce changeover times by more than 50% compared to traditional, reusable stainless steel systems, boosting manufacturing agility for contract manufacturers handling multiple high-value products.

What challenges does the Sanitary Pumps Industry face during its growth?

- A key challenge affecting industry growth involves overcoming the high capital expenditure and total cost of ownership associated with sanitary pump systems.

- A significant market challenge is the high capital expenditure, with a certified sanitary pump costing up to 3 times more than its industrial-grade counterpart, creating a substantial barrier for smaller enterprises. This upfront cost forces a difficult trade-off, as a focus on total cost of ownership (TCO) often justifies the higher initial investment through long-term operational efficiency.

- The challenge is amplified by persistent supply chain volatility. For instance, fluctuations in the price of raw material sourcing for 316L stainless steel have varied by as much as 40% in recent cycles, directly compressing manufacturer margins and extending equipment lead times for end-users.

Exclusive Technavio Analysis on Customer Landscape

The sanitary pumps market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the sanitary pumps market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Sanitary Pumps Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, sanitary pumps market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alfa Laval AB - Vendors provide a diverse portfolio of specialized fluid handling technologies, including kinetic and positive displacement pumps, engineered for stringent hygienic and aseptic processing applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alfa Laval AB

- Ampco Pumps Co.

- Axiflow Technologies Inc.

- Erich NETZSCH BV and Co.

- Fristam

- GEA Group AG

- Goulds Pumps

- IDEX Corp.

- INOXPA USA Inc.

- KSB SE and Co. KGaA

- LEWA GmbH

- NOV Inc.

- Pentair Plc

- PSG Dover

- Q Pumps

- Spirax Group

- SPX FLOW Inc.

- Sulzer Ltd.

- Verder Liquids

- Xylem Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Industrial Machinery and Supplies and Components industry, the integration of Industrial Internet of Things (IIoT) capabilities and digital twin technology has become a key differentiator, directly increasing demand for smart pump integration in the global sanitary pumps market 2026-2030 to enhance predictive maintenance and operational efficiency.

- A heightened focus on safety standards and risk mitigation in manufacturing setups has compelled end-users to prioritize equipment with certified hygienic design, boosting the adoption of sanitary pumps that ensure microbial contamination control and simplify process validation.

- The expansion of industrial output in key end-use sectors, particularly food and beverage processing and pharmaceutical manufacturing, creates sustained capital expenditure cycles, driving foundational demand for new and replacement sanitary pumps to equip additional production lines.

- A persistent drive to improve plant-wide operational efficiency and reduce energy consumption has accelerated the adoption of machinery with advanced HMI and variable frequency drives (VFDs), favoring sanitary pumps that deliver measurable energy savings and a lower total cost of ownership (TCO).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Sanitary Pumps Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.2% |

| Market growth 2026-2030 | USD 611.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The sanitary pumps market ecosystem is a tightly integrated network where end-user segments, particularly food and beverage processing, which accounts for over 60% of demand, dictate stringent product specifications. This value chain begins with suppliers of high-grade raw materials like 316L stainless steel and biocompatible polymers, which are crucial for manufacturers to meet regulatory compliance.

- These manufacturers, in turn, rely on distribution channels to provide local sales and technical support. Regulatory bodies such as 3-A and EHEDG play a pivotal role, as their certifications are often a prerequisite for market access.

- Certified hygienic design can reduce cleaning times by up to 25%, directly impacting the operational efficiency and total cost of ownership (TCO) for end-users in the pharmaceutical and dairy sectors. This interconnectedness ensures that innovation is driven by both compliance needs and the pursuit of operational excellence.

What are the Key Data Covered in this Sanitary Pumps Market Research and Growth Report?

-

What is the expected growth of the Sanitary Pumps Market between 2026 and 2030?

-

The Sanitary Pumps Market is expected to grow by USD 611.4 million during 2026-2030, registering a CAGR of 4.2%. Year-over-year growth in 2026 is estimated at 4.0%%. This acceleration is shaped by escalating stringency of regulatory frameworks and hygiene standards, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Kinetic sanitary pumps, and Positive displacement (PD) sanitary pumps), End-user (Food and beverage, Pharmaceutical and biotechnology applications, and Others), Material (Stainless steel, Plastic, Hastelloy, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa). Among these, the Kinetic sanitary pumps segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, Europe, North America, South America and Middle East and Africa. APAC is estimated to contribute 57.1% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Turkey and Egypt, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating stringency of regulatory frameworks and hygiene standards, which is accelerating investment and industry demand. The main challenge is overcoming high capital expenditure and total cost of ownership hurdles, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Sanitary Pumps Market?

-

Key vendors include Alfa Laval AB, Ampco Pumps Co., Axiflow Technologies Inc., Erich NETZSCH BV and Co., Fristam, GEA Group AG, Goulds Pumps, IDEX Corp., INOXPA USA Inc., KSB SE and Co. KGaA, LEWA GmbH, NOV Inc., Pentair Plc, PSG Dover, Q Pumps, Spirax Group, SPX FLOW Inc., Sulzer Ltd., Verder Liquids and Xylem Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape in the sanitary pumps market is intensely fragmented, with the top five players commanding less than 40% of the total market share, leading to significant price pressure. In response, established leaders like Alfa Laval and SPX FLOW are differentiating through technological innovation and strategic market expansion.

- For instance, the focus on smart pump integration is critical, as IIoT-enabled features can improve process uptime by over 20% by enabling predictive maintenance. This shift toward intelligent solutions directly addresses end-user demands for greater operational efficiency and simplified regulatory compliance.

- At the same time, the introduction of pre-assembled, modular systems by various players signifies a strategy to reduce installation complexity and cost for end-users, tackling the challenge of high capital expenditure.

We can help! Our analysts can customize this sanitary pumps market research report to meet your requirements.

RIA -

RIA -