Software Defined Everything (SDE) Market Size 2024-2028

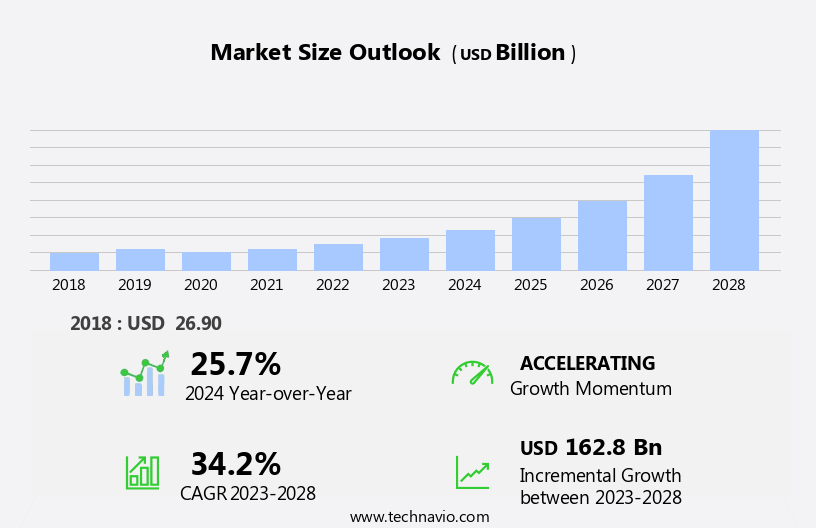

The software defined everything market size is forecast to increase by USD 162.8 billion at a CAGR of 34.2% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing adoption of cloud services among enterprises and the rising demand for cloud-based applications.The software businesses are increasingly turning to SDE solutions to enhance their infrastructure flexibility and agility, enabling them to respond more effectively to market demands and customer needs. However, the high cost associated with the installation of SaaS technology poses a significant challenge for market expansion.

- Despite this obstacle, opportunities exist for companies to capitalize on the market's momentum by offering cost-effective solutions and collaborating with cloud service providers to offer integrated offerings.By focusing on these opportunities and addressing the installation cost challenge, market players can effectively navigate the competitive landscape and capture a larger share of the growing SDE market.

What will be the Size of the Software Defined Everything (SDE) Market during the forecast period?

- The market continues to evolve, with security hardening and infrastructure automation at its core. Automation platforms enable seamless integration of self-service portals, machine learning, and configuration management, driving business agility and operational efficiency. Network programmability and virtualization platforms underpin network virtualization and software-defined networking, enabling network slicing and service mesh for telecom operators. Enterprise IT and data center modernization are major applications, with cost optimization and policy-based management key considerations. Cloud-native applications, open standards, and open source solutions further fuel innovation.

- The ongoing unfolding of market activities shapes the landscape, with digital transformation and cloud orchestration shaping the future. Financial services and various sectors adopt SDE for enhanced security and agility, as artificial intelligence and agile development continue to redefine business models.

How is this Software Defined Everything (SDE) Industry segmented?

The software defined everything (sde) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- IT and telecom

- BFSI

- Government and defense

- Others

- Application

- IT Infrastructure

- Cloud Computing

- Network Security

- Deployment Type

- Cloud

- On-Premises

- Component

- Software Defined Networking (SDN)

- Software Defined Storage (SDS)

- Software Defined Data Center (SDDC)

- Geography

- North America

- US

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Middle East and Africa

- UAE

- APAC

- Australia

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

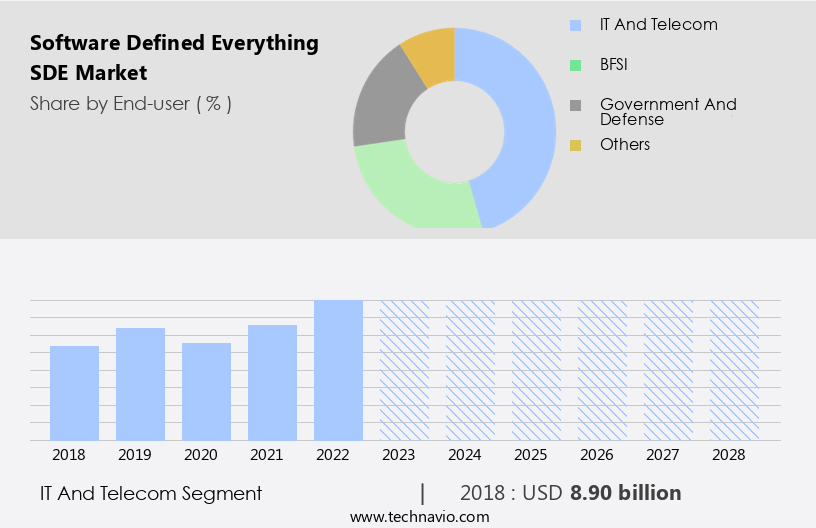

By End-user Insights

The it and telecom segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth as communication service providers (CSPs) seek to scale their operations across physical, virtual, and cloud resources without the need for hardware modifications. In the telecom sector, this shift is primarily driven by the increasing volume of data being generated, collected, and managed. Traditional storage solutions offer limited visibility, hinder integration, and restrict tool choices to proprietary options. As a result, the global SDE market is experiencing increased demand from telecom and IT enterprises in search of enhanced storage solutions. Telecom service providers are undergoing digital transformation to deliver advanced services, such as 5G Internet of Things (IoT), and edge computing solutions, to businesses and consumers.

Infrastructure automation, software-defined security (SDS), and orchestration tools are essential components of this transformation. SDS enables policy-based management and cost optimization, while network programmability and network virtualization facilitate network slicing and improved operational efficiency. Cloud orchestration and cloud-native applications are also driving the adoption of SDE, as they allow for self-service portals and agile development. Open standards and open source solutions are increasingly popular, as they offer flexibility and reduce company lock-in. Machine learning (ML) and artificial intelligence (AI) are playing a crucial role in network optimization and improving business agility. The financial services industry is another significant contributor to the SDE market, as they seek to enhance security and improve operational efficiency.

Service mesh and configuration management are essential tools for managing complex microservices architectures. Edge computing and virtualization platforms are also gaining traction, as they enable faster data processing and reduce latency. In conclusion, the SDE market is witnessing substantial growth due to the increasing demand for advanced services and the need for more efficient, flexible, and cost-effective solutions. The integration of automation platforms, SDS, orchestration tools, and open standards is transforming the telecom and IT industries, enabling businesses to adapt to the evolving digital landscape.

The IT and telecom segment was valued at USD 8.90 billion in 2018 and showed a gradual increase during the forecast period.

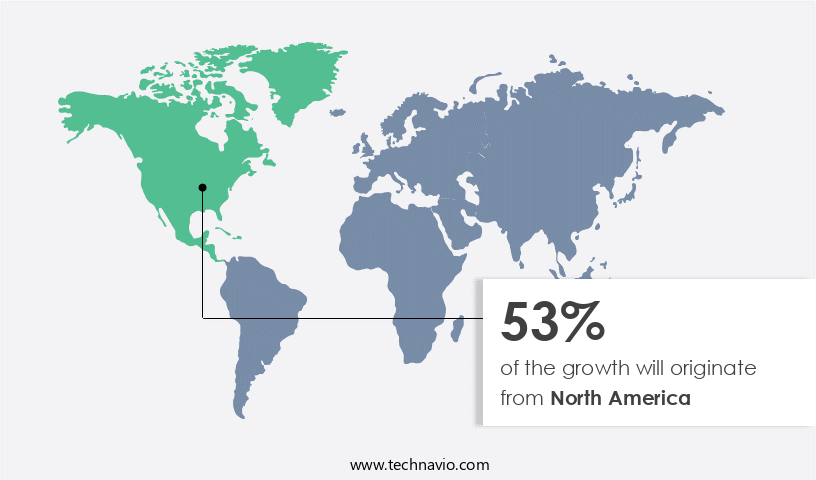

Regional Analysis

North America is estimated to contribute 53% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth, particularly in North America, which holds a prominent position in the global landscape. This region's dominance can be attributed to the increasing demand for cloud computing services, leading to the expansion of data centers and storage spaces. The Software-Defined Security (SDS) module is a key component of SDE, enabling users to scale resources on demand, making it an attractive solution for startups, SMEs, and enterprises alike. Its flexibility caters to temporary workloads and those subject to unexpected changes. The adoption of SDE is driven by the benefits of virtualization, automation of administrative tasks, and dynamic scaling.

Infrastructure automation and orchestration tools are essential components of SDE, ensuring operational efficiency and business agility. Open standards and open source solutions are integral to the SDE ecosystem, fostering innovation and collaboration. Machine learning and artificial intelligence are also playing a pivotal role in enhancing network programmability and network virtualization. Software-Defined Networking (SDN) and Software-Defined Storage (SDS) are critical technologies that enable policy-based management and cost optimization. Edge computing and service mesh further extend the reach of SDE, while digital transformation initiatives in telecom operators, financial services, and other industries are fueling the adoption of SDE for network slicing and cloud orchestration.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Global Software Defined Everything (SDE) Market is reshaping IT infrastructure through virtualization, automation, and intelligent control. Software-defined networking for IT companies enables agile, programmable networks that reduce complexity and cost. SD-WAN platforms for telecom operators offer scalable, high-performance connectivity for distributed networks. Software-defined storage for data centers improves flexibility and resource utilization across hybrid environments. The rise of AI-driven SDE for cloud infrastructure supports predictive automation and intelligent workload distribution. Security is reinforced with zero-trust security for SDE systems and blockchain integration for SDE security, ensuring robust data protection. Enterprises benefit from multi-cloud management for enterprises, optimizing performance and compliance across diverse cloud platforms. Edge SDE solutions for IoT bring real-time processing to connected devices, while real-time analytics for network management enhances visibility and operational efficiency. Additionally, containerized SDE for cybersecurity enables secure, scalable deployments critical to modern enterprise defense strategies

What are the key market drivers leading to the rise in the adoption of Software Defined Everything (SDE) Industry?

- The significant rise in the adoption of cloud services by enterprises serves as the primary market driver. The market is experiencing significant growth due to the increasing adoption of cloud-based managed services. SDE offers organizations centralized administration and control over all resources, including edge computing and virtualization platforms, through company-managed infrastructure and SLAs. Cloud computing eliminates the need for businesses to update and maintain IT infrastructure, allowing them to focus on their core competencies. Open standards and open source solutions are driving innovation in SDE, enabling cost optimization and policy-based management. Digital transformation is a key factor propelling the adoption of SDE, as it offers immersive and harmonious experiences for end-users.

- Configuration management and cost savings are additional benefits, making SDE an attractive option for organizations seeking to streamline their IT operations. Overall, the shift to cloud-based managed services is enabling businesses to reduce costs, improve efficiency, and enhance their digital capabilities.

What are the market trends shaping the Software Defined Everything (SDE) Industry?

- The increasing demand for cloud-based applications represents a significant market trend in the technology industry. Cloud solutions offer numerous benefits, including scalability, cost savings, and increased efficiency, making them an attractive option for businesses and individuals alike.

- The market is experiencing significant growth due to the increasing adoption of cloud computing by organizations worldwide. This shift is driven by the cost savings and flexibility offered by cloud services, enabling businesses to reduce capital expenditures (CAPEX) and focus on low-cost, agile development. Cloud orchestration, network slicing, artificial intelligence (AI), and service mesh are among the key technologies driving this trend. Cloud solutions offer quick implementation as they are accessible through web browsers, allowing for easy configuration and implementation within a short timeframe. Telecom operators and financial services are among the major industries embracing cloud-based technologies to enhance their operations and provide better customer experiences.

- AI is also playing a crucial role in driving innovation and automation in various industries. Moreover, the use of cloud-based solutions enables organizations to scale their workload as needed, eliminating the need for expensive data centers and reducing operating expenditure (OPEX). Agile development methodologies are also gaining popularity, allowing for faster time-to-market and increased efficiency. Overall, the adoption of cloud-based technologies is transforming the way businesses operate and providing them with a competitive edge.

What challenges does the Software Defined Everything (SDE) Industry face during its growth?

- The high cost of installing software-defined technology poses a significant challenge to the industry's growth trajectory. The market encompasses various technologies that enable enterprises to modernize their data centers, including infrastructure automation, security hardening, and orchestration tools. companies offer software-defined security (SDS) solutions, automation platforms, and storage solutions to help businesses streamline operations and reduce costs. However, the complexity of managing multiple software-defined storage solutions can pose a challenge for enterprises, leading to increased costs and potential inefficiencies. One of the primary drivers of the SDE market is the need for data center modernization. Technologies such as virtualization, containerization, and hyper-converged infrastructure enable enterprises to consolidate their data center components, reducing capital expenditures and operational expenses.

- companies provide software-defined storage solutions, including hyper-converged infrastructure, primary storage, secondary storage, object storage, and cloud storage, to address the diverse requirements of enterprises. Despite the benefits, there are challenges associated with software-defined storage solutions. Some companies require upfront licensing fees based on storage capacity requirements, while others may not fully utilize the existing storage infrastructure, leading to significant losses for enterprises. Effective management of these solutions is crucial to maximizing their value and ensuring a harmonious IT environment. In conclusion, the SDE market offers numerous opportunities for enterprises to optimize their data centers, but careful consideration of the challenges and benefits is essential for successful implementation.

- Recent research indicates that the trend towards software-defined everything is accelerating, making it an exciting and dynamic area for enterprise IT.

Exclusive Customer Landscape

The software defined everything (sde) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the software defined everything (sde) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, software defined everything (sde) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arista Networks - The company specializes in Software-Defined Everything (SDE) solutions, specifically SD-WAN technology, which optimizes network and security services for branch offices. Our brand, Versa Networks, delivers advanced functionalities, enhancing business agility and performance. By leveraging SDE architecture, organizations can simplify branch office operations, improve application performance, and bolster security. This technology enables dynamic, automated network and application policies, ensuring business continuity and reducing IT complexity. Versa Networks' SD-WAN solution seamlessly integrates various connectivity options, including broadband and MPLS, ensuring optimal network performance and reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arista Networks

- AT&T

- Cisco Systems

- Citrix Systems

- Dell Technologies

- Ericsson

- Hewlett Packard Enterprise

- Huawei Technologies

- IBM Corporation

- Intel Corporation

- Juniper Networks

- Microsoft Corporation

- Nokia Corporation

- Nutanix

- Oracle Corporation

- Red Hat

- VMware

- Wind River Systems

- Extreme Networks

- Fortinet

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Software Defined Everything (SDE) Market

- In February 2024, IBM announced the launch of its new Software-Defined Manageability (SDM) solution, aimed at simplifying the management of complex IT environments using artificial intelligence and automation. This offering is expected to significantly enhance the market by streamlining the process of managing software-defined networks, storage, and applications (IBM Press Release, 2024).

- In May 2025, Microsoft and Amazon Web Services (AWS) joined forces to expand their strategic collaboration, enabling seamless integration between Microsoft Azure and AWS Outposts. This partnership is anticipated to accelerate the adoption of Software-Defined Infrastructure (SDI) and Software-Defined Networking (SDN) solutions, as businesses increasingly adopt multi-cloud strategies (Microsoft News Center, 2025).

- In August 2024, VMware, a leading player in the SDE market, secured a strategic investment of USD1.1 billion from Silver Lake Partners. The funds will be used to accelerate the company's innovation and growth in the areas of multi-cloud, edge computing, and artificial intelligence (VMware Investor Relations, 2024).

Research Analyst Overview

The market is experiencing significant growth and innovation, integrating various technologies to enhance business continuity and network security in a multi-cloud environment. Solutions for load balancing, network function virtualization, capacity planning, network analytics, edge orchestration, and container orchestration are essential for managing complex infrastructures. Service chaining, cloud bursting, and service assurance ensure seamless application delivery and scalability. Automation scripting, programmable infrastructure, hybrid cloud, predictive maintenance, data analytics, intent-based networking, performance monitoring, microservices architecture, disaster recovery, compliance frameworks, zero-trust security, serverless computing, dynamic routing, firewall management, and API management are key components driving market trends.

Network optimization is a critical focus area, enabling businesses to improve efficiency and reduce costs. These technologies enable businesses to adapt to changing demands, ensuring network security, enhancing application performance, and optimizing resource utilization. By leveraging the power of SDE, organizations can achieve greater agility, flexibility, and efficiency in their IT operations.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Software Defined Everything (SDE) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

148 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 34.2% |

|

Market growth 2024-2028 |

USD 162.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

25.7 |

|

Key countries |

US, China, Germany, Japan, UK, Australia, India, France, Brazil, UAE, Rest of World (ROW), Saudi Arabia, France, South Korea, Mexico, Italy, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Software Defined Everything (SDE) Market Research and Growth Report?

- CAGR of the Software Defined Everything (SDE) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the software defined everything (sde) market growth of industry companies

We can help! Our analysts can customize this software defined everything (sde) market research report to meet your requirements.

RIA -

RIA -