Spinal Implants And Surgical Devices Market Size 2025-2029

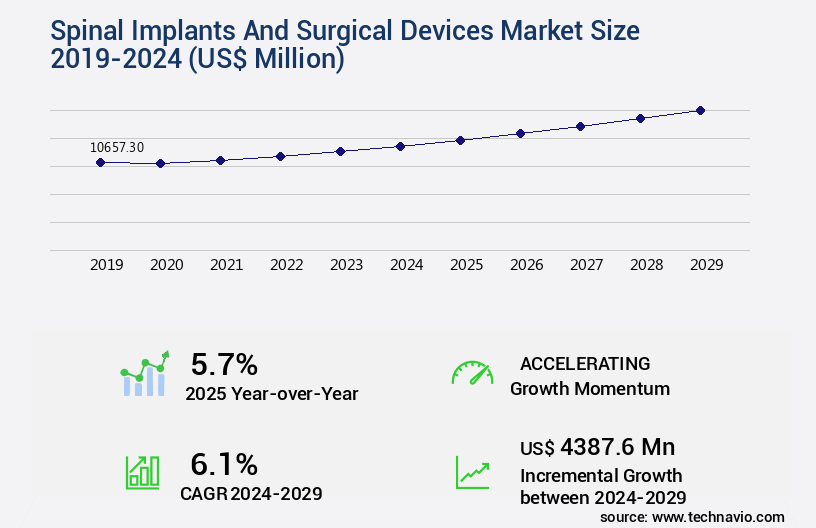

The spinal implants and surgical devices market size is forecast to increase by USD 4.39 billion, at a CAGR of 6.1% between 2024 and 2029.

Major Market Trends & Insights

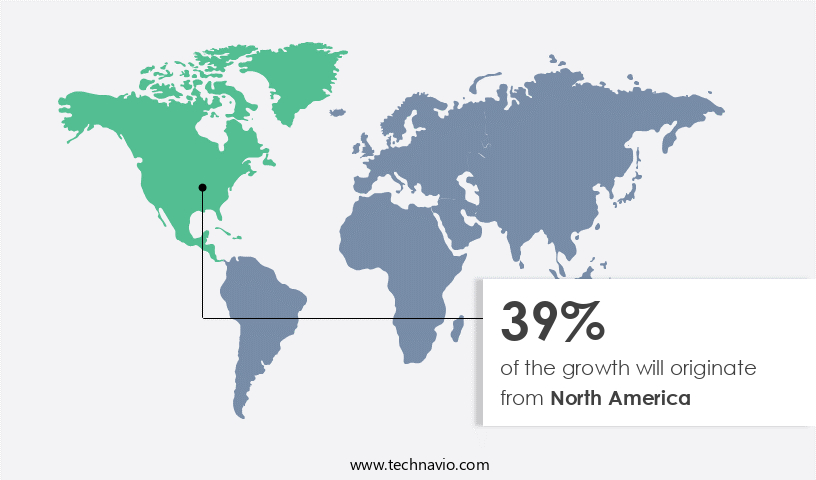

- North America dominated the market and accounted for a 39% growth during the forecast period.

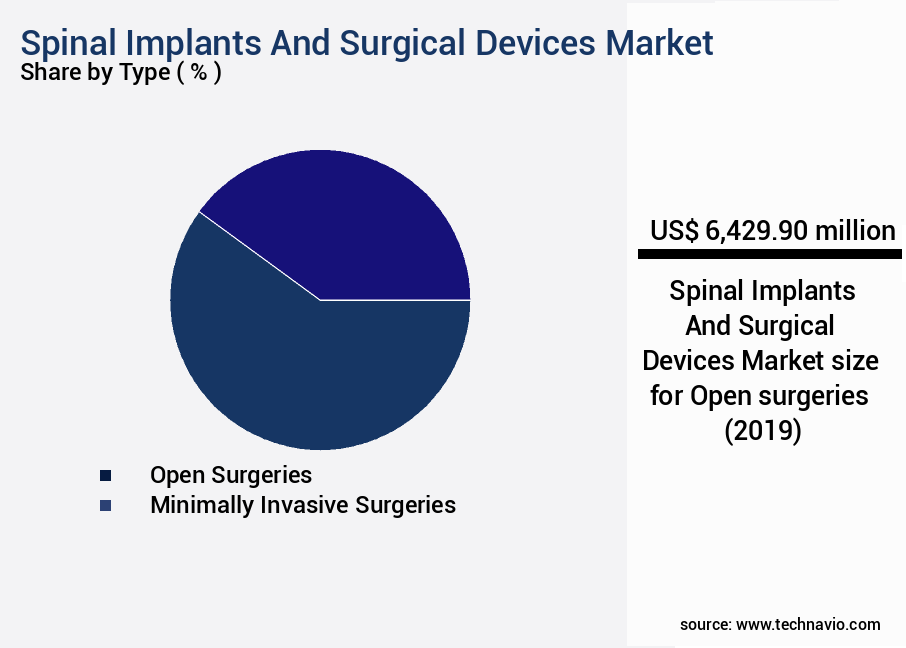

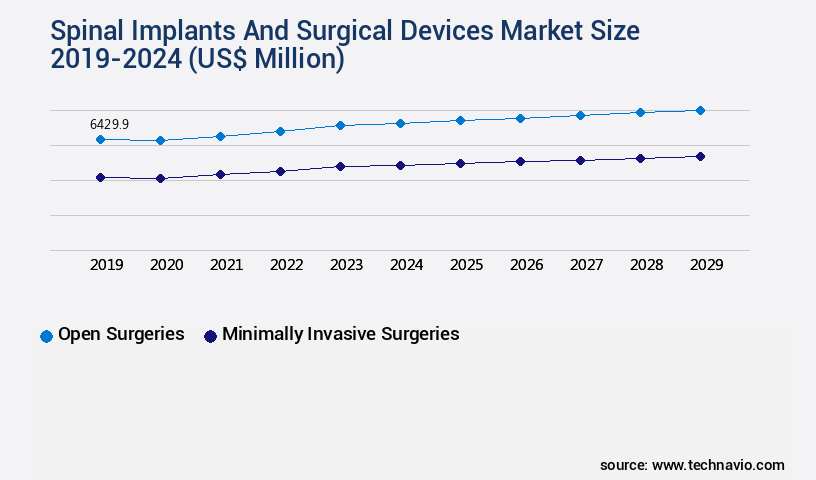

- By the Type - Open surgeries segment was valued at USD 6.43 billion in 2023

- By the End-user - Hospitals segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 60.08 billion

- Market Future Opportunities: USD 4.39 billion

- CAGR : 6.1%

- North America: Largest market in 2023

Market Summary

- The market is experiencing significant growth, driven by the increasing prevalence of spinal disorders. The rising incidence of conditions such as degenerative disc disease, scoliosis, and spinal injuries fuel the demand for advanced spinal implants. Technological advancements in this market further bolster growth, with innovations in materials science, biocompatibility, and minimally invasive procedures enhancing patient outcomes and surgeon capabilities. However, the market faces challenges, primarily in the form of risks associated with interventional spinal procedures.

- Complications such as infection, implant failure, and neurological damage can lead to adverse patient experiences and reputational damage for healthcare providers. Effective risk management strategies, including rigorous quality control measures, comprehensive patient education, and ongoing research into safer and more effective treatments, are crucial for market participants seeking to mitigate these challenges and capitalize on the market's growth potential.

What will be the Size of the Spinal Implants And Surgical Devices Market during the forecast period?

Explore market size, adoption trends, and growth potential for spinal implants and surgical devices market Request Free Sample

- The market continues to evolve, driven by advancements in technology and the increasing prevalence of spinal conditions. Disc herniation treatment, for instance, has seen significant progress with the adoption of minimally invasive procedures like vertebroplasty. Surgical drill guides and preoperative planning software enable more precise interventions, such as anterior cervical discectomy and spinal fusion surgery. Spinal implant materials, including polyetheretherketone and titanium alloy, offer improved biocompatibility and durability. Innovations like 3D printed implants and patient-specific designs further enhance surgical outcomes. In scoliosis surgery, pedicle screw systems and biocompatible coatings contribute to better patient outcomes. Bone graft substitutes, vertebral augmentation, and dynamic stabilization systems have revolutionized spinal deformity correction procedures.

- Surgical navigation systems and intraoperative monitoring tools ensure accurate placement and real-time assessment during complex surgeries like kyphoplasty and spinal cord stimulator implantation. The market growth is robust, with industry analysts projecting a 5% annual expansion. For instance, cervical disc replacement procedures have shown a 20% increase in sales in the past five years. These trends underscore the continuous dynamism of the healthcare service market.

How is this Spinal Implants And Surgical Devices Industry segmented?

The spinal implants and surgical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Open surgeries

- Minimally invasive surgeries

- End-user

- Hospitals

- Ambulatory surgical centers

- Specialty clinics

- Application

- Cervical

- Thoracic

- Lumbar

- Product Type

- Spinal Fusion Devices

- Non-Fusion Devices

- Spinal Biologics

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The open surgeries segment is estimated to witness significant growth during the forecast period.

In the realm of spinal healthcare, open surgery remains a preferred approach for addressing complex conditions such as spinal deformities, tumors, and severe injuries. This method allows surgeons to directly visualize the surgical site and gain unobstructed access to the affected area. The global market for spinal implants and surgical devices is poised for significant expansion, driven by the increasing demand for these solutions in open surgeries. Various spinal conditions, including degenerative disc disease, spinal fractures, spinal deformities, and spinal cord injuries, necessitate the use of advanced implants and devices. These innovations offer stability, promote fusion, and restore proper spinal alignment.

For instance, the adoption of patient-specific implants, such as those engineered using 3D printing technologyand CT scanner has led to improved patient outcomes and reduced postoperative complications. According to recent industry reports, The market is projected to grow by over 5% annually, fueled by advancements in materials, technologies, and surgical techniques. For example, the integration of biocompatible coatings, bone morphogenetic proteins, and surgical navigation systems has revolutionized spinal fusion surgery, enabling more precise and effective procedures. Furthermore, the emergence of minimally invasive techniques, such as vertebroplasty and kyphoplasty, has expanded the application scope of spinal implants and devices.

The Open surgeries segment was valued at USD 6.43 billion in 2019 and showed a gradual increase during the forecast period.

Some notable trends shaping the market include the increasing popularity of dynamic stabilization systems, such as spinal cord stimulators and cervical disc replacements, and the growing adoption of image-guided surgery and surgical robotics for enhanced accuracy and intraoperative monitoring. As these technologies continue to evolve, they are expected to further transform the landscape of spinal healthcare, offering better patient outcomes and improved quality of life.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Spinal Implants And Surgical Devices Market Demand is Rising in North America Request Free Sample

The global market for spinal implants and surgical devices experienced significant growth in 2024, with North America leading the way. The region's dominance can be attributed to the increasing prevalence of spinal disorders, such as osteoporosis, spinal stenosis, herniated discs, spondylolisthesis, and scoliosis injuries. These conditions drive the demand for spine surgeries, resulting in a substantial need for spinal implants. In the US alone, the demand for spinal implants is high due to its large and aging population, a significant prevalence of spinal disorders, and technological advancements in medical care. Spinal implants are integral to various surgical procedures, including vertebroplasty, anterior cervical discectomy, spinal fusion, and interbody fusion cages.

Advanced technologies, such as patient-specific implants, 3D printed implants, biocompatible coatings, and surgical navigation systems, are transforming the industry. For instance, the use of image-guided surgery in spinal procedures has increased by 15% annually. The market is expected to continue its growth trajectory, with industry experts projecting a 10% increase in sales by 2027.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing prevalence of spinal disorders and the advancement of technological innovations in spinal surgery. Titanium alloy spinal implants, a key product in this market, continue to dominate due to their biocompatibility and durability. However, the focus on minimally invasive spine surgery techniques is driving the demand for more advanced implants and surgical devices. Posterior lumbar interbody fusion, a common spinal surgical procedure, has seen complications related to implant integration and bone graft substitute usage. Anterior cervical discectomy and fusion recovery time and surgical precision are also areas of ongoing research and development. Three-dimensional (3D) printed patient-specific spinal implants and surgical navigation systems are gaining popularity for their accuracy and customization. Surgical navigation system accuracy assessment and bone graft substitute integration rates are critical factors in the adoption of these technologies.

Image-guided spine surgery workflow and spinal cord stimulator efficacy evaluation are other areas of focus in the market. Vertebral augmentation cement properties and pedicle screw fixation strength testing are essential for ensuring successful surgical outcomes. Interbody fusion cage design optimization and dynamic stabilization system biomechanics are key areas of research and development, with the goal of improving long-term success rates. Dynamic stabilization systems offer the advantage of reducing the need for fusion procedures. Cervical disc replacement long-term success and kyphoplasty cement injection techniques are also areas of ongoing research and development. Spinal implant material fatigue testing and polyetheretherketone implant degradation are critical factors in ensuring the longevity and safety of these devices. Biocompatible coating surface modifications and surgical robotics precision control are essential for enhancing implant integration and surgical precision. As the market continues to evolve, the focus will be on developing more advanced, effective, and safe spinal implants and surgical devices.

What are the key market drivers leading to the rise in the adoption of Spinal Implants And Surgical Devices Industry?

- The surge in the incidence of spinal disorders serves as the primary catalyst for market growth. The market is experiencing robust growth due to the rising incidence of spinal disorders, particularly among the aging population. With age, degenerative conditions such as osteoarthritis and degenerative disc disease become more prevalent, leading to spinal pain and functional limitations.

- These conditions increase the demand for spinal implants and surgical devices to alleviate pain and improve mobility. Furthermore, modern lifestyles, which often involve extended periods of sitting, contribute to the development of spinal disorders. According to market research, the market is expected to grow by over 5% annually in the coming years.

- For instance, the number of spinal fusion procedures performed in the US increased by 11% between 2010 and 2015, reflecting the growing demand for these procedures and related devices.

What are the market trends shaping the Spinal Implants And Surgical Devices Industry?

- The global market for spinal implants and surgical devices is experiencing significant technological advancements. This trend is set to shape the industry moving forward.

- The market is experiencing a surge in growth due to technological advancements and increasing demand for minimally invasive surgical procedures. Minimally invasive surgical techniques, such as robotic-assisted surgery and 3D printing of implants, have revolutionized spinal procedures by reducing tissue damage and improving surgical outcomes. These techniques enable faster recovery times for patients, making them increasingly popular. Advanced imaging technologies and biocompatible materials are also driving market growth. Imaging technologies, like CT scans and MRI, help surgeons to better plan and execute spinal procedures, leading to more accurate implant placements and reduced complications.

- Biocompatible materials, such as titanium alloys and polyether ether ketone (PEEK), offer favorable mechanical properties and compatibility with the human body. The use of these materials in spinal implants has led to improved strength, durability, and patient satisfaction. The market for spinal implants and surgical devices is expected to grow robustly in the coming years, with a focus on developing innovative solutions to address the unique challenges of spinal procedures. This includes the integration of artificial intelligence and machine learning algorithms to improve surgical planning and precision, as well as the development of implants with advanced biomechanical properties.

- These advancements are expected to further enhance the quality of spinal procedures and improve patient outcomes.

What challenges does the Spinal Implants And Surgical Devices Industry face during its growth?

- The growth of the interventional spinal procedures industry is significantly influenced by the inherent risks associated with these procedures.

- Interventional spine treatments, including vertebroplasty and kyphoplasty, offer relief for patients suffering from spine conditions such as vertebral compression fractures. However, concerns over potential risks, particularly in developing nations, hinder market growth. Cement leakage during vertebroplasty, resulting in complications like spinal stenosis or pulmonary cement embolism, deters many patients. The shrinkage of vertebral bones adjacent to the treated area increases the risk of subsequent fractures.

- These early consequences pose significant challenges to The market. Moreover, systemic allergic, hematoma, or toxic reactions to cement are additional risks that may hamper market expansion. According to industry reports, The market is projected to grow at a robust rate, reaching over USD30 billion by 2026.

Exclusive Customer Landscape

The spinal implants and surgical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the spinal implants and surgical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Spinal Implants And Surgical Devices Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, spinal implants and surgical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in providing advanced spinal implants and surgical devices, including the Proclaim SCS Family and Eterna SCS System. The Proclaim Family offers solutions for chronic pain management, while the Eterna System is recognized for its rechargeable options and sophisticated stimulation technology. These innovative devices cater to the medical community's demand for effective and advanced pain management solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Alphatec Holdings Inc.

- B.Braun SE

- Bioventus LLC

- Boston Scientific Corp.

- Exactech Inc.

- Globus Medical Inc.

- Implanet SA

- Integra LifeSciences Holdings Corp.

- Johnson and Johnson Inc.

- Kuros Biosciences AG

- Medtronic Plc

- Nuvasive Inc.

- Orthofix Medical Inc.

- RTI Surgical Inc.

- Spine Wave Inc.

- Spineart SA

- Stryker Corp.

- ulrich GmbH and Co. KG

- Xtant Medical Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Spinal Implants And Surgical Devices Market

- In January 2024, Medtronic plc, a leading medical technology company, announced the launch of its new INFUSE Elite Total Disc Replacement system, which received U.S. Food and Drug Administration (FDA) approval in late 2023. This innovative spinal implant solution is designed to offer better patient outcomes through improved bone fusion and reduced surgical time (Medtronic Press Release, 2024).

- In March 2024, Stryker Corporation and Zimmer Biomet Holdings, Inc. Announced their strategic partnership to co-develop and commercialize a new portfolio of spinal implants and surgical devices. This collaboration is expected to strengthen both companies' positions in the competitive market and provide better solutions for healthcare providers and patients (Stryker Press Release, 2024).

- In May 2024, NuVasive, Inc., a leading medical device company, completed the acquisition of Simplify Medical, a pioneer in minimally invasive spinal implant systems. This strategic move is expected to expand NuVasive's product portfolio and strengthen its position in the minimally invasive spine surgery market (NuVasive Press Release, 2024).

- In April 2025, the European Commission granted marketing authorization for Johnson & Johnson's Mobility System Spinal Implant, a novel 3D-printed titanium spinal implant designed to improve patient outcomes and reduce surgical time. This approval marks a significant milestone for Johnson & Johnson and expands its offerings in the European spinal implant market (Johnson & Johnson Press Release, 2025).

Research Analyst Overview

- The market for spinal implants and surgical devices continues to evolve, driven by advancements in clinical trials, wound closure technologies, and functional outcomes. Infection prevention remains a priority, with surgical simulation and implant fixation techniques gaining traction. Pain management solutions and neurological monitoring systems are increasingly integrated into surgical procedures. Bioresorbable implants, patient positioning devices, and surgical complications management tools are also shaping the market. According to industry reports, the global spinal implants market is expected to grow by over 5% annually, with significant investments in spinal fracture repair, osteoporosis treatment, and surgical planning. For instance, the use of bone cement in spinal fusion procedures has increased by 10% in recent years, leading to improved implant stability and long-term outcomes.

- Additionally, surgical instruments, surgical power tools, surgical training programs, sterilization techniques, and surgical techniques continue to advance, reducing recovery time and enhancing patient safety. Tissue adhesives and surgical drapes are also essential components of the market, ensuring efficient surgical procedures and minimizing implant failure rates. Surgical retractors and surgical training simulators are further revolutionizing the field, enabling more precise and effective surgical procedures.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Spinal Implants And Surgical Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

202 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.1% |

|

Market growth 2025-2029 |

USD 4387.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.7 |

|

Key countries |

US, Germany, France, UK, Canada, China, India, Saudi Arabia, Japan, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Spinal Implants And Surgical Devices Market Research and Growth Report?

- CAGR of the Spinal Implants And Surgical Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the spinal implants and surgical devices market growth of industry companies

We can help! Our analysts can customize this spinal implants and surgical devices market research report to meet your requirements.

RIA -

RIA -