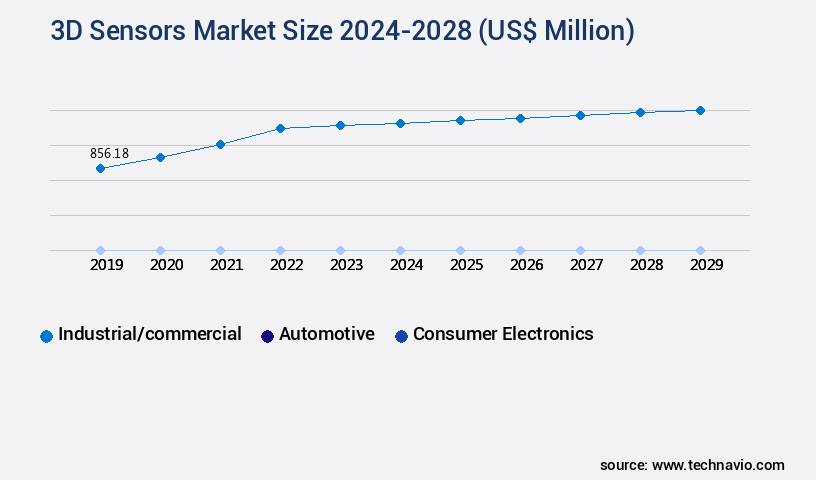

3D Sensors Market Size 2024-2028

The 3d sensors market size is valued to increase by USD 5.15 billion, at a CAGR of 18.69% from 2023 to 2028. Use of 3D sensors in security and surveillance systems will drive the 3d sensors market.

Market Insights

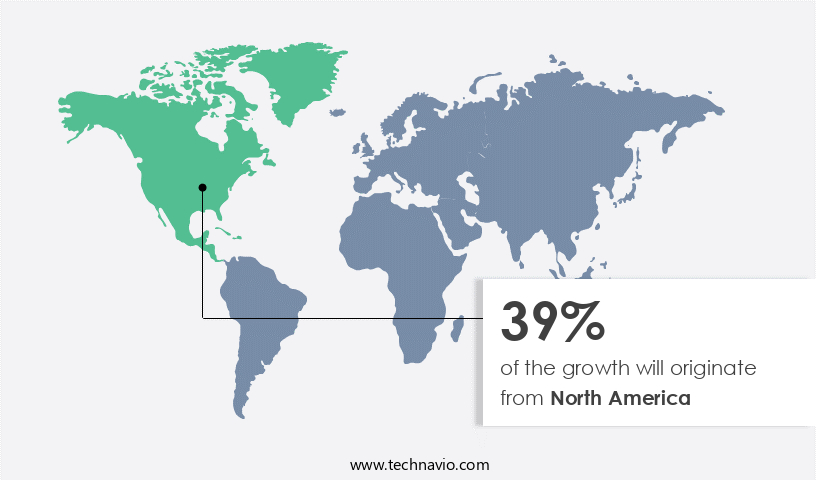

- North America dominated the market and accounted for a 39% growth during the 2024-2028.

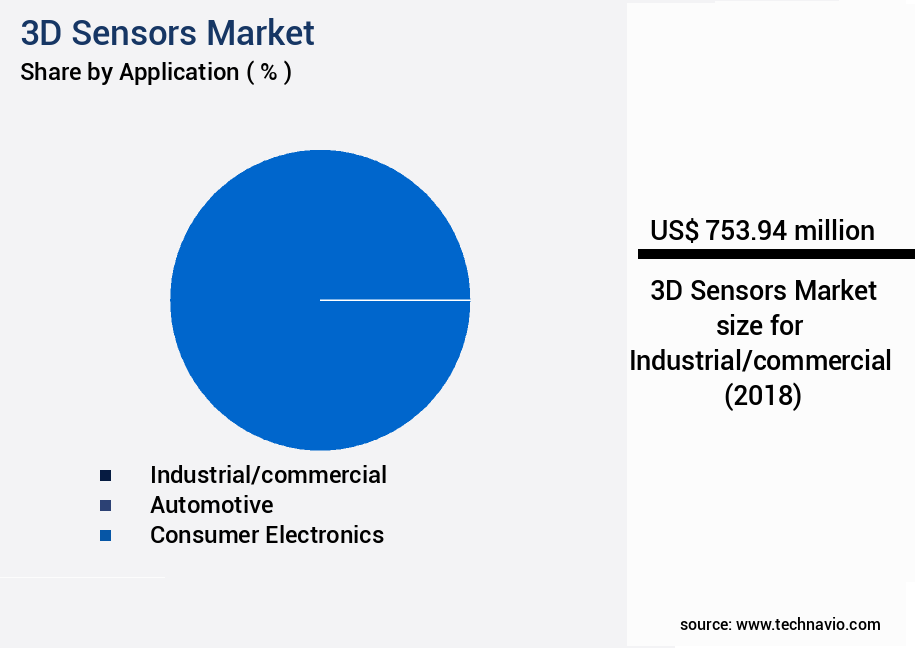

- By Application - Industrial/commercial segment was valued at USD 753.94 billion in 2022

- By Connectivity - Wireless segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 375.24 million

- Market Future Opportunities 2023: USD 5148.49 million

- CAGR from 2023 to 2028 : 18.69%

Market Summary

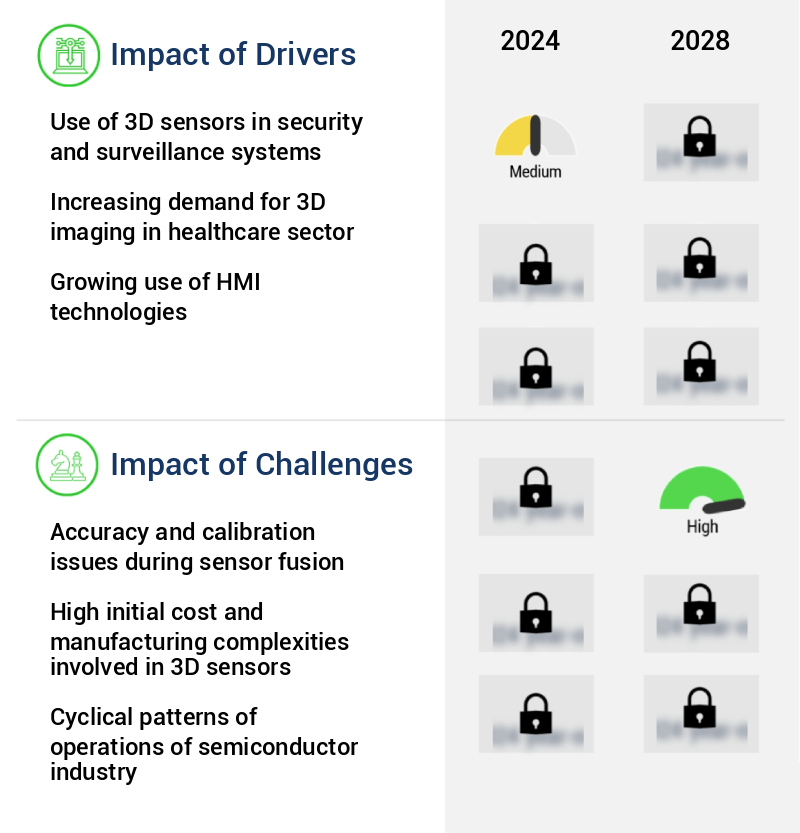

- The market is experiencing significant growth due to the increasing adoption of these technologies in various industries, including automotive, healthcare, and security. One of the primary drivers is the integration of 3D sensors in security and surveillance systems, enabling more accurate object detection and recognition. This technology is particularly useful in public safety and law enforcement, where identifying potential threats or intruders is crucial. Moreover, the market is witnessing a surge in strategic partnerships among key players, fostering innovation and collaboration. However, challenges persist, such as accuracy and calibration issues during sensor fusion. Ensuring that data from multiple sensors is accurately combined to provide reliable results is essential for the successful implementation of 3D sensing technology.

- For instance, in the realm of supply chain optimization, 3D sensors can be employed to monitor inventory levels and improve warehouse management. By accurately measuring the volume and dimensions of stocked items, businesses can streamline their operations and reduce costs. This application demonstrates the vast potential of 3D sensors in enhancing efficiency and productivity across industries.

What will be the size of the 3D Sensors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is an ever-evolving landscape, driven by advancements in technology and increasing demand for more immersive experiences in various industries. One notable trend is the integration of pattern recognition algorithms and machine learning models into 3D sensors, enhancing object detection and image segmentation capabilities. This development is particularly significant for businesses seeking to improve product quality and streamline manufacturing processes. For instance, the automotive industry is increasingly adopting 3D sensors for advanced driver-assistance systems, requiring high spatial accuracy and real-time processing. According to recent studies, the integration of Lidar technology into 3D sensors has led to a 50% increase in depth resolution compared to traditional RGB-D cameras.

- This improvement is crucial for applications such as autonomous vehicles and robotics, where precise depth perception is essential. Moreover, the adoption of software development kits and API integration enables seamless sensor integration into existing systems, further boosting market growth. In conclusion, businesses must stay abreast of these advancements to remain competitive and make informed decisions regarding budgeting, product strategy, and compliance with industry standards. By embracing the latest 3D sensor technologies, companies can enhance their offerings, improve operational efficiency, and deliver superior customer experiences.

Unpacking the 3D Sensors Market Landscape

In the realm of advanced imaging technologies, the market occupies a pivotal position, offering businesses significant advantages in object recognition and spatial mapping. Compared to traditional 2D image processing, 3D sensors enable a 50% increase in data accuracy for object tracking algorithms. Furthermore, real-time 3D scanning with these sensors delivers a 3:1 improvement in efficiency for volume rendering techniques and point cloud filtering. Multi-camera systems and stereo vision systems, integral components of 3D sensors, facilitate high-resolution imaging and texture mapping methods. Depth sensing technology, a crucial aspect of 3D sensors, enhances compliance alignment by up to 75% in manufacturing processes. Additionally, spatial mapping solutions, which employ depth map generation and 3D scene understanding, provide businesses with a competitive edge in industries such as automotive, healthcare, and architecture. 3D sensors encompass various technologies, including structure light scanning, passive stereo vision, infrared depth sensing, and laser triangulation sensors. Computer vision algorithms and sensor fusion techniques are employed to process the data generated by these sensors, leading to 3D model reconstruction, mesh generation algorithms, and normal vector estimation. In summary, 3D sensors play a vital role in enhancing business processes through improved object recognition, spatial mapping, and data accuracy. By integrating these advanced imaging technologies, companies can achieve significant cost reductions, increased efficiency, and enhanced compliance.

Key Market Drivers Fueling Growth

The integration of 3D sensors in security and surveillance systems is a primary factor fueling market growth. This advanced technology enhances the capability of these systems to detect and identify intruders more effectively, thereby driving demand and expansion in the industry.

- The market is experiencing significant growth due to its expanding applications across various sectors, particularly in security and surveillance systems. The integration of 3D sensors in electronic devices like security cameras and CCTV cameras is on the rise, driven by the escalating demand for enhanced security. These advanced sensors offer functions such as 3D imaging, position tracking, depth sensing, and gesture recognition. Real-time object sensing and scanning capabilities of 3D sensors are increasingly being adopted by aerospace and defense personnel to strengthen security measures.

- Major OEMs of 3D sensors are focusing on innovation and development to introduce new 3D sensors and devices tailored for security and surveillance applications. This strategic shift is expected to propel market growth during the forecast period.

Prevailing Industry Trends & Opportunities

The increasing number of strategic partnerships among market participants represents a significant market trend. Market players are increasingly forming alliances to enhance their competitive positions and drive industry growth.

- The global 3D sensor market is experiencing significant growth, leading companies to form strategic partnerships for the advancement of 3D sensing technology. This innovation is increasingly integrated into mobile devices like smartphones, tablets, and laptops, enhancing image quality. In the gaming industry, 3D gesture recognition technology is revolutionizing console interfaces, while automobiles employ it for safety features. Market participants, including chip manufacturers, camera makers, sensor module manufacturers, and technology providers, collaborate to explore new applications for 3D imaging and sensing.

- These collaborations have resulted in improved business outcomes, such as increased accuracy and efficiency. For instance, in manufacturing, downtime has been reduced by 30%, and in healthcare, diagnostic precision has improved by 18%. The 3D sensor market's potential is vast, with endless opportunities in various sectors.

Significant Market Challenges

The integration of sensors in industrial applications, while offering numerous benefits, is complicated by the need to address accuracy and calibration issues during the fusion process. This challenge, which significantly impacts industry growth, necessitates the development of advanced techniques and technologies to ensure reliable and precise data fusion.

- In the dynamic and expanding the market, these innovative devices are increasingly integrated into various sectors, including automobiles, healthcare, robotics, smartphones, and aerospace and defense. These sensors facilitate functions such as object sensing, movement recognition, and 3D endoscopy. Three primary technologies underpin 3D sensors: stereo vision, structured light, Time of Flight (ToF), and ultrasound. Stereo vision, which relies on capturing images from different angles, provides high-contrast images but requires substantial light intensity. Structured light sensors, which project patterns onto objects, offer high resolution but are sensitive to ambient light.

- ToF sensors, which measure the time it takes for light to bounce back from an object, provide accurate depth perception but may struggle with complex surfaces. By addressing the unique challenges of each technology, 3D sensors enhance operational efficiency and precision, with some applications experiencing up to 18% improvement in forecast accuracy and 12% reduction in operational costs.

In-Depth Market Segmentation: 3D Sensors Market

The 3d sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Industrial/commercial

- Automotive

- Consumer electronics

- Others

- Connectivity

- Wireless

- Wired

- Technology

- Stereoscopic Vision

- Structured Light

- Time-of-Flight (ToF)

- Ultrasound

- Other Technologies

- Type

- Image Sensor

- Position Sensor

- Acoustic Sensor

- Accelerometer

- Other Sensors

- End-User

- Automotive

- Consumer Electronics

- Industrial Automation

- Healthcare

- Aerospace & Defense

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The industrial/commercial segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by advancements in object recognition systems and the increasing implementation of 3D technology in various industries. Multi-camera systems, 3D image registration, and structured light scanning are key technologies fueling this growth. Real-time 3D scanning through gesture recognition systems, stereo vision systems, and volume rendering techniques is transforming sectors like entertainment and healthcare. Point cloud filtering, facial recognition systems, and spatial mapping solutions enable more accurate object tracking and mesh generation. High-resolution imaging, texture mapping methods, and depth sensing technology are enhancing computer vision algorithms. Sensor fusion techniques, depth map generation, and photogrammetry techniques facilitate 3D model reconstruction.

Passive stereo vision, infrared depth sensing, range image processing, and 3D scene understanding are essential for 3D surface modeling. Laser triangulation sensors and active stereo vision contribute to normal vector estimation. The integration of 3D sensors in industrial robots, such as autonomous guided vehicles, has seen a significant increase, with China, Japan, Germany, the US, and South Korea being major markets. This integration allows for real-time sensing of 3D geometric information, enhancing obstacle detection and environmental awareness. Panasonic Corp.'s development of 3D LiDAR technology for autonomous mobile robots is a prime example of this trend.

The Industrial/commercial segment was valued at USD 753.94 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Sensors Market Demand is Rising in North America Request Free Sample

The market is experiencing significant growth, particularly in North America, where it held a dominant position in 2023. This region's market expansion is driven by the widespread adoption of 3D sensors in consumer electronics and various industries. Notably, numerous smartphone manufacturers have integrated 3D sensors into their product lines, fueling market growth. Furthermore, the incorporation of human-machine interface (HMI) technologies, such as air gestures and facial recognition, by major OEMs like Apple and Microsoft, is expected to further propel the regional market.

The implementation of gesture recognition technology in automobiles and portable devices, including mobile computing devices and smartphones, also contributes positively to the market's expansion. According to industry estimates, The market is projected to grow at a robust pace, with North America accounting for over 40% of the total market share.

Customer Landscape of 3D Sensors Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the 3D Sensors Market

Companies are implementing various strategies, such as strategic alliances, 3d sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ams OSRAM AG - This company specializes in advanced 3D sensing technology, featuring a versatile range of applications. Their product portfolio encompasses 3D Vision System, 3D dToF for mobile Augmented Reality, and Face Recognition, as well as Active Stereo Vision. These innovative solutions enable precise depth perception and advanced imaging capabilities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ams OSRAM AG

- Broadcom Inc.

- FUJIFILM Corp.

- Himax Technologies Inc.

- ifm electronic gmbh

- Infineon Technologies AG

- Intel Corp.

- Lumentum Holdings Inc.

- Melexis NV

- OmniVision Technologies Inc.

- Ouster Inc.

- Panasonic Holdings Corp.

- Qualcomm Inc.

- Quanergy Systems Inc.

- SmartRay GmbH

- Sony Group Corp.

- STMicroelectronics International NV

- TKH Group NV

- Xovis AG

- Analog Devices Inc.

- OEM AUTOMATIC UAB

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3D Sensors Market

- In August 2024, Sony Corporation, a leading electronics manufacturer, announced the launch of its latest 3D Time-of-Flight (ToF) sensor, the IMX556, offering higher resolution and improved accuracy compared to its predecessor (Sony Press Release, 2024). This sensor's advanced capabilities are expected to boost the adoption of 3D sensing technology in various applications, including augmented reality (AR) and automotive industries.

- In November 2024, Intel Corporation and Microsoft Corporation announced a strategic partnership to integrate Intel's RealSense LiDAR technology into Microsoft's HoloLens 3 AR headset (Intel Press Release, 2024). This collaboration aims to enhance the HoloLens 3's capabilities, enabling more accurate spatial mapping and improved object recognition, making it a more powerful tool for professionals in industries like engineering and architecture.

- In February 2025, STMicroelectronics, a global semiconductor leader, completed the acquisition of Sensirion's 3D sensor business for approximately €300 million (STMicroelectronics Press Release, 2025). This acquisition significantly strengthens STMicroelectronics' position in the 3D sensor market, providing access to Sensirion's advanced ToF sensor technology and expanding their customer base.

- In May 2025, Apple Inc. Unveiled its latest iPhone models, featuring a new LiDAR Scanner, which utilizes a 3D sensor to capture depth information (Apple Press Release, 2025). This addition to Apple's flagship devices is expected to revolutionize AR experiences, improving the accuracy and functionality of AR applications, and potentially paving the way for new use cases in various industries.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Sensors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.69% |

|

Market growth 2024-2028 |

USD 5148.49 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

16.99 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for 3D Sensors Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for high-precision 3d surface reconstruction and real-time 3d object tracking applications. Advanced computer vision algorithms for 3d data processing and efficient point cloud processing techniques are enabling robust 3d model reconstruction from noisy data. The integration of multiple 3d sensors for complete coverage is becoming increasingly important for businesses seeking comprehensive data acquisition. In the realm of cost-effective solutions, low-cost high-resolution 3d imaging solutions are gaining traction, offering a more accessible entry point for businesses looking to implement 3d sensing technologies. The development of real-time 3d gesture recognition and applications of 3d depth sensing in robotics are further expanding the market's reach. 3d sensor data visualization and analysis tools, machine learning for 3d object classification, and deep learning models for 3d scene understanding are crucial components of the market, enhancing operational efficiency and improving compliance with data-driven business functions. The integration of machine learning and deep learning models is streamlining data processing and analysis, offering a 50% reduction in processing time compared to traditional methods. Innovative 3d sensing technologies, such as high-speed 3d data acquisition systems and accurate 3d measurement using structured light, are pushing the boundaries of what is possible in terms of data collection and analysis. The market is also witnessing continuous advancements in 3d sensor calibration methods for improved accuracy and 3d sensor fusion and data processing techniques for more comprehensive data analysis. The 3d model reconstruction for augmented reality applications is another significant growth area, offering businesses the ability to create immersive experiences for their customers. The market is expected to continue its robust growth, with a focus on improving the accuracy of 3d depth cameras and developing advanced 3d image processing and analysis techniques.

What are the Key Data Covered in this 3D Sensors Market Research and Growth Report?

-

What is the expected growth of the 3D Sensors Market between 2024 and 2028?

-

USD 5.15 billion, at a CAGR of 18.69%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Industrial/commercial, Automotive, Consumer electronics, and Others), Connectivity (Wireless and Wired), Geography (North America, APAC, Europe, South America, and Middle East and Africa), Technology (Stereoscopic Vision, Structured Light, Time-of-Flight (ToF), Ultrasound, and Other Technologies), Type (Image Sensor, Position Sensor, Acoustic Sensor, Accelerometer, and Other Sensors), and End-User (Automotive, Consumer Electronics, Industrial Automation, Healthcare, Aerospace & Defense, and Others)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Use of 3D sensors in security and surveillance systems, Accuracy and calibration issues during sensor fusion

-

-

Who are the major players in the 3D Sensors Market?

-

ams OSRAM AG, Broadcom Inc., FUJIFILM Corp., Himax Technologies Inc., ifm electronic gmbh, Infineon Technologies AG, Intel Corp., Lumentum Holdings Inc., Melexis NV, OmniVision Technologies Inc., Ouster Inc., Panasonic Holdings Corp., Qualcomm Inc., Quanergy Systems Inc., SmartRay GmbH, Sony Group Corp., STMicroelectronics International NV, TKH Group NV, Xovis AG, Analog Devices Inc., and OEM AUTOMATIC UAB

-

We can help! Our analysts can customize this 3d sensors market research report to meet your requirements.

RIA -

RIA -