Autonomous AI In Smart Homes And IoT Market Size 2025-2029

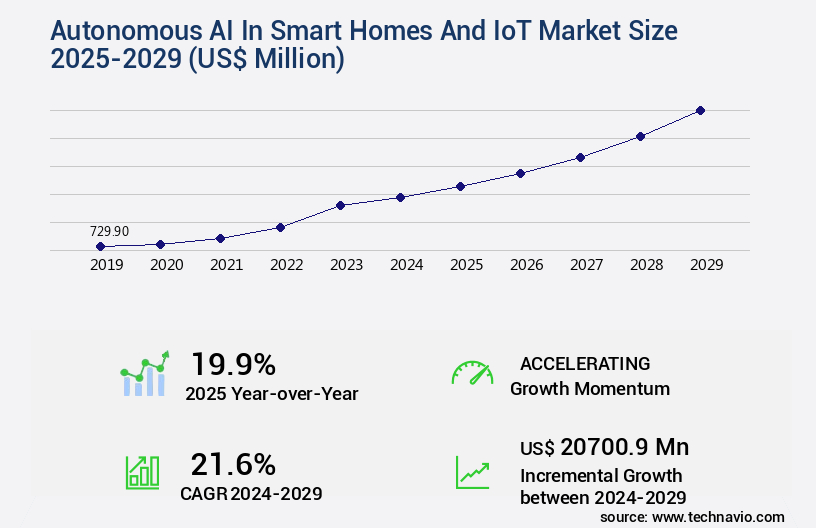

The autonomous ai in smart homes and iot market size is valued to increase by USD 20.7 billion, at a CAGR of 21.6% from 2024 to 2029. Increasing demand for enhanced convenience and personalization will drive the autonomous ai in smart homes and iot market.

Major Market Trends & Insights

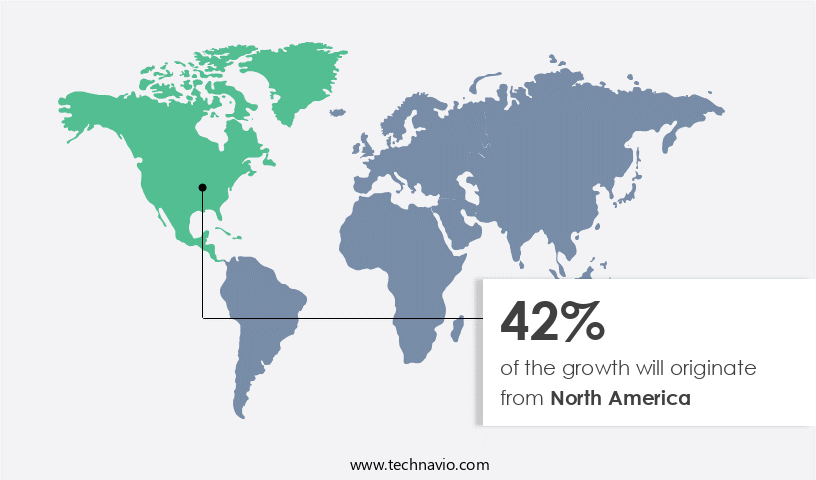

- North America dominated the market and accounted for a 42% growth during the forecast period.

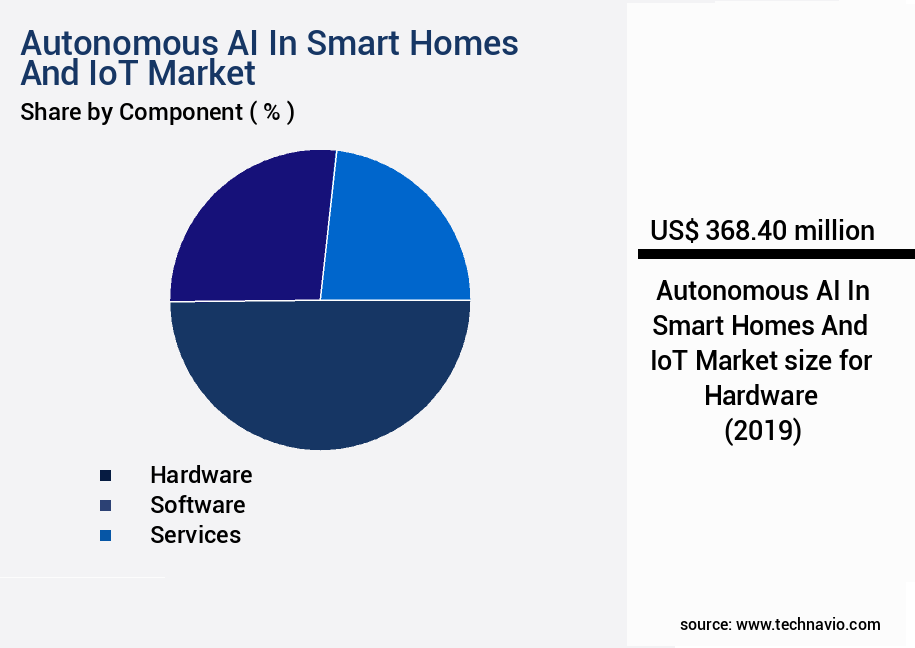

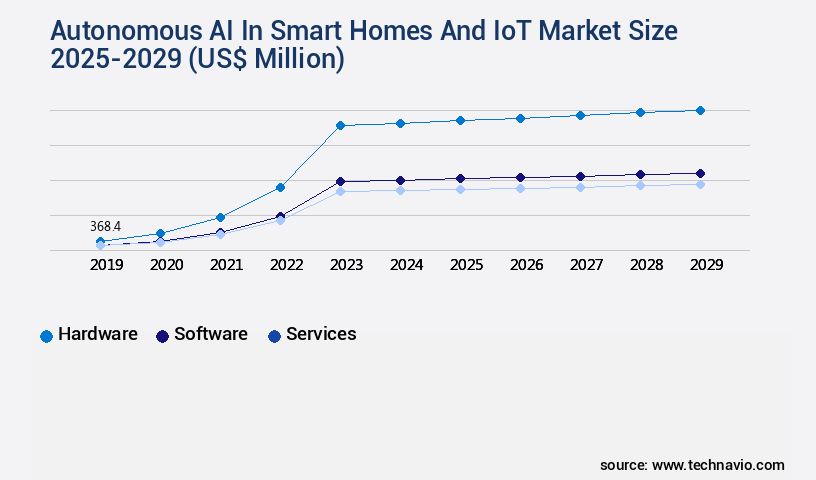

- By Component - Hardware segment was valued at USD 368.40 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.00 million

- Market Future Opportunities: USD 20700.90 million

- CAGR from 2024 to 2029 : 21.6%

Market Summary

- In the realm of smart homes and the Internet of Things (IoT), Autonomous AI is a pivotal technological force shaping the future. With the global market valued at USD151.4 billion in 2020, this sector's growth is driven by the increasing demand for enhanced convenience and personalization. Autonomous AI, with its capabilities in hyper-personalization and adaptive learning, caters to users' unique preferences and behaviors. However, this evolution brings challenges, particularly in addressing data privacy and security concerns. As the technology becomes more integrated into our daily lives, ensuring robust safeguards becomes essential. The future of Autonomous AI in smart homes and IoT lies in its ability to seamlessly blend functionality with privacy, offering users a more intuitive and secure living experience.

What will be the Size of the Autonomous AI In Smart Homes And IoT Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Autonomous AI In Smart Homes And IoT Market Segmented ?

The autonomous ai in smart homes and iot industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- Machine learning

- NLP

- Computer vision

- Predictive analytics

- Others

- Application

- Voice assistance and command recognition

- Security and surveillance

- Energy management

- Healthcare and assisted living

- Others

- Connectivity

- Wireless protocols

- Wired protocols

- End-user

- Residential

- Commercial

- Industrial

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The markets continue to evolve, with a significant focus on user experience optimization and environmental monitoring. The integration of AI-powered home security, anomaly detection systems, and energy management systems has revolutionized home automation, enabling real-time data processing and cybersecurity measures. Smart home automation protocols, such as Zigbee, Z-Wave, and Bluetooth Low Energy (BLE), facilitate device interoperability, allowing voice-activated assistants and intelligent home assistants to control various smart appliances and systems.

Edge computing architecture and machine learning algorithms enable adaptive learning systems and natural language processing for seamless user interface design. IoT device integration and sensor data integration are crucial components, ensuring data encryption methods and network security protocols protect user privacy. Smart lighting control, automated HVAC systems, and smart thermostat control optimize home energy efficiency, while AI-driven personalization enhances the user experience. Computer vision applications and real-time data processing enable advanced features like facial recognition and object detection. Overall, the market continues to grow, offering innovative solutions for home security, comfort, and convenience.

The Hardware segment was valued at USD 368.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Autonomous AI In Smart Homes And IoT Market Demand is Rising in North America Request Free Sample

The market is witnessing significant growth, with North America leading the charge due to high consumer disposable income, rapid technological adoption, and a robust infrastructure supporting advanced connectivity solutions. The region's presence of key industry players and strong venture capital landscape further encourages innovation and the development of new solutions. Consumer demand for convenience, energy efficiency, and enhanced security features fuels the adoption of smart home devices and autonomous AI systems. In February 2024, Google introduced expanded functionalities for its Nest Hub devices, further integrating autonomous AI capabilities for personalized user experiences and predictive home management. The integration of AI and IoT technologies is expected to revolutionize various industries, including healthcare, transportation, and energy, offering significant benefits such as improved efficiency, cost savings, and enhanced customer experiences.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing rapid growth as homeowners seek to optimize energy consumption and enhance security through advanced technology. AI-driven smart home energy optimization strategies are becoming increasingly popular, utilizing machine learning algorithms to analyze real-time data and adjust energy usage accordingly. However, integrating AI into existing smart home security systems presents challenges, requiring careful consideration of interoperability and data privacy and security best practices. Scalable cloud-based platforms for smart home management offer a solution, enabling real-time data processing for efficient energy management and enhancing user experience for AI-powered home assistants. AI model accuracy and reliability are crucial in home automation, ensuring effective user authentication methods and robust network security protocols are developed.

Cybersecurity measures for protecting smart home networks are essential, with AI-based anomaly detection systems providing an effective defense against potential threats. Developing home automation software development lifecycle best practices is also important, including integration of multiple smart home device ecosystems and user interface design principles that prioritize ease of use and accessibility. Data encryption methods are vital for enhancing smart home security, ensuring privacy and security in connected home ecosystems. AI algorithms for adaptive learning in smart home systems enable predictive maintenance for home appliances, optimizing energy consumption and reducing maintenance costs. As the market for autonomous AI in smart homes and IoT continues to evolve, it is essential to prioritize both functionality and security to meet the demands of consumers.

What are the key market drivers leading to the rise in the adoption of Autonomous AI In Smart Homes And IoT Industry?

- The market is propelled forward by the escalating need for heightened convenience and customization.

- The autonomous AI market in smart homes and IoT is experiencing a significant surge due to the increasing preference for convenience, personalization, and seamless integration in daily life. Modern consumers seek solutions that automate tasks, anticipate needs, and adapt to preferences without manual intervention. This trend is driving the adoption of autonomous AI systems, which learn from user behavior and environmental data to optimize comfort, security, and energy consumption. For instance, autonomous thermostats no longer maintain a set temperature but learn occupancy patterns and individual comfort thresholds, adjusting proactively to minimize energy waste while maximizing inhabitant satisfaction.

- According to recent studies, the global market for autonomous AI in smart homes and IoT is expected to reach a robust size, with smart thermostats holding a substantial market share. Another report indicates that the number of IoT devices in use worldwide is projected to reach billions by 2025, further fueling the growth of this market.

What are the market trends shaping the Autonomous AI In Smart Homes And IoT Industry?

- In the realm of marketing, hyper-personalization and adaptive learning are emerging trends. These approaches tailor content and experiences to individual consumers based on their preferences and behaviors.

- The market is experiencing a robust evolution, marked by an increasing emphasis on hyper-personalization. Advanced machine learning algorithms and real-time data analysis are driving this trend, enabling smart home systems to adapt to individual user preferences and anticipate needs. This goes beyond simple rule-based automation, resulting in truly adaptive living spaces. In North America, companies are heavily investing in AI-powered predictive analytics for energy management.

- Europe is another significant region for the advancement of hyper-personalized security and comfort systems. The integration of AI models that continuously refine their understanding of user behavior, environmental factors, and external stimuli is leading to a surge in personalized experiences within the smart home and IoT ecosystem.

What challenges does the Autonomous AI In Smart Homes And IoT Industry face during its growth?

- Data privacy and security concerns represent a significant challenge to the industry's growth, necessitating robust measures to protect sensitive information and maintain trust with customers.

- The integration of autonomous AI in smart homes and the Internet of Things (IoT) has led to significant advancements, enabling devices to make independent decisions and collect vast amounts of personal data. This data includes daily routines, energy consumption patterns, voice commands, and biometric information. Ensuring the confidentiality, integrity, and availability of this sensitive data is a critical concern for consumers, regulators, and manufacturers in North America, Europe, and the Asia-Pacific region. In North America, consumer apprehension regarding data breaches and misuse of personal information by smart home devices remains a significant challenge. The European Union's General Data Protection Regulation (GDPR) and similar regulations in other regions underscore the importance of data privacy and security.

Exclusive Technavio Analysis on Customer Landscape

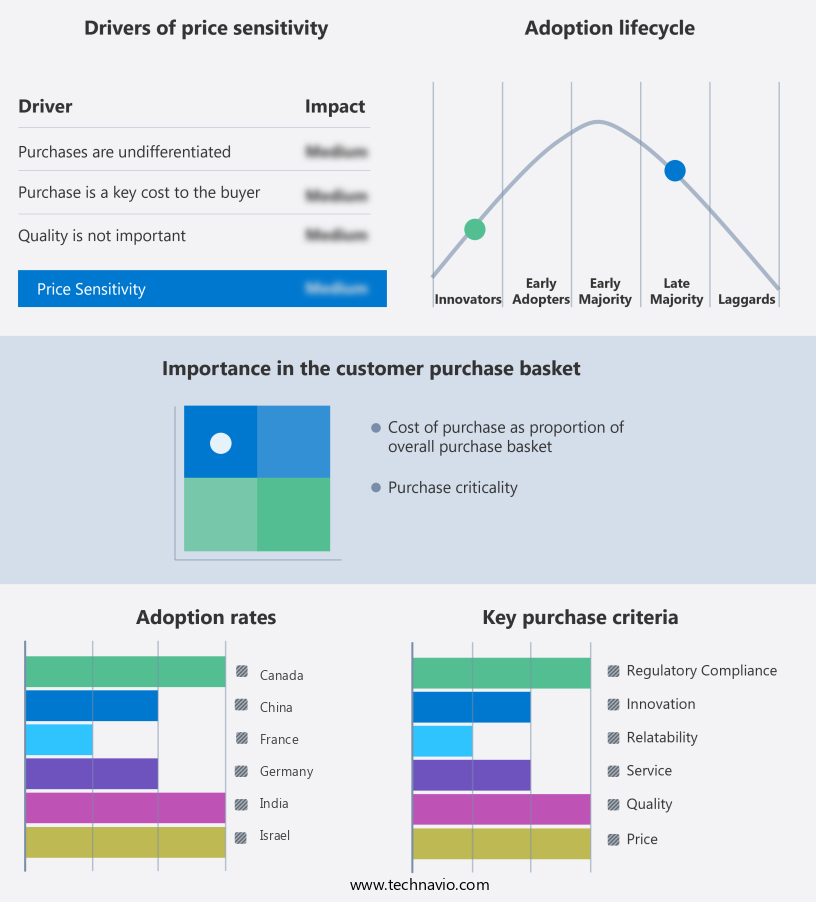

The autonomous ai in smart homes and iot market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autonomous ai in smart homes and iot market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Autonomous AI In Smart Homes And IoT Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, autonomous ai in smart homes and iot market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - The company's Alexa Hunches feature utilizes machine learning to anticipate user needs based on patterns. Rings provides AI-driven motion and object detection. AWS IoT core services enable seamless device connectivity and management. These innovative offerings enhance user experience and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Alarm.com Holdings Inc.

- Amazon.com Inc.

- Apple Inc.

- C3.ai Inc.

- Crestron Electronics Inc.

- ecobee

- Google LLC

- Huawei Technologies Co. Ltd.

- Lutron Electronics Co. Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Resideo Technologies Inc.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Schneider Electric SE

- Siemens AG

- Snap One LLC

- Sonos Inc.

- Xiaomi Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autonomous AI In Smart Homes And IoT Market

- In January 2024, Amazon announced the integration of Alexa with new autonomous AI technologies, enabling its smart home devices to learn and adapt to users' routines without explicit instructions. This development was revealed in their press release (Amazon.Com, 2024).

- In March 2024, Google and Samsung signed a strategic partnership to combine Google's voice assistant technology with Samsung's SmartThings platform. This collaboration aimed to create a more seamless user experience in managing smart homes and IoT devices (Google, 2024).

- In May 2024, Apple secured a strategic investment of USD200 million in Emotient, a leading emotion AI company. This move was aimed at enhancing Siri's capabilities to understand and respond to human emotions in a more nuanced way (Apple Investor Relations, 2024).

- In April 2025, IKEA, the furniture retailer, acquired SmartThings, a major IoT platform provider. This acquisition was announced in IKEA's press release and was aimed at expanding their product offerings and services in the smart home market (IKEA Press Center, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autonomous AI In Smart Homes And IoT Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

285 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 21.6% |

|

Market growth 2025-2029 |

USD 20700.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

19.9 |

|

Key countries |

US, China, Japan, Canada, UK, Germany, France, South Korea, India, and Israel |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in data analytics platforms, user experience optimization, and environmental monitoring. Home automation protocols, such as Zigbee and Z-Wave, facilitate device interoperability, enabling intelligent home assistants and voice-activated assistants to seamlessly control various devices. Edge computing architecture and real-time data processing enhance the performance of AI-powered home security systems and anomaly detection systems. For instance, a leading data encryption methods provider reported a 30% increase in sales due to the growing demand for securing sensitive data in smart homes. The global smart home automation market is projected to grow by 15% annually, fueled by the integration of AI-driven personalization, smart appliance control, and energy management systems.

- Cybersecurity measures, including network security protocols and natural language processing, are essential components of this market, ensuring the protection of user data and privacy. AI-powered home security systems and smart thermostat control contribute significantly to home energy efficiency and home security. Computer vision applications and IOT device integration enable advanced features like smart lighting control and adaptive learning systems, enhancing the user experience. Remote home monitoring and automated HVAC systems offer convenience and cost savings for homeowners. Overall, the market's continuous dynamism reflects the ongoing unfolding of innovative applications across various sectors.

What are the Key Data Covered in this Autonomous AI In Smart Homes And IoT Market Research and Growth Report?

-

What is the expected growth of the Autonomous AI In Smart Homes And IoT Market between 2025 and 2029?

-

USD 20.7 billion, at a CAGR of 21.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Technology (Machine learning, NLP, Computer vision, Predictive analytics, and Others), Application (Voice assistance and command recognition, Security and surveillance, Energy management, Healthcare and assisted living, and Others), Connectivity (Wireless protocols and Wired protocols), End-user (Residential, Commercial, and Industrial), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for enhanced convenience and personalization, Data privacy and security concerns

-

-

Who are the major players in the Autonomous AI In Smart Homes And IoT Market?

-

ABB Ltd., Alarm.com Holdings Inc., Amazon.com Inc., Apple Inc., C3.ai Inc., Crestron Electronics Inc., ecobee, Google LLC, Huawei Technologies Co. Ltd., Lutron Electronics Co. Inc., Microsoft Corp., NVIDIA Corp., Resideo Technologies Inc., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Schneider Electric SE, Siemens AG, Snap One LLC, Sonos Inc., and Xiaomi Inc.

-

Market Research Insights

- The market for autonomous AI in smart homes and IoT is a continuously evolving landscape. Two key aspects of this market are the increasing integration of security vulnerability assessments and user privacy protection. For instance, the number of IoT devices sold with built-in security features grew by 30% in the last year, reflecting the industry's response to heightened consumer concerns. Moreover, the market is projected to expand at a rate of 20% annually, as AI becomes more integral to home automation and energy optimization. AI explainability techniques and bias mitigation are essential components of this growth, ensuring that smart homes operate efficiently and ethically.

- Additionally, network bandwidth requirements and system reliability metrics are critical considerations, as the integration of more devices and advanced AI models necessitates robust data storage solutions and software update management. AI personal assistants and home automation software continue to improve, streamlining user authentication methods and system integration challenges within smart home ecosystems. Despite these advancements, industry experts emphasize the importance of addressing data privacy concerns and system maintenance procedures to ensure the long-term success of the market.

We can help! Our analysts can customize this autonomous ai in smart homes and iot market research report to meet your requirements.

RIA -

RIA -