Data Center GPU Market Size 2026-2030

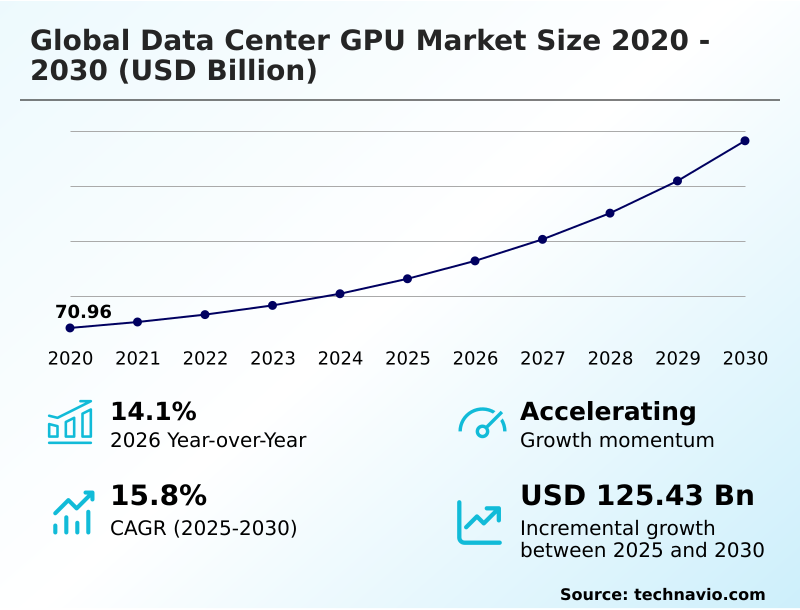

The data center gpu market size is valued to increase by USD 125.43 billion, at a CAGR of 15.8% from 2025 to 2030. Strategic expansion of AI training and trillion-parameter model development will drive the data center gpu market.

Major Market Trends & Insights

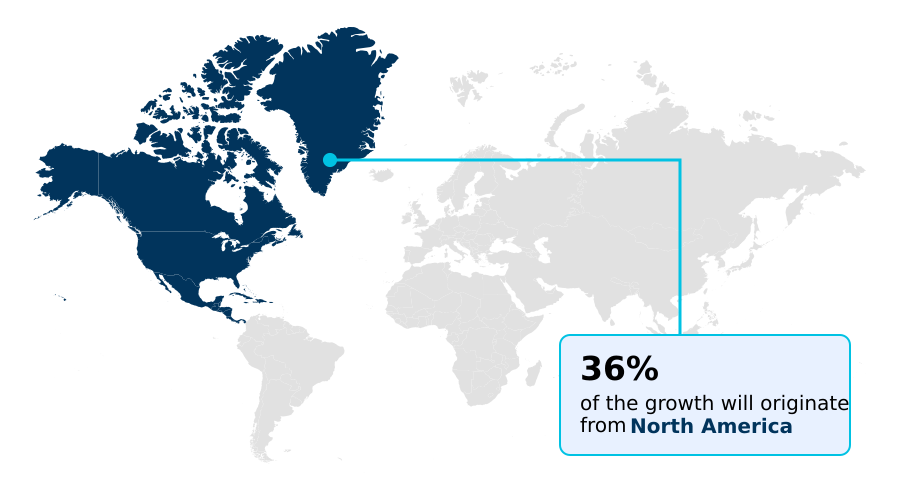

- North America dominated the market and accounted for a 36.3% growth during the forecast period.

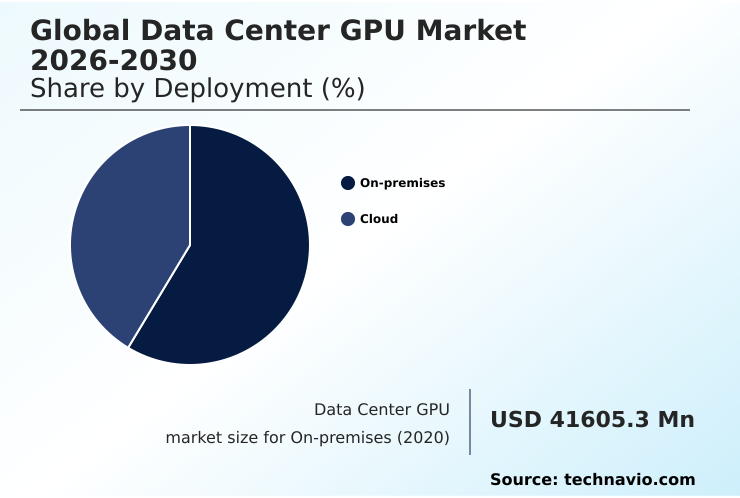

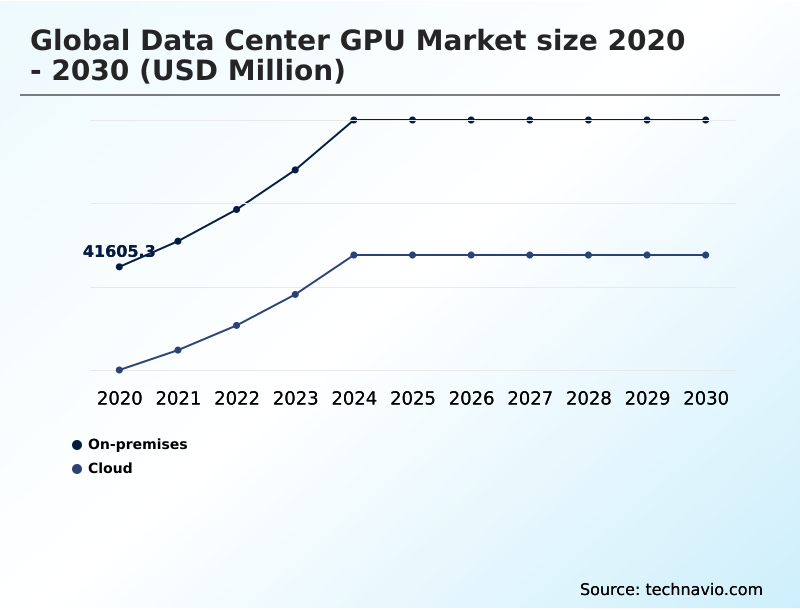

- By Deployment - On-premises segment was valued at USD 59.05 billion in 2024

- By Type - Training segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 170.14 billion

- Market Future Opportunities: USD 125.43 billion

- CAGR from 2025 to 2030 : 15.8%

Market Summary

- The data center GPU market is undergoing a structural transformation, shifting from general-purpose hardware to specialized accelerated computing. This evolution is driven by the computational demands of artificial intelligence, particularly large-scale model training and real-time inference. Modern GPUs leverage massively parallel architectures with thousands of cores to process complex algorithms far more efficiently than traditional CPUs.

- This capability is essential for industries adopting AI into their core operations. For instance, a pharmaceutical firm can utilize GPU clusters to simulate molecular interactions, drastically reducing drug discovery timelines. The technology's ecosystem is also maturing, with advancements in high-bandwidth memory, interconnect fabrics, and cooling technologies becoming critical for sustaining performance gains.

- As enterprises deploy more sophisticated AI applications, from predictive analytics to autonomous systems, the reliance on these powerful processors as the fundamental engine of digital innovation continues to intensify, shaping infrastructure investment strategies across the board.

What will be the Size of the Data Center GPU Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Data Center GPU Market Segmented?

The data center gpu industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud

- Type

- Training

- Inference

- Technology

- Generative AI

- ML

- NLP

- Computer vision

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

On-premises deployment remains a critical segment for organizations prioritizing data sovereignty and performance control.

This model involves direct ownership of hardware, enabling deep customization of the parallel processing architecture and tensor core technology to reduce inference latency for specific AI tasks.

For sectors like finance and defense, local control mitigates security risks inherent in multi-tenant environments. While requiring significant capital for procurement and maintenance, this approach provides predictable training performance without concerns for external network bottlenecks.

The adoption of advanced chiplet design and hardware-agnostic compilers is improving the total cost of ownership, with some firms reporting a 15% reduction in project runtimes by optimizing their bespoke infrastructure, including systems with a reconfigurable dataflow unit or tensor streaming processor, for specialized, compute-intensive workloads using floating-point 4 precision.

The On-premises segment was valued at USD 59.05 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Data Center GPU Market Demand is Rising in North America Get Free Sample

The geographic landscape of the data center GPU market is dominated by North America, which accounts for over 36% of the opportunity, driven by massive investments from US-based hyperscalers in AI factory infrastructure.

This region is the epicenter for custom silicon development and high-density computing.

Meanwhile, the APAC region is the fastest-growing, contributing more than 32% to the incremental growth, fueled by national AI strategies and the build-out of digital economies in countries like China, India, and Japan.

Organizations are deploying server-side parallel computing solutions, including those with a wafer-scale engine, to gain a competitive edge. The demand for AI accelerators with double-precision floating-point capabilities remains high globally, supporting both scientific research and commercial high-performance computing tasks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic investment in the Global Data Center GPU Market 2026-2030 requires a multifaceted evaluation beyond initial hardware acquisition. A thorough tco analysis of on-premise gpu clusters is essential, weighing capital expenditure against the long-term power consumption of high-performance gpus and operational costs.

- Key technical considerations include the interconnect bandwidth for distributed training, which directly impacts the scalability and efficiency of large model development. The debate over custom silicon vs commercial gpu performance is intensifying, as hyperscalers demonstrate the benefits of tailored hardware. For many, software compatibility for ai accelerators remains a primary concern, influencing the choice between open-source and proprietary ecosystems.

- The future of gpu chiplet technology promises greater customization and performance scaling. As deployments grow, understanding the thermal design power in server gpus and the benefits of liquid cooling for high-density racks becomes critical. Decision-makers must also assess the role of gpus in edge computing and the security risks in multi-tenant gpu clouds.

- Exploring pcie 6.0 impact on gpu performance and comparing fp8 and fp4 precision gpus helps future-proof investments. The hbm supply chain for ai accelerators continues to be a factor in procurement timelines, while achieving a positive ai accelerator roi for enterprise depends on aligning hardware capabilities with specific business goals.

- Efficient gpu virtualization for cloud environments and ensuring energy efficiency in gpu data centers are now standard operational requirements. Ultimately, success hinges on a holistic strategy that balances performance with sustainability and cost, a key determinant of the overall data center gpu market share.

What are the key market drivers leading to the rise in the adoption of Data Center GPU Industry?

- The strategic expansion of AI training capabilities and the development of computationally intensive trillion-parameter models are key drivers of market growth.

- The primary market driver is the exponential growth of generative AI workloads, which require an accelerated computing framework to function effectively. The development of trillion-parameter models necessitates massive GPU clusters capable of exascale performance for both training and inference.

- This demand for high-performance computing (HPC) has spurred significant investment in AI training infrastructure, with large language model (llm) processing needs increasing compute requirements by over 400% with each generation.

- The focus on neural network optimization is intense, as enterprises seek to balance model complexity with operational costs. This has led to the rise of specialized autonomous digital assistants and predictive analytics engines that provide real-time insights, driving further adoption.

What are the market trends shaping the Data Center GPU Industry?

- The market is witnessing a proliferation of liquid cooling architectures and high-density rack infrastructure. This shift addresses the increasing thermal demands of next-generation accelerators.

- Market trends are coalescing around thermal and architectural efficiency to support next-generation accelerators. The adoption of advanced liquid cooling solutions is becoming standard for new builds, with direct-to-chip cooling and immersion cooling systems enabling denser rack-scale solutions. This shift allows for a 15% improvement in power usage effectiveness (PUE) over traditional air-cooled designs.

- Architecturally, the move toward memory-centric architecture and advanced interconnect fabrics addresses performance bottlenecks, with next-generation interconnects doubling bandwidth for large-scale model training. Furthermore, AI sovereignty initiatives are driving regional investments in localized compute infrastructure, promoting data security and fostering specialized hardware development, supporting both AI training infrastructure and national strategic goals.

What challenges does the Data Center GPU Industry face during its growth?

- Supply chain volatility and a structural shortage of high-bandwidth memory present a key challenge, impacting production and availability across the industry.

- Significant market challenges stem from supply chain constraints and software complexities. The structural shortage of high-bandwidth memory (HBM) and advanced CoWoS packaging has created severe bottlenecks, extending lead times for top-tier GPUs by up to 50 weeks in some cases. This directly impacts supply chain resilience for hardware manufacturers.

- Concurrently, issues with thermal throttling prevention in densely packed racks elevate operational costs, as energy consumption for a single high-power rack can increase by 25%. Another hurdle is ensuring software ecosystem portability across different hardware platforms, which complicates workload optimization. Addressing the limitations of reticle-limited dies through innovative design is essential for future performance gains.

Exclusive Technavio Analysis on Customer Landscape

The data center gpu market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center gpu market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Data Center GPU Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, data center gpu market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - Offerings are centered on high-performance compute for AI training and HPC workloads, delivering data center GPUs designed for energy-efficient scalability and accelerated performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Alibaba Group Holding Ltd.

- Amazon Web Services Inc.

- Baidu Inc.

- Broadcom Inc.

- Cerebras Systems Inc.

- Etched

- Fujitsu Ltd.

- Google LLC

- Graphcore Ltd.

- Groq Inc.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Intel Corp.

- Microsoft Corp.

- NVIDIA Corp.

- Qualcomm Inc.

- Rivos Inc.

- SambaNova Systems Inc.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data center gpu market

- In March 2025, NVIDIA Corp. announced the first large-scale commercial deployments of its Blackwell GPU architecture in North American high-performance computing centers, enabling trillion-parameter AI model processing.

- In January 2025, Advanced Micro Devices Inc. revealed a strategic partnership with a major cloud provider to integrate its next-generation Instinct MI-series accelerators, expanding options for enterprise AI training workloads.

- In November 2024, Intel Corp. launched its next-generation AI accelerator, emphasizing an open-standard software approach to challenge proprietary ecosystems and improve code portability for developers.

- In September 2024, Google LLC began rolling out its latest generation of Tensor Processing Units (TPUs) across its cloud platform, offering a highly optimized alternative for large-scale inference and training.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Center GPU Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.8% |

| Market growth 2026-2030 | USD 125433.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.1% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Singapore, Australia, Germany, UK, France, Italy, The Netherlands, Spain, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center GPU market's trajectory is defined by a relentless pursuit of computational density, driven by generative AI workloads. This has forced a strategic pivot to an accelerated computing framework, where rack-scale solutions and GPU clusters are fundamental. The industry is moving beyond monolithic chips toward chiplet design and advanced reticle-limited dies to achieve exascale performance.

- Managing this power requires innovation in liquid cooling solutions, including direct-to-chip cooling and immersion cooling systems, for thermal throttling prevention and improved power usage effectiveness (PUE). Core to these systems are parallel processing architecture and tensor core technology, optimized for neural network optimization and both training performance and low inference latency.

- High-bandwidth memory (HBM) and advanced interconnect fabrics are critical enablers, though CoWoS packaging remains a bottleneck. Boardroom decisions now weigh the benefits of custom silicon development against reliance on established vendors, with hardware-agnostic compilers and open platforms like those using a reconfigurable dataflow unit or a tensor streaming processor gaining traction.

- For enterprises, deploying high-performance computing (HPC) infrastructure with processors supporting double-precision floating-point and floating-point 4 precision has reduced complex simulation times by over 25%, influencing budgeting for future AI factory infrastructure and AI sovereignty initiatives. This landscape demands a holistic approach, integrating everything from server-side parallel computing to memory-centric architecture and even unconventional designs like a wafer-scale engine.

What are the Key Data Covered in this Data Center GPU Market Research and Growth Report?

-

What is the expected growth of the Data Center GPU Market between 2026 and 2030?

-

USD 125.43 billion, at a CAGR of 15.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud), Type (Training, and Inference), Technology (Generative AI, ML, NLP, and Computer vision) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Strategic expansion of AI training and trillion-parameter model development, Supply chain volatility and structural shortage of high-bandwidth memory

-

-

Who are the major players in the Data Center GPU Market?

-

Advanced Micro Devices Inc., Alibaba Group Holding Ltd., Amazon Web Services Inc., Baidu Inc., Broadcom Inc., Cerebras Systems Inc., Etched, Fujitsu Ltd., Google LLC, Graphcore Ltd., Groq Inc., Huawei Technologies Co. Ltd., IBM Corp., Intel Corp., Microsoft Corp., NVIDIA Corp., Qualcomm Inc., Rivos Inc., SambaNova Systems Inc. and Tenstorrent Inc.

-

Market Research Insights

- The market's dynamics are shaped by the dual demands for raw computational throughput and operational efficiency. The integration of platform-level solutions has demonstrably improved workload optimization, with some enterprises achieving a 20% greater utilization of virtualized GPU resources. Concurrently, the push for real-time inference at the edge is driving architectural innovation.

- Strategic adoption of a cohesive silicon-to-software stack enables organizations to streamline MLOps pipelines, reducing model deployment times by up to 30%. This focus on hybrid cloud integration and energy-efficient scalability is critical as businesses balance performance needs with rising operational costs and sustainability mandates.

We can help! Our analysts can customize this data center gpu market research report to meet your requirements.

RIA -

RIA -