Education Hardware Market Size 2024-2028

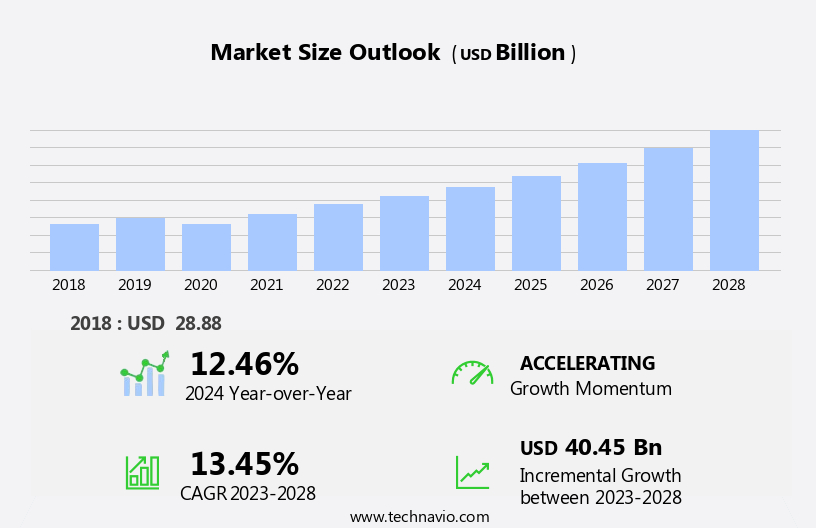

The education hardware market size is forecast to increase by USD 40.45 billion at a CAGR of 13.45% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing adoption of technology in educational institutions. Online learning platforms, digital content, and assessment tools are becoming increasingly popular, driving the demand for education hardware. This trend is particularly noticeable in the focus on Science, Technology, Engineering, and Mathematics (STEM) education, where advanced hardware is essential for delivering effective instruction. However, the high cost of education hardware remains a significant challenge for many institutions and students, limiting the widespread adoption of these technologies.

- Despite this obstacle, companies seeking to capitalize on market opportunities in the market can focus on developing cost-effective solutions while maintaining the necessary performance and functionality to meet the demands of modern education. By addressing this challenge, these companies can help make technology-enhanced learning more accessible and affordable, expanding the market and driving growth.

What will be the Size of the Education Hardware Market during the forecast period?

- The market continues to evolve, driven by advancements in technology and the shifting educational landscape. Digital resources, such as educational platforms, laptops, and interactive whiteboards, are increasingly integrated into curriculum development and educational institutions. Online learning and artificial intelligence are transforming higher education, enabling personalized learning experiences and enhancing student engagement. Communication tools and data privacy are crucial considerations in this digital age, ensuring secure and effective collaboration. Moreover, Education technology adoption extends to early childhood education, where digital literacy and interactive content are essential for fostering a strong foundation. K-12 education embraces digital textbooks, virtual labs, and assessment tools to enhance learning outcomes.

- Secondary education and STEM education leverage technology for augmented reality tools and adaptive learning, while professional development opportunities equip teachers with the necessary skills to effectively integrate technology into their classrooms. Network connectivity, cloud computing, and wireless networks are essential infrastructure components, enabling seamless access to digital content and online assessments. Tablets and laptops offer versatility and portability, while interactive whiteboards and digital signage facilitate engaging and collaborative learning environments. E-learning platforms and educational apps cater to diverse learning styles and preferences, while machine learning and adaptive learning technologies enable customized instruction. The market is a dynamic and evolving space, with ongoing innovations shaping the future of education.

- From primary to higher education, technology integration continues to redefine learning experiences, fostering digital citizenship and preparing students for the digital world.

How is this Education Hardware Industry segmented?

The education hardware industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- K-12 education

- Higher education

- Type

- PCs

- Interactive displays

- Classroom wearables

- VR/AR Device

- Deployment Type

- On-Premises

- Cloud-Integrated

- Service Mode

- Classroom Learning

- Remote Learning

- STEM Education

- Professional Development

- Geography

- North America

- US

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Middle East and Africa

- UAE

- APAC

- Australia

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

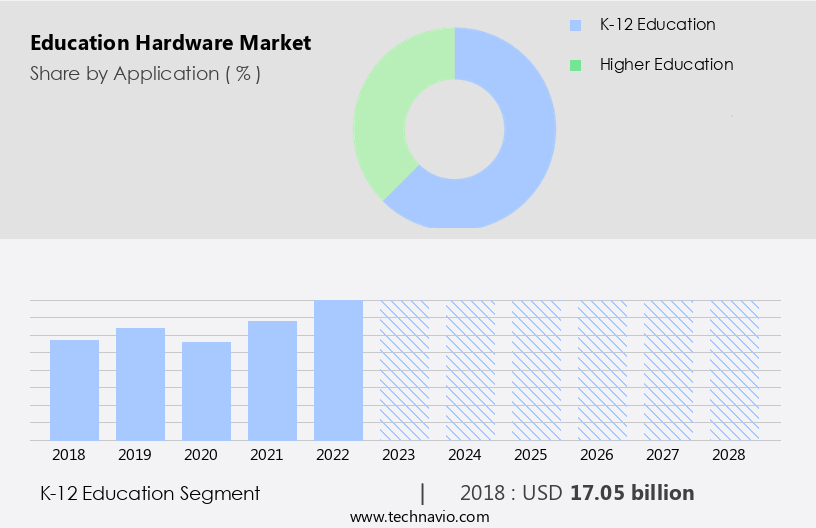

The k-12 education segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, particularly in the K-12 education segment. This sector's focus on interactive and technology-driven learning tools is propelling the demand for education hardware. Interactive displays and smart boards are leading the charge, enabling teachers to deliver engaging lessons through multimedia content and interactive activities. These technologies, including interactive whiteboards, are transforming classrooms by fostering collaboration and student engagement. Cloud computing, wireless networks, and digital textbooks are also essential components of the education hardware landscape, offering flexibility and convenience. Furthermore, artificial intelligence, machine learning, and adaptive learning are revolutionizing personalized education, while data privacy and security remain critical concerns.

Virtual reality headsets and educational games are also gaining popularity, adding a new dimension to learning experiences. Educational institutions are increasingly integrating technology into their curriculum development and teacher training programs, with e-learning platforms, communication tools, and student response systems becoming essential components. The higher education sector is also embracing technology, with laptops and tablets becoming standard tools for learning. The market is a dynamic and evolving space, with learning analytics, digital content, and online assessments playing crucial roles in enhancing learning outcomes.

The K-12 education segment was valued at USD 17.05 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

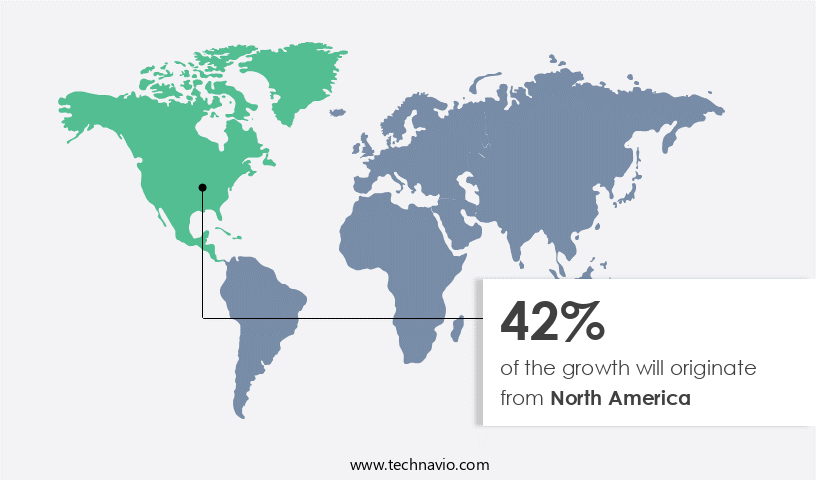

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic realm of educational technology, big data is increasingly shaping learning experiences by providing valuable insights for curriculum development and personalized instruction. Network connectivity, a fundamental requirement for data exchange, is becoming ubiquitous in educational institutions, enabling real-time collaboration and online learning. Early childhood education is embracing digital textbooks and interactive content, while virtual labs offer hands-on experiences for students in STEM fields. Assessment tools and student response systems facilitate ongoing evaluation, enhancing learning outcomes. Teacher training programs are adopting technology, integrating artificial intelligence and machine learning for adaptive learning and professional development. Cloud computing and wireless networks ensure access to educational resources, enabling blended learning and online assessments.

Digital literacy and digital citizenship are essential skills for students, fostering collaboration through communication tools and educational apps. Virtual reality headsets and augmented reality tools offer immersive learning experiences, while educational software caters to K-12 and higher education. Learning management systems facilitate curriculum development and student engagement, while data privacy remains a crucial concern. Online learning platforms and e-learning apps cater to diverse learning styles, offering interactive content and personalized learning experiences. School districts and educational institutions are investing in technology integration, from laptops and tablets for education to interactive whiteboards and digital signage. Classroom technology, including student engagement tools and communication systems, fosters a harmonious learning environment. Technology adoption continues to emphasize the importance of learning analytics, enabling educators to optimize instruction and improve student performance.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is evolving rapidly, fueled by demand for interactive whiteboards for classrooms and educational laptops for remote learning. As hybrid models expand, education hardware for hybrid learning and durable laptops for student use are becoming essential. Schools are adopting smart projectors for schools, classroom tablets for e-learning, and VR headsets for education to enrich student engagement. Key education hardware market trends include 3D printers for STEM education, AR devices for educational training, and AI-integrated classroom technology. Institutions are investing in cloud-connected classroom projectors, IoT-enabled classroom devices, and secure education hardware solutions. From portable devices for mobile learning to eco-friendly education hardware, the market supports digital transformation across K-12 and universities, with a focus on affordable tablets for schools and smartboards for interactive teaching.

What are the key market drivers leading to the rise in the adoption of Education Hardware Industry?

- The increasing implementation of online learning platforms, digital content, and assessment tools within educational institutions is the primary market driver.

- The global education market has experienced notable growth in the implementation of digital tools and technologies, particularly in the realm of stem education and k-12 institutions. This shift is driven by the demand for more immersive, harmonious, and adaptive learning experiences. Educational software, such as machine learning and adaptive learning platforms, are increasingly utilized to cater to individual students' needs. Interactive content, educational apps, collaboration tools, and learning management systems are becoming integral components of modern educational practices. Schools and districts are investing in these solutions to provide students with a blended learning experience, combining traditional classroom instruction with digital resources.

- This digital transformation is essential for enhancing the learning experience, making education more accessible, and preparing students for the future workforce.

What are the market trends shaping the Education Hardware Industry?

- The growing emphasis on STEM reflects a significant market trend. As a professional, it is essential to keep abreast of this development and adapt accordingly.

- The market is experiencing significant growth due to the increasing prioritization of STEM (Science, Technology, Engineering, and Mathematics) education. This shift in focus is driven by the recognition of the importance of STEM fields in preparing students for future careers. One of the key areas of innovation in this space is the development of educational toys that promote STEM learning. These toys, which include coding and robotics kits, are in high demand as parents and educators seek to develop computational thinking and problem-solving abilities in students. Another significant trend in the market is the integration of technology into the classroom.

- This includes the use of digital textbooks, virtual labs, assessment tools, and wireless networks. Cloud computing and tablet devices are also becoming increasingly popular, enabling access to vast amounts of educational resources and facilitating remote learning. Moreover, technology is also being used to enhance teacher training and professional development. Learning analytics and digital citizenship are key areas of focus, with virtual reality headsets and other immersive technologies being explored to create harmonious and engaging learning experiences. Overall, the market is undergoing a transformation, with a strong emphasis on innovation and the use of technology to enhance the learning experience.

What challenges does the Education Hardware Industry face during its growth?

- The escalating costs of educational hardware pose a significant challenge to the industry's growth trajectory. The market faces a substantial challenge due to the high cost of acquiring and maintaining necessary technology solutions for educational institutions and students. This financial barrier restricts accessibility and equity in the adoption of essential education hardware, including laptops for various educational levels and purposes, interactive whiteboards, and educational games. For instance, the cost of a general-purpose computer for education may range from USD500 to USD1,000, while specialized hardware, such as graphic design computers, can cost upwards of USD2,000. Peripherals like monitors, printers, and software further increase the overall expense. Moreover, the integration of advanced technologies like artificial intelligence, online learning platforms, and e-learning tools in education has become increasingly important for curriculum development and digital literacy.

- Communication tools and data privacy concerns are also essential considerations for educational institutions. Despite these challenges, the market for education hardware continues to evolve, with advancements in technology driving immersive and harmonious learning experiences. Online learning platforms and educational games offer engaging and interactive alternatives to traditional classroom settings. As educational institutions and students navigate the complexities of the market, understanding the costs and benefits of various technology solutions will be crucial for making informed decisions.

Exclusive Customer Landscape

The education hardware market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the education hardware market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, education hardware market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acer - This company specializes in providing top-tier education hardware solutions. Among the offerings are the Acer Chromebook Spin 713 (model CP713 3W), Dell Latitude 7410 Chromebook Enterprise, and HP Elite Dragonfly 13.5 Chromebook. Each device is meticulously selected to ensure optimal performance and reliability in an educational setting.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acer

- Apple

- Asus

- BenQ

- Boxlight

- Cisco Systems

- Dell Technologies

- Epson

- Hitachi

- HP Inc.

- Lenovo

- Microsoft

- NEC Corporation

- Panasonic

- Promethean

- Samsung Electronics

- SMART Technologies

- Sony

- ViewSonic

- Vivitek

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Education Hardware Market

- In January 2024, Microsoft Corporation announced the global availability of its new Surface Hub 2S interactive whiteboard, designed for modern classroom settings. This innovative hardware solution, featuring a 50.5-inch 4K+ touchscreen and improved pen technology, aims to enhance collaborative learning experiences (Microsoft Press Release, 2024).

- In March 2025, Apple Inc. And Google joined forces to invest in a multi-year partnership with Clemson University to create a state-of-the-art facility for research and development in education technology. This collaboration will focus on integrating advanced hardware and software solutions to improve access to technology-driven education (Apple Newsroom, 2025).

- In May 2024, Lenovo Group Ltd. Acquired MoboSystems, a leading provider of educational software and hardware solutions. This strategic acquisition will allow Lenovo to expand its product offerings and strengthen its position in the education market (Lenovo Press Release, 2024).

Research Analyst Overview

The market is experiencing significant shifts as technology integration becomes increasingly essential for student-centered learning. Tech support plays a crucial role in ensuring seamless implementation of mobile learning, online tutoring, and virtual classrooms. Differentiated instruction and personalized learning pathways are driving demand for IT infrastructure capable of handling data analytics and personalized learning recommendations. Green technology is gaining traction, with cloud-based solutions and live streaming enabling inclusive learning and reducing carbon footprints. Hybrid learning models combine the benefits of in-person and remote instruction, while project-based learning and video conferencing foster collaborative learning experiences.

Digital assessments and predictive analytics offer valuable insights, enhancing the effectiveness of instruction and addressing the digital divide. Open educational resources and digital literacy training ensure equitable access to quality education. The market's focus on inclusive learning and return on investment underscores the importance of investing in robust IT infrastructure and innovative solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Education Hardware Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.45% |

|

Market growth 2024-2028 |

USD 40.45 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.46 |

|

Key countries |

US, China, Germany, Japan, UK, Australia, India, France, Brazil, UAE, Rest of World (ROW), Saudi Arabia, France, South Korea, Mexico, Italy, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Education Hardware Market Research and Growth Report?

- CAGR of the Education Hardware industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the education hardware market growth of industry companies

We can help! Our analysts can customize this education hardware market research report to meet your requirements.

RIA -

RIA -