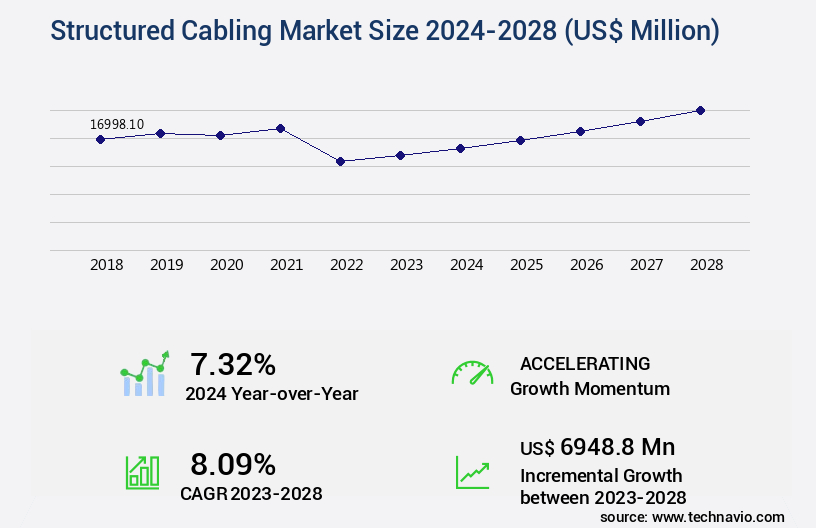

Structured Cabling Market Size 2024-2028

The structured cabling market size is valued to increase USD 6.95 billion, at a CAGR of 8.09% from 2023 to 2028. Increasing investments in data centers will drive the structured cabling market.

Major Market Trends & Insights

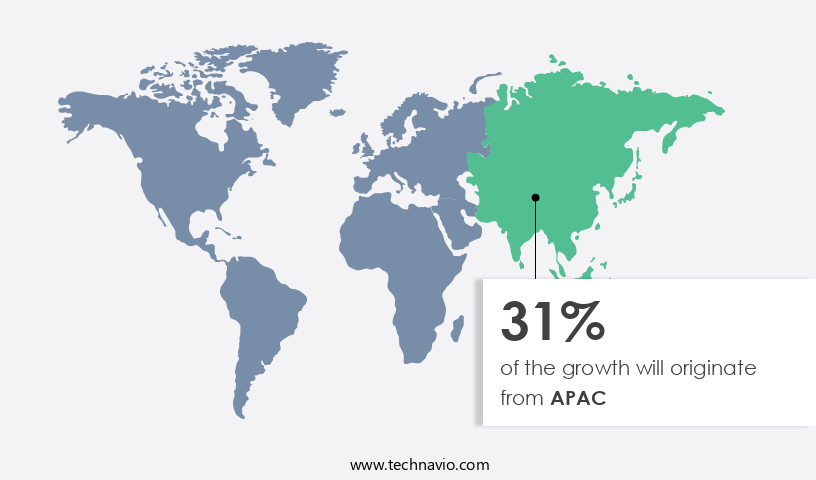

- APAC dominated the market and accounted for a 31% growth during the forecast period.

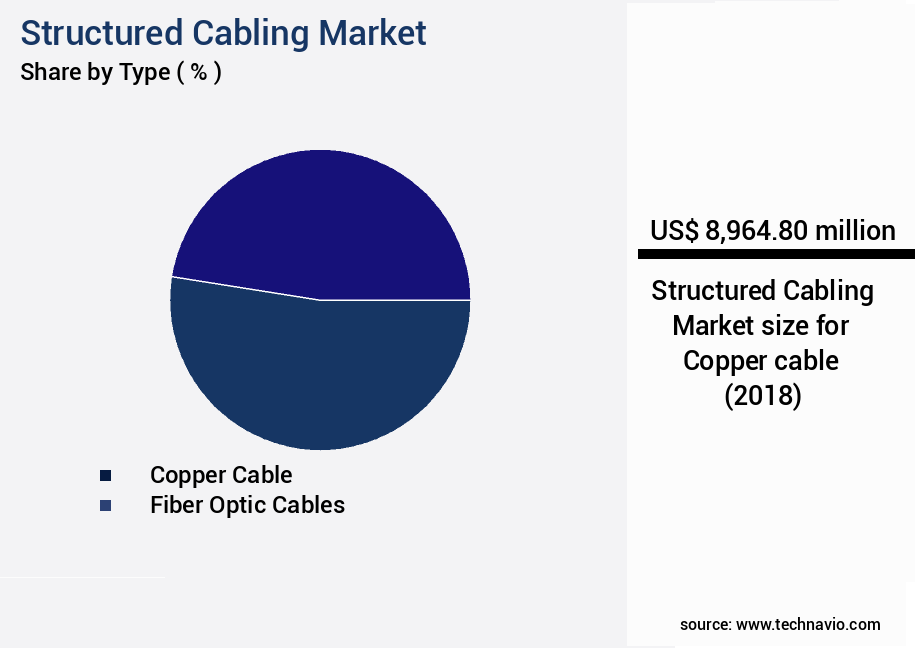

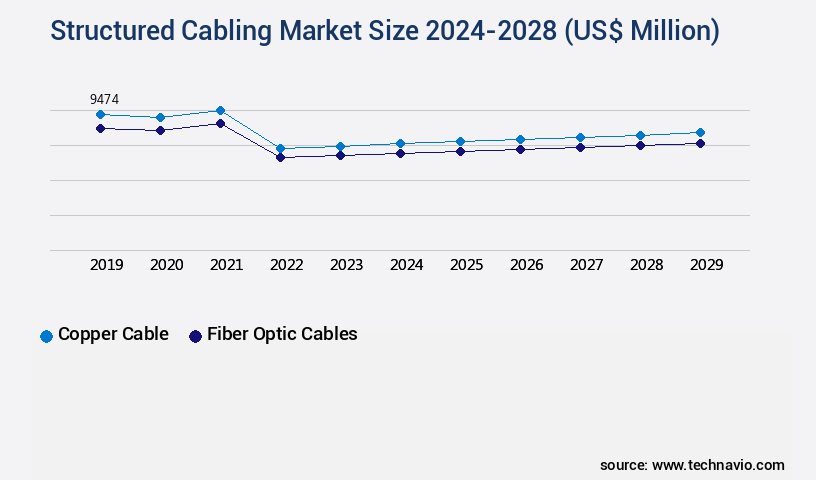

- By Type - Copper cable segment was valued at USD 8.96 billion in 2022

- By Application - Data center segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 26.90 million

- Market Future Opportunities: USD 6948.80 million

- CAGR from 2023 to 2028 : 8.09%

Market Summary

- The market encompasses the production and installation of specialized cabling systems used for telecommunications and data transfer within buildings and campuses. This market is characterized by continuous evolution, driven by several key factors. Core technologies, such as fiber optics and copper cabling, are advancing rapidly, enabling higher bandwidth and faster data transfer speeds. Applications, particularly in sectors like telecommunications, healthcare, and education, are expanding, fueling demand for reliable and efficient cabling solutions. Service types, including installation, maintenance, and consulting, are evolving to meet the growing complexity of cabling infrastructure. Meanwhile, regulations, such as BICSI and TIA/EIA standards, ensure consistency and quality in cabling installations.

- Volatility in raw material prices poses a challenge, but increasing investments in data centers and the emergence of cloud computing technology offer significant opportunities. According to a recent report, the fiber optics segment is projected to account for over 40% of the market share by 2026, underscoring the sector's dynamic nature.

What will be the Size of the Structured Cabling Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Structured Cabling Market Segmented ?

The structured cabling industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Copper cable

- Fiber optic cables

- Application

- Data center

- Telecommunications

- Industrial

- Buildings

- End-User

- IT & Telecom

- Healthcare

- Manufacturing

- Government

- Geography

- North America

- US

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Middle East and Africa

- UAE

- APAC

- Australia

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The copper cable segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, copper cables continue to dominate, accounting for the largest market share in 2023. Copper's effectiveness in transmitting data over short to medium distances makes it a preferred choice for various applications, including data centers and desktop connections. The copper wire and cable industry experiences growth due to increasing energy needs and substantial construction investments. Furthermore, the expansion of smart grids and the enhancement of power transmission and distribution systems fuel the demand for copper cables. High-speed data transmission requirements, cable labeling systems, and cabling standards compliance are key factors driving the evolution of network infrastructure design.

Cable termination techniques, bandwidth capacity planning, and cable routing optimization are essential for network connectivity solutions. Cable testing equipment, cabling installation methods, and cable tray management are crucial components of network cabling infrastructure. Network performance metrics, security cabling practices, and cable pathway design are integral to maintaining network efficiency and reliability. The integration of wireless networks and the implementation of fiber optic and twisted pair cabling systems further expand the market's scope. Overall, the market continues to evolve, addressing the needs of various industries and applications.

The Copper cable segment was valued at USD 8.96 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 31% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Structured Cabling Market Demand is Rising in APAC Request Free Sample

The market, a crucial component of the IT infrastructure sector, experienced significant growth in 2022, with the data center segment leading the charge. In North America, the data center market's dominance became increasingly apparent. This trend was driven by the increasing number of data center establishments in the region, which in turn fueled the demand for IT infrastructure and related cabling solutions. Technavio anticipates that North America will continue to lead the market throughout the forecast period.

This prediction is based on the numerous data centers currently under construction, slated for completion by the end of the forecast period. These upcoming data centers represent substantial investments, necessitating purchases of IT infrastructure, power and cooling systems, and associated accessories.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market plays a pivotal role in enhancing network performance by optimizing cable routing for data centers and large buildings. Implementing TIA-568 cabling standards is crucial for choosing the right cabling for high-speed networks, ensuring compatibility and interoperability. In industrial settings, best practices for cabling include designing scalable systems for future growth, reducing cable clutter, and improving accessibility. Preventative maintenance for cabling systems is essential to minimize downtime and maintain optimal network performance. Integrating structured cabling with cloud services and building automation systems is a growing trend, enabling seamless data transfer and improving overall efficiency. Measuring network performance after cabling upgrades is vital for identifying potential issues and ensuring the success of these projects.

In the data center sector, implementing fiber optic cabling and advanced cable management techniques in server rooms have become standard practices. According to market intelligence, more than 70% of new cabling projects focus on large buildings and data centers. This significant share underscores the importance of structured cabling in supporting the growing demand for high-speed connectivity and data-intensive applications. Ensuring security and compliance with cabling systems is another critical consideration, as the risks of data breaches and non-compliance can lead to costly consequences. Comparatively, the industrial application segment accounts for a significantly larger share of the market compared to the academic sector.

This disparity highlights the importance of reliable and robust cabling solutions in industrial settings, where network uptime and data security are paramount. Troubleshooting common cabling infrastructure issues and employing cost-effective strategies for cabling projects are essential for maintaining a competitive edge in this market. Proper cable labeling and documentation are indispensable for managing complex cabling systems. Using network monitoring tools to optimize cabling systems and identifying potential issues before they become critical is a best practice that can save organizations time and resources. The role of cabling in network security is increasingly recognized, with the implementation of advanced security features becoming a priority for many organizations.

What are the key market drivers leading to the rise in the adoption of Structured Cabling Industry?

- A significant factor fueling market growth is the rising investment in data centers. This trend reflects the increasing demand for advanced technological infrastructure to support business operations and digital transformation initiatives.

- Data center structured cabling investments have experienced significant growth due to the increasing importance of efficient and dependable data center operations. Structured cabling systems offer numerous advantages, such as increased equipment return on investment, decreased operating expenses, expanded growth and resilience, enhanced risk management, and heightened visibility. The proliferation of cloud computing, the transition to faster speeds, the expansion of edge computing, and the escalating demand for greater bandwidth are primary catalysts fueling the surge in investments in structured cabling within data centers. Moreover, the requirement for adaptable and reliable cabling solutions to accommodate the escalating data traffic volume, technological advancements, and the demand for streamlined connectivity are additional factors driving the expansion and investments in data center structured cabling.

What are the market trends shaping the Structured Cabling Industry?

- Cloud computing technology, which is on the rise, represents the latest market trend.

- On-premises data centers are increasingly perceived as a drain on resources for organizations, offering limited strategic value. In contrast, the shift towards cloud computing empowers businesses with flexibility, enhanced compute power, and agility essential for growth. Maintaining on-premises data centers is a costly and complex endeavor, compelling companies to reallocate their resources towards more strategic initiatives. Cloud computing enables businesses to hire talent globally and pursue new opportunities regardless of geographic boundaries.

- The benefits of cloud services extend beyond cost savings, as they offer scalability, reliability, and improved disaster recovery capabilities. These trends underscore the evolving nature of the market, with businesses continually seeking to optimize their IT infrastructure and adapt to the dynamic business landscape.

What challenges does the Structured Cabling Industry face during its growth?

- The volatile pricing of raw materials poses a significant challenge to the industry's growth trajectory.

- Aluminum and copper are the primary raw materials in the production of structured cabling systems, accounting for a significant portion of manufacturers' costs. Aluminum conductors, coated with copper, are lighter than solid copper cables and offer excellent performance in extreme conditions, making them ideal for various industries. The prices of these materials are subject to various influences, including inflation, availability, and production costs.

- Approximately 85% of the total production cost is attributed to material expenses. The volatile nature of raw material prices, particularly aluminum and copper, significantly impacts the revenue or cost of sales for cable manufacturers. The high melting points and ruggedness of these materials make them indispensable in industries where durability and resilience are crucial factors.

Exclusive Technavio Analysis on Customer Landscape

The structured cabling market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the structured cabling market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Structured Cabling Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, structured cabling market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CommScope - This company specializes in providing comprehensive structured cabling offerings, encompassing cable ties, tools and accessories, grounding systems, wire termination tools, wiring ducts, and trunking. Their product range caters to various cabling needs, ensuring optimal network performance and reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CommScope

- Panduit

- Legrand

- Corning

- Belden

- Nexans

- Schneider Electric

- Siemens

- ABB

- Anixter

- Superior Essex

- General Cable

- Hubbell

- Leviton

- TE Connectivity

- Furukawa Electric

- HellermannTyton

- R&M

- Oberon

- Chatsworth Products

- Tripp Lite

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Structured Cabling Market

- In January 2024, Belden Inc., a leading provider of signal transmission solutions, announced the launch of their new Ravenna high-performance networking solution for professional audio applications (Belden Inc. Press release). This innovative structured cabling system offers enhanced synchronization and reduced latency, catering to the growing demand for high-quality audio in various industries, including live events and broadcasting.

- In March 2024, TE Connectivity and CommScope, two major players in the market, entered into a strategic collaboration to expand their joint offering of end-to-end connectivity solutions (TE Connectivity press release). This partnership aimed to provide customers with a comprehensive suite of products and services, strengthening their competitive position in the market.

- In May 2024, Legrand, a global specialist in electrical and digital building infrastructures, completed the acquisition of Nexans' Building Cables business, significantly expanding its structured cabling portfolio (Legrand press release). This strategic move enabled Legrand to broaden its product range and geographic reach, bolstering its position as a leading player in the industry.

- In April 2025, the Telecommunications Industry Association (TIA) approved the new TIA-1172-D standard for twisted-pair cabling systems, setting new performance requirements for Cat. 8.2 and Cat. 8.1 cables (TIA press release). This regulatory approval marked a significant technological advancement, enabling higher bandwidth and faster data transfer rates for structured cabling systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Structured Cabling Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.09% |

|

Market growth 2024-2028 |

USD 6948.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Key countries |

US, China, Germany, Japan, UK, Australia, India, France, Brazil, UAE, Rest of World (ROW), Saudi Arabia, France, South Korea, Mexico, Italy, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving landscape, characterized by ongoing advancements and innovations in cable labeling systems, cabling standards compliance, and network infrastructure design. Horizontal cabling systems, including coaxial cabling and copper cable types, continue to play a crucial role in facilitating high-speed data transmission and building automation systems. Cable termination techniques and cable routing optimization have gained significant attention, with the increasing demand for network connectivity solutions and data center cabling. Bandwidth capacity planning and cable testing equipment are essential components of network infrastructure design, ensuring optimal network performance metrics and security cabling practices. Moreover, the market is witnessing a growing trend towards cable tray management, backbone cabling design, and wiring closet organization.

- The integration of wireless network systems with structured media pathways and patch panel management further enhances network connectivity and flexibility. Fiber optic cabling and twisted pair cabling are prominent low-voltage cabling systems, each offering distinct advantages in terms of bandwidth capacity and transmission distance. Cable pathway design and network cabling infrastructure are critical aspects of ensuring efficient and reliable network operations. In the realm of high-speed data transmission, cable labeling systems are increasingly important for effective cable management and network maintenance. As network infrastructure becomes more complex, the need for advanced cable testing equipment and cable termination techniques becomes increasingly apparent.

- In summary, the market is a vibrant and continually evolving space, marked by ongoing advancements in cabling technologies, network infrastructure design, and cable management solutions. These trends reflect the growing importance of reliable and efficient network connectivity in today's digital economy.

What are the Key Data Covered in this Structured Cabling Market Research and Growth Report?

-

What is the expected growth of the Structured Cabling Market between 2024 and 2028?

-

USD 6.95 billion, at a CAGR of 8.09%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Copper cable and Fiber optic cables), Application (Data center, Telecommunications, Industrial, and Buildings), Geography (North America, Europe, APAC, South America, and Middle East and Africa), and End-User (IT & Telecom, Healthcare, Manufacturing, and Government)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing investments in data centers, Volatile raw material prices

-

-

Who are the major players in the Structured Cabling Market?

-

CommScope, Panduit, Legrand, Corning, Belden, Nexans, Schneider Electric, Siemens, ABB, Anixter, Superior Essex, General Cable, Hubbell, Leviton, TE Connectivity, Furukawa Electric, HellermannTyton, R&M, Oberon, Chatsworth Products, and Tripp Lite

-

Market Research Insights

- The market encompasses the design, installation, and maintenance of cabling infrastructure for data communication networks. This market continues to evolve, with key components including copper cable crimping, remote network management, signal attenuation, and network documentation. Copper cable accounts for a significant portion of this market, with over 70% of installed cabling being copper. In contrast, fiber optic cable, while more expensive, offers higher bandwidth and lower signal attenuation, making it the preferred choice for high-speed networks. Network documentation and cable testing methodologies are essential for ensuring network performance and fault tolerance. Physical layer design, cabling material selection, and network topology design are crucial factors in cable infrastructure design.

- Data rate requirements, network fault tolerance, and network security protocols are integral to network functionality. Network monitoring tools, project management tools, and system uptime monitoring are essential for maintaining network performance. With the increasing adoption of cloud network connectivity, bandwidth utilization, latency and jitter become critical concerns. Cable length limitations and link aggregation techniques are also important considerations in cable infrastructure design. Certification of cabling systems ensures compliance with industry standards.

We can help! Our analysts can customize this structured cabling market research report to meet your requirements.

RIA -

RIA -