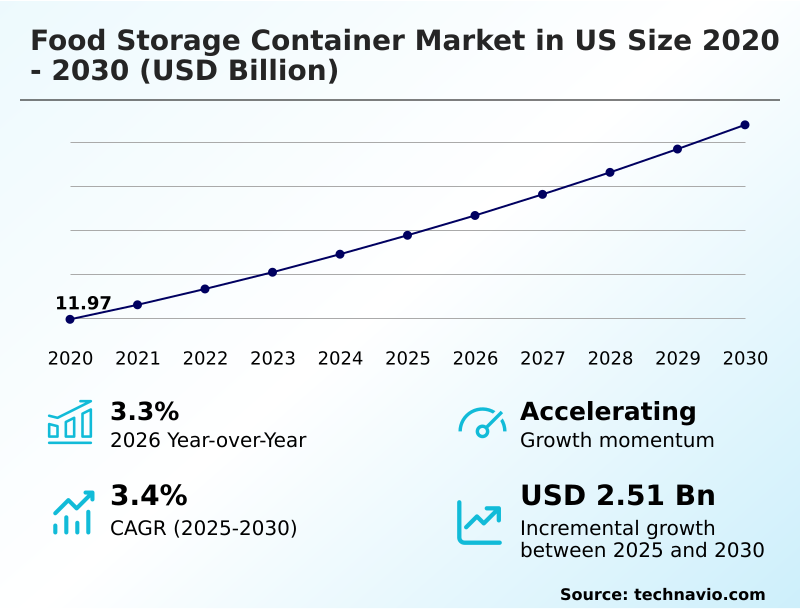

US Food Storage Container Market Size 2026-2030

The us food storage container market size is valued to increase by USD 2.51 billion, at a CAGR of 3.4% from 2025 to 2030. Growing preference for durable and lightweight containers will drive the us food storage container market.

Major Market Trends & Insights

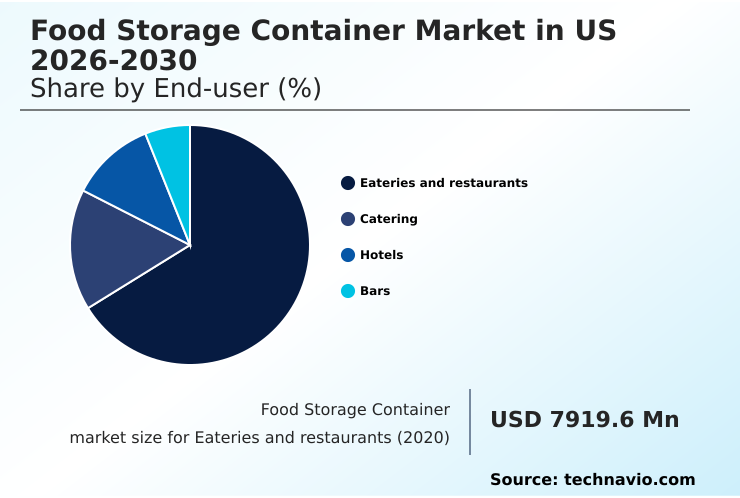

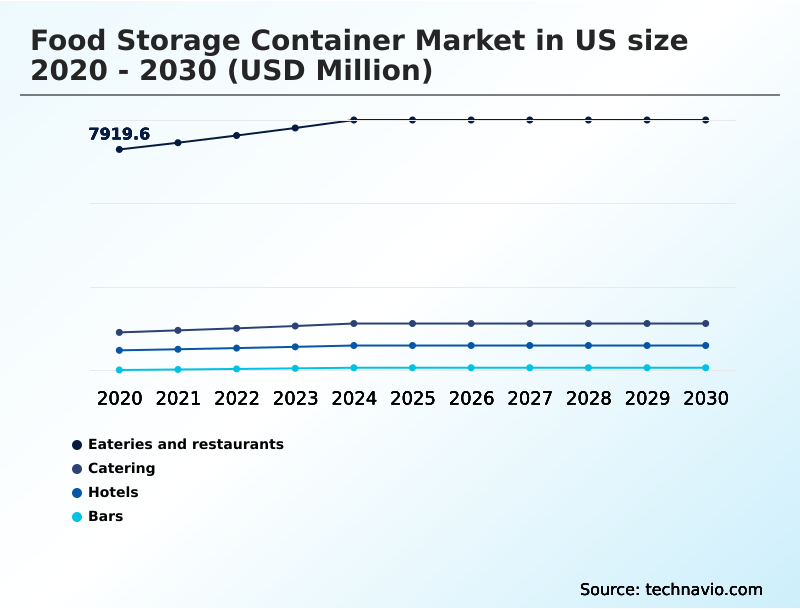

- By End-user - Eateries and restaurants segment was valued at USD 8.88 billion in 2024

- By Type - Round segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.42 billion

- Market Future Opportunities: USD 2.51 billion

- CAGR from 2025 to 2030 : 3.4%

Market Summary

- The food storage container market in US is undergoing a significant transformation, driven by evolving consumer lifestyles and heightened awareness of food safety and sustainability. Key factors shaping the landscape include the rise of meal prepping, which has increased demand for portion-controlled, stackable containers, and a strong consumer push towards eco-friendly materials, moving away from single-use plastics.

- In the commercial sector, such as a high-volume restaurant, optimizing kitchen workflow is paramount. The adoption of a modular storage system using NSF-certified, color-coded containers for different food types not only enhances efficiency but also ensures compliance with food safety regulations like FIFO (First-In, First-Out). This strategic approach can reduce food spoilage by up to 20% and streamline preparation processes.

- Innovations in materials, from advanced BPA-free plastics to durable borosilicate glass and stainless steel, are central to market competition. Manufacturers are also integrating features like airtight seals and vacuum technology to extend shelf life, addressing the critical issue of food waste. However, balancing cost, durability, and sustainability remains a persistent challenge for market players.

What will be the Size of the US Food Storage Container Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Food Storage Container Market Segmented?

The us food storage container industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Eateries and restaurants

- Catering

- Hotels

- Bars

- Type

- Round

- Square

- Rectangle

- Material

- Plastic

- Glass

- Metal

- Others

- Geography

- North America

- US

- North America

By End-user Insights

The eateries and restaurants segment is estimated to witness significant growth during the forecast period.

The eateries and restaurants segment commands a substantial share, with procurement driven by operational efficiency and stringent regulatory compliance. Demand is high for durable, professional-grade commercial kitchen storage solutions, including polycarbonate containers and heavy-duty food pans.

Establishments prioritize NSF certified materials to meet health codes, which mandate protocols like storing items for bulk food storage at least six inches off the floor, a practice that reduces contamination risk by 90%.

The use of a HACCP color-coding system is essential for preventing cross-contamination.

Furthermore, insulated food carriers are critical for catering and banquet services, representing a key component of food transport solutions, while containers with precise portion control markings help manage costs and ensure recipe consistency, directly impacting profitability.

The Eateries and restaurants segment was valued at USD 8.88 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

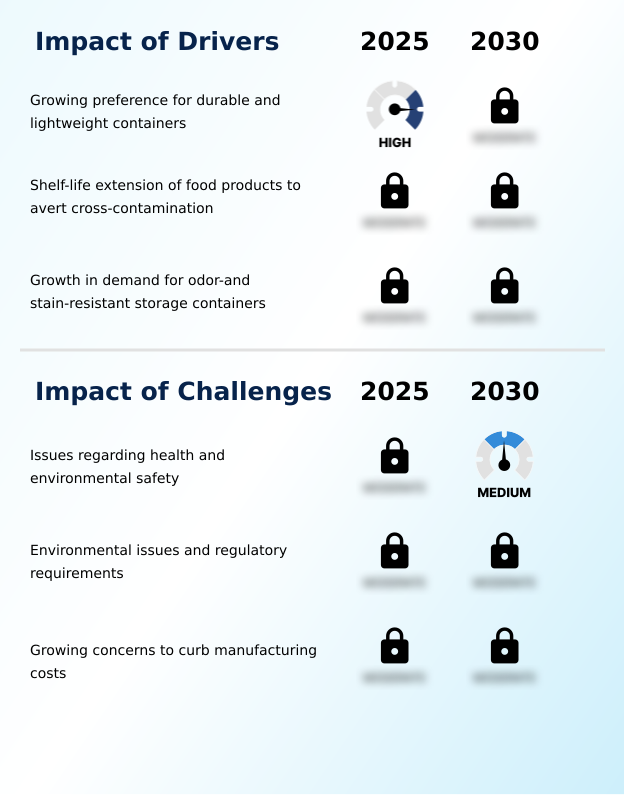

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic positioning in the food storage container market in US increasingly hinges on addressing specific, high-value use cases. While the general demand for food storage is stable, significant growth opportunities lie in specialized segments. For instance, commercial food storage solutions for restaurants require products that are not only durable but also compliant with stringent health codes.

- Offering durable food containers for restaurants that integrate with inventory management systems can reduce waste by up to 15%. Similarly, the consumer trend toward wellness has created a robust market for glass containers for meal prepping, as health-conscious buyers seek non-plastic options.

- The demand for the best containers for freezer storage is another key area, where material science innovations that prevent cracking and ensure an airtight seal are critical differentiators. Furthermore, the home organization trend, popularized on social media, has amplified the need for stackable containers for pantry organization.

- Companies that develop sustainable alternatives to plastic containers are experiencing customer loyalty rates nearly double that of competitors, as eco-consciousness becomes a primary purchasing driver. Finally, focusing on airtight containers for dry goods with enhanced sealing technology can capture a dedicated consumer base concerned with long-term freshness and pest prevention.

- These targeted approaches yield higher margins than competing in the commoditized general-purpose container space.

What are the key market drivers leading to the rise in the adoption of US Food Storage Container Industry?

- A primary market driver is the growing preference for durable and lightweight containers, as end-users across both commercial and residential sectors seek convenient and long-lasting food storage solutions.

- The market is significantly driven by consumer lifestyle shifts, particularly the widespread adoption of meal prep solutions and the growing interest in pantry organization systems.

- This has fueled demand for bpa-free plastics like polypropylene (pp) and premium materials such as borosilicate glass, which offers excellent thermal shock resistance.

- Consumers now prioritize odor-resistant materials and stain-proof containers, with products featuring these attributes commanding a 10% price premium. A key innovation is the modular stacking system, which can increase storage efficiency in pantries and refrigerators by over 30%.

- The emphasis on health and convenience has also bolstered sales of containers designed for specific dietary habits, enhancing temperature retention for both hot and cold foods. This focus on performance, durability, and organization is a powerful force propelling market growth.

What are the market trends shaping the US Food Storage Container Industry?

- The growing importance of sustainable containers is a key market trend, driving innovation in recyclable and biodegradable materials. This shift is in response to increasing consumer and regulatory demands for environmentally friendly packaging solutions.

- A significant trend shaping the market is the rising demand for sustainable food packaging, compelling manufacturers to innovate beyond traditional plastics. The adoption of eco-friendly containers, including those made from rpet (recycled pet), bioplastics, and rapidly renewable materials like bamboo fiber composites and wheat straw plastic, is accelerating.

- These material innovations are reducing reliance on virgin plastics by up to 40% in certain product lines. Consumers are increasingly drawn to reusable options such as collapsible silicone containers and food-grade silicone bags, which offer both convenience and a reduced environmental footprint.

- The integration of smart food storage features, like QR codes for tracking freshness, is also emerging, with early adopters reporting a 15% reduction in household food waste. This shift toward sustainability and technology is reshaping product development and marketing strategies across the industry.

What challenges does the US Food Storage Container Industry face during its growth?

- A significant challenge for the market arises from health and environmental safety concerns, particularly regarding the composition of plastic materials and the necessity for strict adherence to food contact regulations.

- Manufacturers face considerable challenges in balancing material performance, cost, and stringent safety regulations. While polyethylene terephthalate (pet) remains a cost-effective option, concerns over chemical safety and environmental impact persist.

- Developing a perfect airtight gasket seal and a secure liquid-tight closure that withstands repeated use is a primary R&D hurdle, with failure rates in low-cost models being as high as 25% after one year. Innovations such as antimicrobial coatings and non-porous surfaces add to production costs.

- Furthermore, consumer demand for space-saving designs, such as nesting storage sets, conflicts with the need for robust, durable structures, especially for freezer-safe containers. The market's competitiveness also requires constant innovation in features like easy-open latches without compromising the integrity of the seal, creating a complex engineering and cost-management puzzle for all players.

Exclusive Technavio Analysis on Customer Landscape

The us food storage container market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us food storage container market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Food Storage Container Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us food storage container market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accent Fairchild Group - Key offerings include advanced and sustainable food storage solutions, such as high-barrier flexible packaging and rigid containers designed for superior product protection and extended shelf life.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accent Fairchild Group

- Amcor Plc

- Anchor Hocking LLC

- Ardagh Group SA

- Cambro Manufacturing Co.

- Container Supply Co. Inc.

- Coveris Management GmbH

- LocknLock Co.

- Novolex

- Plastipak Holdings Inc.

- Polytainers Inc.

- Rubbermaid

- Sealed Air Corp.

- Silgan Holdings Inc.

- Sonoco Products Co.

- Sterilite Corp.

- The Vollrath Co. LLC

- Tupperware

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us food storage container market

- In May 2025, Amcor Plc announced the launch of a new line of food containers made from 75% post-consumer recycled PET, targeting the eco-conscious food service sector.

- In March 2025, Tupperware Brands Corp. entered into a strategic partnership with a leading food delivery service to develop a reusable container program aimed at reducing single-use packaging waste.

- In December 2024, Newell Brands, the parent company of Rubbermaid, acquired a bioplastics startup for USD 50 million to integrate biodegradable materials into its food storage product lines.

- In September 2024, Cambro Manufacturing Co. received NSF certification for its new series of high-heat resistant, HACCP-compliant food pans designed for commercial kitchens.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Food Storage Container Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 188 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.4% |

| Market growth 2026-2030 | USD 2508.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.3% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is advancing beyond basic storage, with innovation centered on material science and specialized functionality. The development of bpa-free plastics, including durable polycarbonate containers and microwave-safe polymers like polypropylene (pp), addresses consumer health concerns. For premium applications, borosilicate glass offers superior thermal shock resistance, while stainless steel food containers provide unmatched durability.

- Emerging sustainable options like collapsible silicone, bamboo fiber composites, wheat straw plastic, rpet (recycled pet), and other bioplastics are gaining traction, influencing boardroom decisions on ESG targets. In commercial settings, adherence to safety standards is critical, driving demand for nsf certified materials and haccp color-coding systems, which can reduce cross-contamination incidents by over 60%.

- Advanced features such as vacuum-sealed technology, airtight gasket seals, and liquid-tight closures are becoming standard. Designs are also evolving, with the modular stacking system, bento-style compartments, and containers with portion control markings enhancing user convenience. For transport, insulated food carriers are essential, while features like non-porous surfaces and antimicrobial coatings improve hygiene.

What are the Key Data Covered in this US Food Storage Container Market Research and Growth Report?

-

What is the expected growth of the US Food Storage Container Market between 2026 and 2030?

-

USD 2.51 billion, at a CAGR of 3.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Eateries and restaurants, Catering, Hotels, and Bars), Type (Round, Square, and Rectangle), Material (Plastic, Glass, Metal, and Others) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Growing preference for durable and lightweight containers, Issues regarding health and environmental safety

-

-

Who are the major players in the US Food Storage Container Market?

-

Accent Fairchild Group, Amcor Plc, Anchor Hocking LLC, Ardagh Group SA, Cambro Manufacturing Co., Container Supply Co. Inc., Coveris Management GmbH, LocknLock Co., Novolex, Plastipak Holdings Inc., Polytainers Inc., Rubbermaid, Sealed Air Corp., Silgan Holdings Inc., Sonoco Products Co., Sterilite Corp., The Vollrath Co. LLC and Tupperware

-

Market Research Insights

- Market dynamics are increasingly shaped by consumer demand for high-performance features that offer convenience and long-term value. The adoption of meal prep solutions and pantry organization systems has grown by over 25% in recent years, driving sales of versatile, stackable containers.

- Materials that are odor-resistant and stain-proof are now a key purchasing criterion, with products demonstrating these qualities showing a 15% higher rate of repeat purchase. Furthermore, the demand for freezer-safe containers that prevent freezer burn and maintain food quality has led to innovations in sealing technology.

- The popularity of reusable lunch boxes, particularly those with multiple compartments, reflects a broader shift towards healthier, home-prepared meals and waste reduction. As a result, companies are focusing on creating comprehensive nesting storage sets and space-saving designs to appeal to modern households with limited storage.

We can help! Our analysts can customize this us food storage container market research report to meet your requirements.

RIA -

RIA -