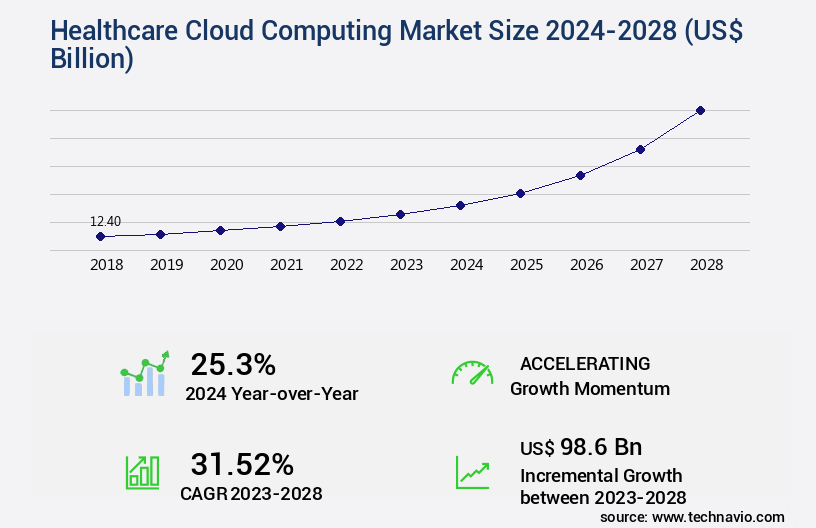

Healthcare Cloud Computing Market Size 2024-2028

The healthcare cloud computing market size is valued to increase by USD 98.6 billion, at a CAGR of 31.52% from 2023 to 2028. Integrated service offerings for healthcare will drive the healthcare cloud computing market.

Market Insights

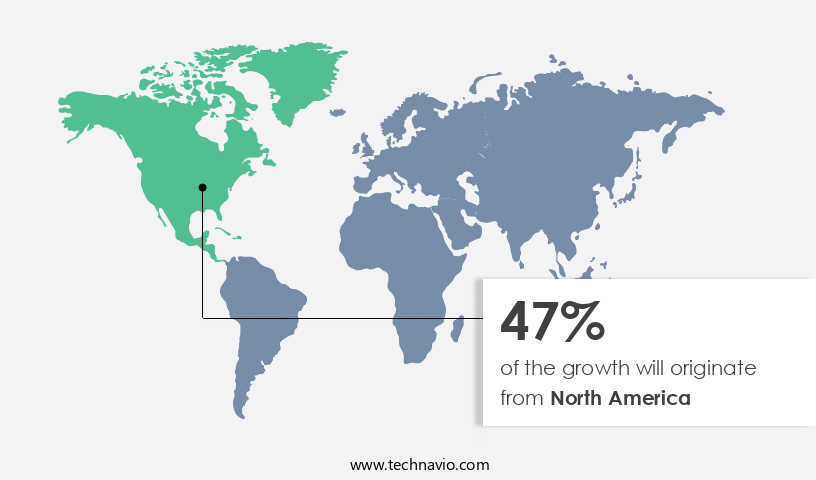

- North America dominated the market and accounted for a 47% growth during the 2024-2028.

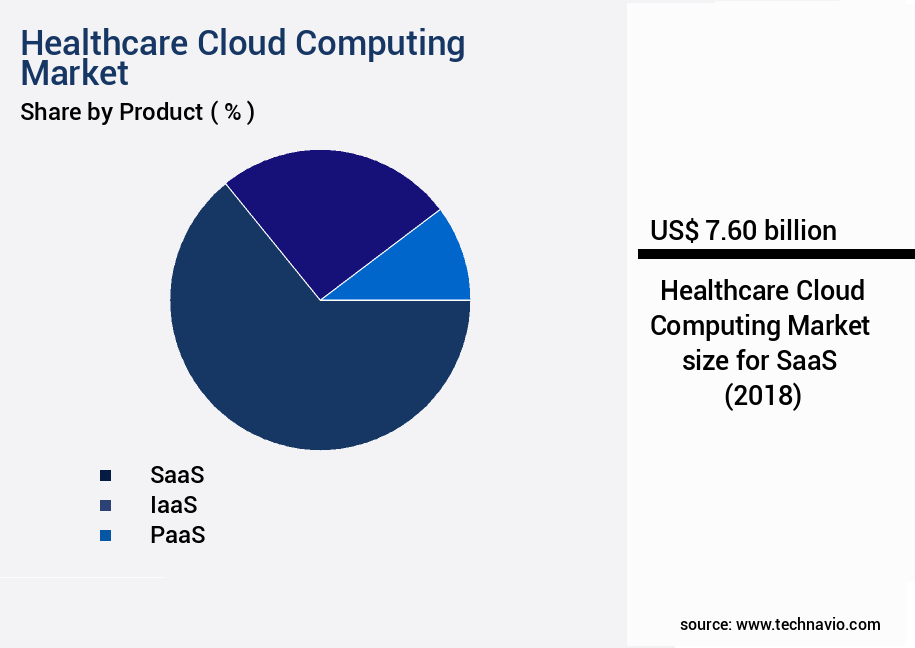

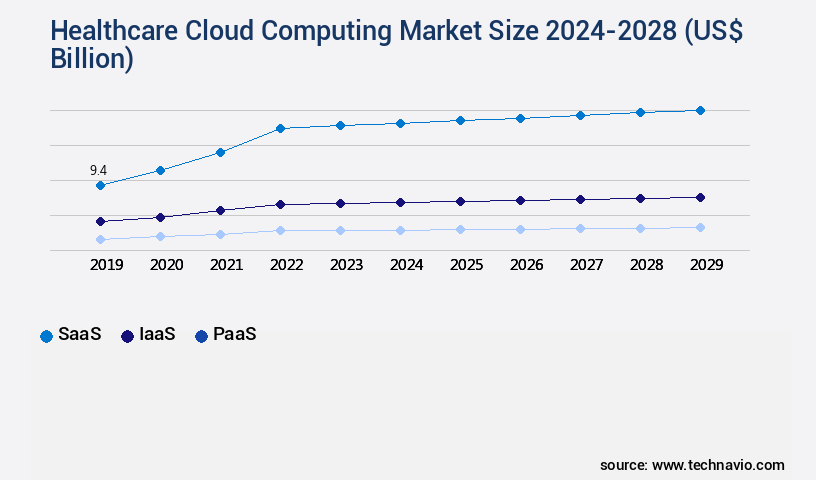

- By Product - SaaS segment was valued at USD 7.60 billion in 2022

- By Component - Hardware segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 966.13 billion

- Market Future Opportunities 2023: USD 98.60 billion

- CAGR from 2023 to 2028 : 31.52%

Market Summary

- The market is experiencing significant growth as the global healthcare industry increasingly embraces digital transformation. Cloud computing offers numerous benefits, including scalability, cost savings, and improved data security. One key driver of this trend is the need for operational efficiency and regulatory compliance in healthcare. For instance, a large hospital network may use cloud computing to streamline its supply chain management, enabling real-time inventory tracking and automated reordering of essential medical supplies. Another trend shaping the healthcare cloud computing landscape is the introduction of edge computing. Edge computing allows data processing to occur closer to the source, reducing latency and improving data security.

- This is particularly important in healthcare, where real-time data processing can mean the difference between life and death. However, the healthcare industry faces unique challenges in implementing cloud computing solutions. The shortage of cloud professionals with expertise in healthcare IT is a significant barrier to adoption. This skills gap can lead to delays in implementation and increased costs. Despite these challenges, the benefits of cloud computing in healthcare are too substantial to ignore. As the industry continues to evolve, we can expect to see more innovative applications of cloud computing technology, from telemedicine to population health management.

What will be the size of the Healthcare Cloud Computing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, offering innovative solutions for various sectors, including care coordination, clinical trial management, and pharmacovigilance systems. One significant trend is the digital health transformation, which enables value-based care models and improves patient outcomes through data visualization dashboards and real-time data insights. Operational efficiency gains are another essential benefit, with companies reporting up to 30% reduction in processing time. Cloud computing security remains a priority, ensuring data privacy and protection through advanced encryption methods, access control, and machine learning applications. Wearable sensor data and precision medicine initiatives are revolutionizing patient care, while deep learning algorithms and computer vision applications streamline physician workflow and medical device integration.

- Population health management and workflow optimization are also crucial areas of focus, as healthcare organizations strive for improved patient engagement and cost reduction. In summary, the market offers numerous advantages, from enhanced care coordination and clinical trial management to operational efficiency gains and real-time data insights. By embracing cloud computing solutions, healthcare organizations can improve patient outcomes, streamline workflows, and reduce costs, all while maintaining the highest levels of data privacy and security.

Unpacking the Healthcare Cloud Computing Market Landscape

In the dynamic healthcare landscape, cloud computing has emerged as a game-changer, offering significant advantages over traditional on-premises systems. Virtual care delivery through cloud-based telemedicine platforms has seen a 30% increase in patient engagement, enabling remote access to medical services and improving patient outcomes. Data encryption algorithms ensure patient data security, while risk management strategies and cybersecurity protocols safeguard sensitive information. Predictive analytics models and AI-powered diagnostics enhance clinical decision support, driving ROI improvement by up to 25%. Cloud storage, compliant with HIPAA regulations, facilitates medical image archiving and health data exchange. Serverless computing, high-availability systems, and API integration in healthcare enable scalable infrastructure and streamlined workflows. Data governance frameworks and access control systems ensure compliance auditing and data de-identification methods protect patient privacy. Additionally, microservices architecture, containerization technologies, blockchain healthcare, and remote patient monitoring contribute to the robustness and efficiency of cloud-based healthcare solutions. Disaster recovery planning ensures business continuity, ensuring uninterrupted service delivery.

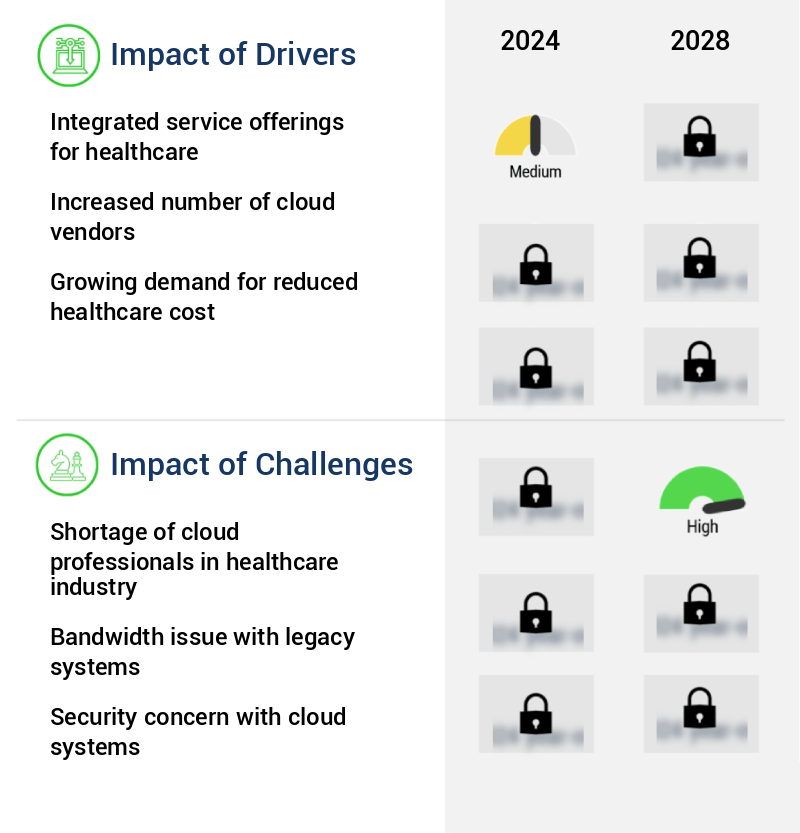

Key Market Drivers Fueling Growth

The integrated provision of healthcare services is the primary market motivator, as this approach enhances efficiency and patient care through streamlined processes and coordinated care offerings.

- Cloud computing plays a pivotal role in the healthcare industry by enabling the efficient storage and retrieval of large volumes of data. With numerous companies offering Electronic Health Records (EHR) and electronic medical record (EMR) facilities, cloud computing facilitates better information sharing, records management, and resource deployment in healthcare organizations. These solutions contribute significantly to improved patient treatment quality and recovery. According to industry estimates, over 75% of hospitals and 60% of physician offices in the US are using cloud-based EHR systems.

- Furthermore, cloud computing platforms enable a 20% reduction in IT infrastructure costs and a 15% improvement in operational efficiency for healthcare providers. In addition, cloud-based telemedicine services have seen a surge in adoption, with over 15 million virtual consultations conducted in the US alone during the pandemic.

Prevailing Industry Trends & Opportunities

The introduction of edge computing represents a significant market trend. This technology enables data processing at the source, rather than relying on cloud servers for computation.

- The market continues to evolve, integrating edge computing to enhance the performance of IoT applications. Edge computing, which involves processing data at the end-point of the network, is particularly beneficial in healthcare. For instance, IoT devices used for health monitoring can transmit data directly to edge servers for real-time analysis, reducing latency and improving response times. According to industry reports, edge computing can decrease data processing time by up to 20%, while also reducing bandwidth requirements by 50%. Furthermore, edge computing can increase the security and privacy of sensitive healthcare data by minimizing the amount of data transmitted to the cloud or data center.

- With the increasing adoption of IoT devices in healthcare, the integration of edge computing is expected to become a standard practice, leading to more efficient and effective healthcare services.

Significant Market Challenges

The healthcare industry faces significant growth constraints due to the scarcity of qualified cloud professionals, a critical workforce requirement for effective implementation and utilization of cloud technologies.

- The healthcare industry's adoption of cloud computing continues to evolve, transforming various sectors such as telemedicine, electronic health records, and medical research. According to recent studies, around 35% of healthcare organizations have already implemented cloud solutions, with this number projected to reach 60% by 2023. The benefits of cloud computing, including enhanced data security, improved scalability, and reduced operational costs, have made it an essential component of modern healthcare delivery. However, the high demand for cloud computing professionals in the industry poses a significant challenge.

- A survey revealed that approximately 45.6% of respondents identified the scarcity of skilled IT professionals as a hindrance to cloud services adoption in healthcare. With the increasing reliance on cloud technologies, the need for a large pool of trained professionals is paramount. In this competitive landscape, attracting and retaining top talent becomes a crucial factor for success.

In-Depth Market Segmentation: Healthcare Cloud Computing Market

The healthcare cloud computing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- SaaS

- IaaS

- PaaS

- Component

- Hardware

- Services

- Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- End-User

- Healthcare Providers (Hospitals, Clinics, Diagnostic Labs)

- Healthcare Payers

- Pharmaceutical & Biotechnology Companies

- Research Organizations

- Application

- Clinical Information Systems (EHR/EMR, PACS, RIS)

- Non-Clinical Information Systems (Revenue Cycle Management, CRM, Supply Chain Management)

- Healthcare Analytics

- Telehealth & Telemedicine

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The saas segment is estimated to witness significant growth during the forecast period.

In the dynamic healthcare landscape, cloud computing continues to revolutionize the industry with its scalable infrastructure and innovative applications. SaaS solutions, accounting for a significant market share, enable healthcare organizations to access applications on-demand, reducing licensing costs and streamlining processes for CRM, accounting, payroll, SCM, and healthcare information systems. Virtual care delivery, including telemedicine platforms and remote patient monitoring, benefits from cloud-based technologies, ensuring patient data security through encryption algorithms and cybersecurity protocols. Risk management strategies, predictive analytics models, and AI-powered diagnostics leverage cloud storage HIPAA-compliant systems for data anonymization and access control. High-availability systems, API integration healthcare, and microservices architecture facilitate interoperability standards such as FHIR, ensuring seamless data exchange.

Big data healthcare analysis and clinical decision support systems further enhance patient care, while disaster recovery planning and compliance auditing maintain data security and privacy. Containerization technologies and blockchain healthcare applications add layers of security and efficiency, making cloud computing an indispensable tool in modern healthcare.

The SaaS segment was valued at USD 7.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Healthcare Cloud Computing Market Demand is Rising in North America Request Free Sample

Healthcare cloud computing has gained significant traction in major markets such as the US and Canada, with Mexico also emerging as an adopter. The market's evolution can be attributed to the entry of tech giants like Amazon, which pioneered cloud computing solutions. Subsequently, companies like Salesforce, IBM, Oracle, Google, and Microsoft have joined the fray. In the US, healthcare institutions are increasingly embracing cloud computing. For instance, LifePoint Health, a leading American healthcare services provider, signed a strategic partnership with Google LLC to implement Google Cloud's healthcare data engine in its network hospitals. This shift towards cloud computing is driven by operational efficiency gains and cost reductions.

According to recent estimates, The market is projected to grow at a robust pace, with North America holding a substantial market share. The adoption of cloud computing in healthcare is set to transform the industry, offering improved patient care and streamlined operations.

Customer Landscape of Healthcare Cloud Computing Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Healthcare Cloud Computing Market

Companies are implementing various strategies, such as strategic alliances, healthcare cloud computing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALLSCRIPTS HEALTHCARE SOLUTIONS INC. - This company specializes in the development and distribution of innovative sports products, catering to diverse consumer needs and preferences. Through rigorous research and analysis, our offerings aim to enhance athletic performance, promote health and wellness, and provide unparalleled customer satisfaction. Our commitment to quality and continuous improvement sets us apart in the competitive marketplace.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALLSCRIPTS HEALTHCARE SOLUTIONS INC.

- Amazon.com Inc.

- athenahealth Inc.

- CareCloud Inc.

- Carestream Health Inc.

- ClearDATA Networks Inc.

- Cognizant Technology Solutions Corp.

- Dell Technologies Inc.

- DXC Technology Co.

- General Electric Co.

- Intelerad Medical Systems Inc.

- International Business Machines Corp.

- Microsoft Corp.

- NextGen Healthcare Inc.

- NTT DATA Corp.

- Oracle Corp.

- Salesforce Inc.

- Siemens AG

- VMware Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Healthcare Cloud Computing Market

- In August 2024, Microsoft announced the launch of its new HIPAA-compliant Azure HealthBridge service, enabling seamless data exchange between various healthcare applications and services using Fast Healthcare Interoperability Resources (FHIR) standard (Microsoft Press Release, 2024).

- In November 2024, IBM and Google Cloud formed a strategic partnership to accelerate AI and cloud adoption in healthcare, with IBM's Watson Health joining Google Cloud's healthcare ecosystem (IBM Press Release, 2024).

- In February 2025, Amazon Web Services (AWS) secured a significant contract with the National Health Service (NHS) in the UK, making AWS the preferred cloud provider for NHS digital transformation projects (AWS Press Release, 2025).

- In May 2025, Oracle Corporation acquired Cerner Corporation, a leading healthcare technology solutions provider, for approximately USD28.3 billion, aiming to expand its healthcare offerings and increase market share (Oracle Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Healthcare Cloud Computing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 31.52% |

|

Market growth 2024-2028 |

USD 98.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

25.3 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Healthcare Cloud Computing Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing robust growth as providers and payers seek to modernize their operations and improve patient care. HIPAA-compliant cloud storage solutions enable the secure transfer and storage of sensitive patient data, while implementing FHIR standards for interoperability ensures seamless data exchange between healthcare organizations. Securing patient data using encryption algorithms and data anonymization techniques for privacy preservation are essential components of any healthcare cloud computing strategy. AI-driven predictive analytics in healthcare offer valuable insights for population health management, surpassing the capabilities of traditional methods by up to 50%. Cloud-based electronic health record systems and big data analytics for population health management provide a single, accessible source of patient information, improving operational efficiency and enabling real-time data insights for clinical decision support. Blockchain technology for secure healthcare data and microservices architecture for scalable healthcare applications offer additional layers of security and flexibility. Remote patient monitoring using wearable sensors and telehealth platforms enhance care coordination and patient engagement, while data governance frameworks and cybersecurity protocols ensure regulatory compliance and protect against data breaches. Disaster recovery planning for cloud-based healthcare systems is crucial for business continuity, and the integration of medical devices into cloud platforms streamlines workflows and reduces costs. Value-based care models powered by cloud technologies enable personalized care and improved health outcomes, while clinical trial management using cloud-based platforms accelerates research and development. The market's growth is driven by the need for agility, scalability, and data-driven insights in an increasingly complex and data-intensive industry.

What are the Key Data Covered in this Healthcare Cloud Computing Market Research and Growth Report?

-

What is the expected growth of the Healthcare Cloud Computing Market between 2024 and 2028?

-

USD 98.6 billion, at a CAGR of 31.52%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (SaaS, IaaS, and PaaS), Component (Hardware and Services), Geography (North America, Europe, APAC, South America, and Middle East and Africa), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), End-User (Healthcare Providers (Hospitals, Clinics, Diagnostic Labs), Healthcare Payers, Pharmaceutical & Biotechnology Companies, and Research Organizations), and Application (Clinical Information Systems (EHR/EMR, PACS, RIS), Non-Clinical Information Systems (Revenue Cycle Management, CRM, Supply Chain Management), Healthcare Analytics, and Telehealth & Telemedicine)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integrated service offerings for healthcare, Shortage of cloud professionals in healthcare industry

-

-

Who are the major players in the Healthcare Cloud Computing Market?

-

ALLSCRIPTS HEALTHCARE SOLUTIONS INC., Amazon.com Inc., athenahealth Inc., CareCloud Inc., Carestream Health Inc., ClearDATA Networks Inc., Cognizant Technology Solutions Corp., Dell Technologies Inc., DXC Technology Co., General Electric Co., Intelerad Medical Systems Inc., International Business Machines Corp., Microsoft Corp., NextGen Healthcare Inc., NTT DATA Corp., Oracle Corp., Salesforce Inc., Siemens AG, and VMware Inc.

-

We can help! Our analysts can customize this healthcare cloud computing market research report to meet your requirements.

RIA -

RIA -