Learning Management Systems For Higher Education Market Size 2024-2028

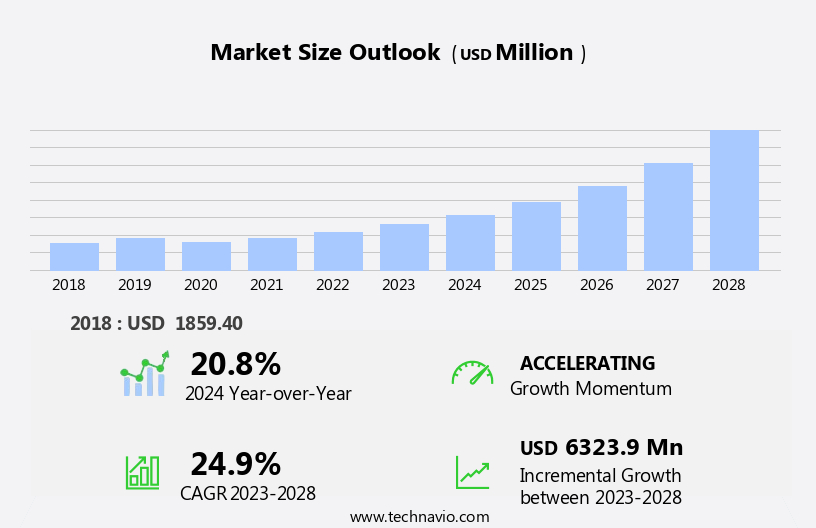

The learning management systems for higher education market size is forecast to increase by USD 6.32 billion at a CAGR of 24.9% between 2023 and 2028.

- The Learning Management Systems (LMS) market for higher education is experiencing significant growth, driven by the increasing demand for centralized and efficient learning solutions. A key trend in this market is the rising popularity of cloud-based LMS, which offers greater flexibility, scalability, and cost savings for educational institutions. Additionally, the increasing number of open-source LMS options is providing more choices for institutions, particularly those with limited budgets. However, this market is not without its challenges. Integration with other educational technologies, ensuring data security, and providing a user-friendly interface are critical considerations for LMS companies seeking to capitalize on market opportunities.

- Institutions must also navigate the complexities of implementing and integrating LMS solutions into their existing infrastructure. To succeed in this market, companies must prioritize user experience, data security, and seamless integration with other educational technologies. By addressing these challenges and leveraging the benefits of cloud-based and open-source solutions, players in the LMS market for higher education can effectively meet the evolving needs of educational institutions and learners alike.

What will be the Size of the Learning Management Systems For Higher Education Market during the forecast period?

- The higher education market for Learning Management Systems (LMS) has experienced significant growth due to the increasing demand for flexible and technology-driven learning solutions. LMS platforms have become essential tools for delivering training courses and programs, enabling institutions to provide personalized learning experiences for students. Advanced technologies such as Artificial Intelligence (AI) and Machine Learning (ML) are being integrated into LMS solutions to enhance the learning experience and improve student engagement. The corporate sector is a major contributor to this market, investing in LMS platforms to train employees and ensure industry compliance. Mobile learning and e-learning services have gained popularity, with communication devices becoming an integral part of the learning process.

- Open online courses and electronic learning have also emerged as business trends, offering cost-effective and accessible education options. The LMS market is expected to continue growing, driven by the increasing adoption of digital technology and the need for flexible and efficient learning solutions. The integration of AI and ML is expected to further revolutionize the learning experience, providing students with personalized and interactive learning experiences. Overall, LMS platforms have become essential tools for delivering high-quality education and training programs in the modern digital age.

How is this Learning Management Systems For Higher Education Industry segmented?

The learning management systems for higher education industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

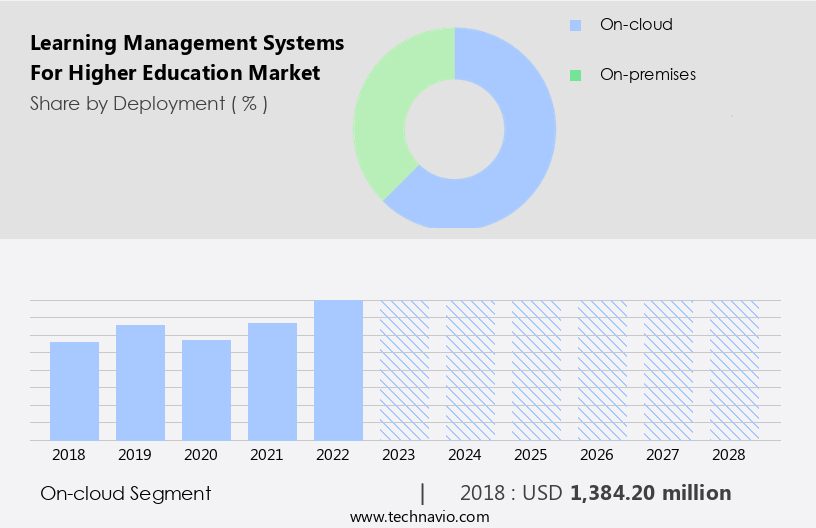

- Deployment

- On-cloud

- On-premises

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

By Deployment Insights

The on-cloud segment is estimated to witness significant growth during the forecast period.

The higher education market for Learning Management Systems (LMS) is experiencing significant growth, particularly in the on-cloud segment. This expansion is attributed to the increased accessibility and affordability of cloud-based LMS solutions. Cloud-based LMS platforms offer flexible pricing models, including pay-per-user and pay-per-use, enabling institutions to choose the most cost-effective option. Traditional LMS companies are adopting penetration pricing strategies to compete, making these solutions more accessible to educational institutions in tier 2 and tier 3 cities. Advanced technologies, such as AI and ML, are enhancing learner experiences and engagement insights. Mobile learning solutions and digital content, including eBooks, multimedia resources, and training courses, are also driving the market's growth.

Despite budget constraints, economic conditions, and digital learning initiatives, LMS platforms are essential for workforce development, talent development, and lifelong learning. Cultural barriers, international students, and the ICT sector's infrastructure also influence the market's growth. The market's future potential lies in the integration of 5G technology, adaptive learning, and blended learning approaches.

Get a glance at the market report of share of various segments Request Free Sample

The On-cloud segment was valued at USD 1.38 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

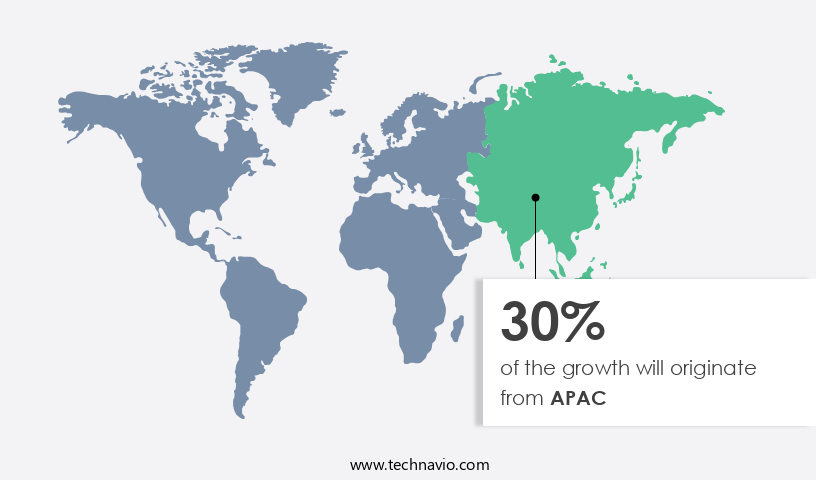

APAC is estimated to contribute 30% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The North American learning management systems (LMS) market is projected to experience consistent growth due to the increasing demand from corporate organizations. Centralized learning offered by LMS solutions has driven the adoption of these systems in Small and Medium-sized Enterprises (SMBs), particularly in the US, Canada, and Mexico. Moreover, the need for effective and high-quality education in developed economies is fueling market growth. Advanced technologies, such as AI and ML, are enhancing learning experiences, enabling adaptive learning and personalized development strategies. LMS platforms offer cloud-based and on-premises solutions, catering to various user types, including corporate users, millennials, and Gen Z.

Mobile learning solutions and multichannel learning are addressing the needs of a mobile workforce. LMS platforms provide digital content, training courses, and programs, enabling workforce development and talent development. Budget constraints and economic conditions are driving the adoption of cost-effective online learning solutions. Infrastructure advancements and the increasing use of communication devices, such as smartphones, laptops, and tablets, are also contributing to market growth. Cultural barriers and the presence of international students in educational institutions and businesses further expand the market scope.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Learning Management Systems For Higher Education Industry?

- Facilitates centralized learning is the key driver of the market.

- LMS software serves as a centralized learning solution for higher education institutions and businesses, delivering diverse learning content to learners. Advanced LMS enables educators to curate content from an extensive pool of online and offline resources, catering to the evolving needs of students in various professional programs, such as data analysis, digital marketing, and bookkeeping. This adaptability has significantly boosted the demand for LMS in the higher education sector. With the aid of advanced LMS, educators can assess user-generated content available online and select relevant material to refine and formalize for distribution.

- This process enhances the overall learning experience and keeps the content up-to-date with industry trends. The integration of technology in education has become increasingly crucial, making LMS an indispensable tool for educators and learners alike.

What are the market trends shaping the Learning Management Systems For Higher Education Industry?

- Rising popularity of cloud-based LMS is the upcoming market trend.

- The shift towards cloud-based Learning Management Systems (LMS) in higher education has gained significant momentum. Traditional LMS providers are transitioning to cloud-based solutions, which are generally hosted on the provider's servers and eliminate the need for on-premise servers. Subscription-based purchasing and low implementation costs are key advantages of cloud-based LMS. Unlike traditional LMS, cloud-based solutions do not require extensive installation processes or dedicated human resources.

- Moreover, cloud-based e-learning can be set up quickly and deployed with minimal time investment. These factors contribute to the increasing popularity of cloud-based LMS in the higher education sector.

What challenges does the Learning Management Systems For Higher Education Industry face during its growth?

- Increase in number of open-source LMS is a key challenge affecting the industry growth.

- The higher education sector's learning management systems (LMS) market has experienced significant growth in open-source LMS solutions. Open-source LMS has gained popularity over traditional LMS due to its adoption in academic institutions, particularly in higher education. The market expansion is attributed to the increasing number of LMS providers offering open-source platforms for end-users. For example, Sakai provides an LMS for educational institutions, featuring tools such as online testing and seamless integration with Google Docs.

- Moodle, another open-source LMS, is a widely-used option in the market. The influx of open-source LMS solutions has intensified competition within the industry. Despite this, the market continues to grow, offering institutions flexibility, cost-effectiveness, and customizable features.

Exclusive Customer Landscape

The learning management systems for higher education market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the learning management systems for higher education market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, learning management systems for higher education market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

360Learning SA - The company specializes in implementing and supporting advanced learning management solutions, including Blackboard Learn and Learning Management Systems. These systems facilitate the delivery, tracking, and management of educational content and student progress, enhancing the overall learning experience. By leveraging innovative technology and customizable features, our clients can effectively engage learners, streamline administrative tasks, and improve educational outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 360Learning SA

- Adrenalin eSystems Ltd.

- Anthology Inc.

- Cornerstone OnDemand Inc.

- D2L Inc.

- Degreed Inc.

- Docebo Inc.

- Epignosis LLC

- Instructure Holdings Inc.

- Koch Industries Inc.

- Oracle Corp.

- Pearson Plc

- PowerSchool Holdings Inc.

- SAP SE

- Skillsoft Corp.

- Sprout On Web Pty. Ltd.

- Tovuti Inc.

- Violet InfoSystems Pvt. Ltd.

- Workday Inc.

- Xperiencify

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Learning Management Systems (LMS) in Higher Education: Driving Workforce Development and Digital Transformation Learning Management Systems (LMS) have emerged as a crucial tool for educational institutions and corporations in the higher education market. These platforms enable the delivery, management, and tracking of training programs, providing advanced technologies to enhance learning experiences and administrative tasks. In today's dynamic business environment, LMS solutions play a pivotal role in workforce development, helping organizations adapt to economic conditions and industry regulations. Advanced technologies, such as artificial intelligence (AI) and machine learning (ML), are increasingly being integrated into LMS platforms to deliver personalized learning experiences and engagement insights.

LMS platforms cater to various user types, including corporate users, millennials, and Gen Z. They offer a multichannel learning approach, enabling access through smartphones, laptops, tablets, and USB drives, ensuring learning is accessible anytime, anywhere. Budget constraints and the need for scalability have led to the adoption of cloud-based LMS platforms. These platforms offer cost savings, flexibility, and ease of deployment, making them an attractive option for businesses and educational institutions. Digital learning initiatives have gained momentum in recent years, driven by the need for reskilling programs and lifelong learning. LMS platforms provide a centralized location for managing and delivering digital content, including multimedia resources and e-books.

However, the implementation of LMS solutions is not without challenges. Cultural barriers, such as resistance to change and the need for multilingual capabilities, can hinder adoption, particularly among international students and organizations operating in linguistically diverse environments. The ICT sector plays a crucial role in the infrastructure required to support LMS platforms. 5G technology and other digital technologies are essential for delivering high-quality learning experiences, particularly for large enterprises and educational institutions with extensive workforces. LMS platforms offer a range of capabilities, from blended learning and face-to-face instruction to online learning activities and instructor-led training. They provide valuable ROI metrics, enabling organizations to measure the impact of their training programs on learner performance and workforce development.

In , LMS solutions have become essential tools for driving workforce development and digital transformation in the higher education market. By providing advanced technologies, flexible deployment options, and scalable solutions, LMS platforms enable organizations to adapt to economic conditions, industry regulations, and the evolving needs of their workforce.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24.9% |

|

Market growth 2024-2028 |

USD 6323.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

20.8 |

|

Key countries |

US, China, UK, Germany, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Learning Management Systems For Higher Education Market Research and Growth Report?

- CAGR of the Learning Management Systems For Higher Education industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the learning management systems for higher education market growth of industry companies

We can help! Our analysts can customize this learning management systems for higher education market research report to meet your requirements.

RIA -

RIA -