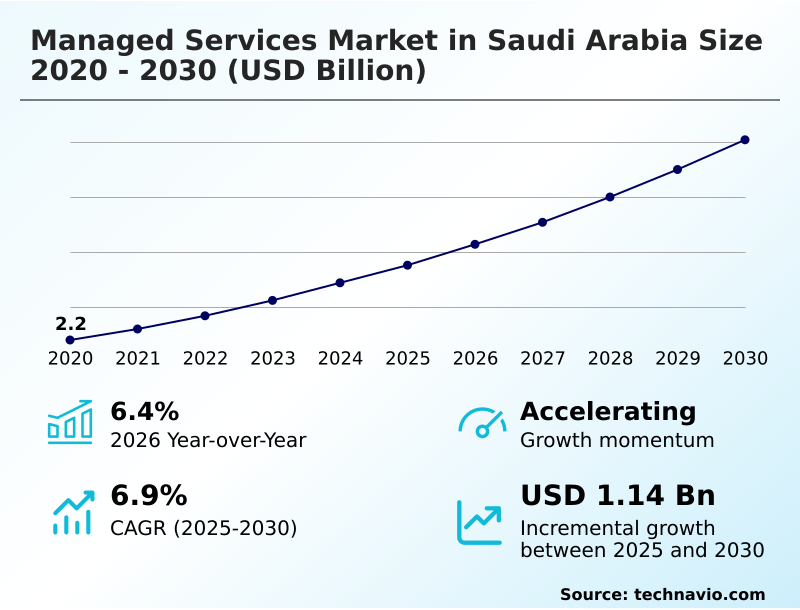

Saudi Arabia Managed Services Market Size 2026-2030

The saudi arabia managed services market size is valued to increase by USD 1.14 billion, at a CAGR of 6.9% from 2025 to 2030. Growing digital transformation initiatives across Saudi enterprises will drive the saudi arabia managed services market.

Major Market Trends & Insights

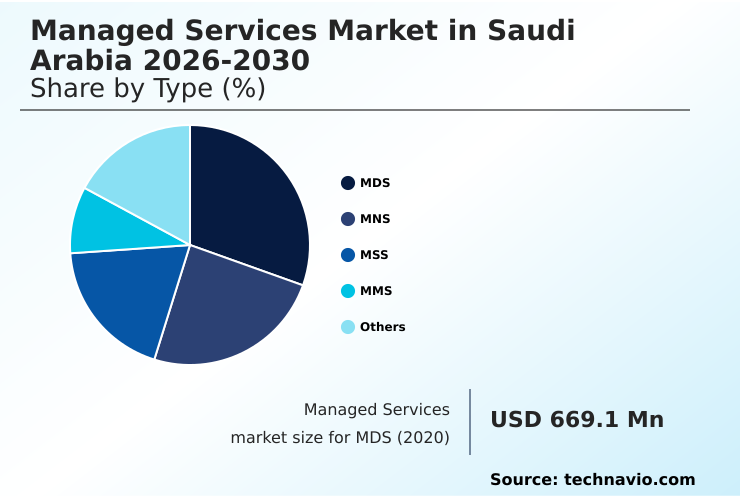

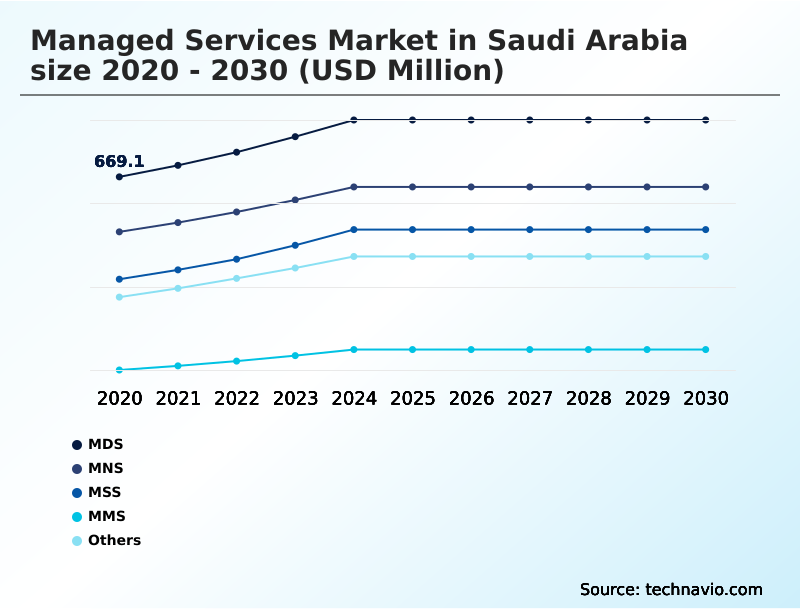

- By Type - MDS segment was valued at USD 807.9 million in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.82 billion

- Market Future Opportunities: USD 1.14 billion

- CAGR from 2025 to 2030 : 6.9%

Market Summary

- The managed services market in saudi arabia is undergoing a significant evolution, moving from traditional break-fix support to proactive, strategic partnerships. This shift is driven by the increasing complexity of IT ecosystems, where organizations leverage managed services to navigate hybrid cloud environments, implement zero-trust architectures, and ensure compliance with stringent data sovereignty regulations.

- Providers offer a spectrum of solutions, including infrastructure management, managed detection and response, and automated infrastructure optimization, which are critical for maintaining operational resilience.

- For instance, a retail enterprise might outsource its IT operations to a provider that ensures the security of its real-time payment platforms and uses predictive analytics to manage digital supply chains, thereby improving both security and efficiency.

- This model allows businesses to focus on core competencies while accessing specialized skills and advanced technologies like intelligent automation, which is essential for achieving the goals of national digital transformation programs. As a result, outcome-based contracts are becoming more prevalent than fixed-fee arrangements, reflecting a mature market that values measurable business outcomes and technological agility.

What will be the Size of the Saudi Arabia Managed Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Saudi Arabia Managed Services Market Segmented?

The saudi arabia managed services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- MDS

- MNS

- MSS

- MMS

- Others

- Deployment

- Cloud

- On premises

- End-user

- Government

- Financial services

- Healthcare

- Oil and gas

- Others

- Geography

- Middle East and Africa

- Saudi Arabia

- Middle East and Africa

By Type Insights

The mds segment is estimated to witness significant growth during the forecast period.

The managed data services segment is foundational to the managed services market in saudi arabia 2026-2030, facilitating data governance and lifecycle management for enterprises.

As organizations shift toward a technology driven economic structure, outsourcing data operations allows for the use of advanced enterprise analytics and high-performance computing.

This is supported by a burgeoning ecosystem of international hyperscalers establishing local regions to meet strict data sovereignty regulations. This strategic outsourcing enables secure and efficient scaling of digital operations.

The adoption of a robust data governance framework and identity and access management protocols ensures compliance, with early adopters reporting up to a 25% improvement in data processing efficiency.

This reliance on specialized third party service providers for information management services is critical for digital transformation initiatives, especially in data-intensive sectors pursuing operational agility.

The MDS segment was valued at USD 807.9 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises evaluating the managed services market in saudi arabia 2026-2030 are increasingly conducting detailed cost-benefit analyses, with the managed services vs in-house it cost debate being a central theme. The primary goal is reducing it operational costs with msp engagement while scaling business with managed services.

- A crucial part of this evaluation involves a managed security services provider comparison to ensure robust protection. As cloud adoption accelerates, understanding cloud managed services pricing models becomes essential for financial planning. The importance of data sovereignty in cloud environments is a key consideration, compelling businesses to seek partners that guarantee data residency.

- Operationally, proactive it monitoring and maintenance is a key value proposition, as firms using this approach report up to 30% fewer critical incidents than those with reactive support models. The benefits of managed services for smes are particularly notable, providing access to enterprise-grade tools.

- Industry-specific needs are addressed through tailored solutions, with high demand for managed services for financial industry and managed it services for healthcare sector. The government sector managed services adoption is also strong, alongside specialized offerings for the telecommunications managed services outsourcing, retail industry managed services benefits, and manufacturing sector it managed services.

- For heavy industries, managed services for oil and gas are critical for operational safety and efficiency. Ultimately, the focus is on a holistic strategy encompassing disaster recovery and business continuity, ensuring the managed services impact on uptime is positive and measurable through superior it infrastructure management best practices for managed services for hybrid cloud.

What are the key market drivers leading to the rise in the adoption of Saudi Arabia Managed Services Industry?

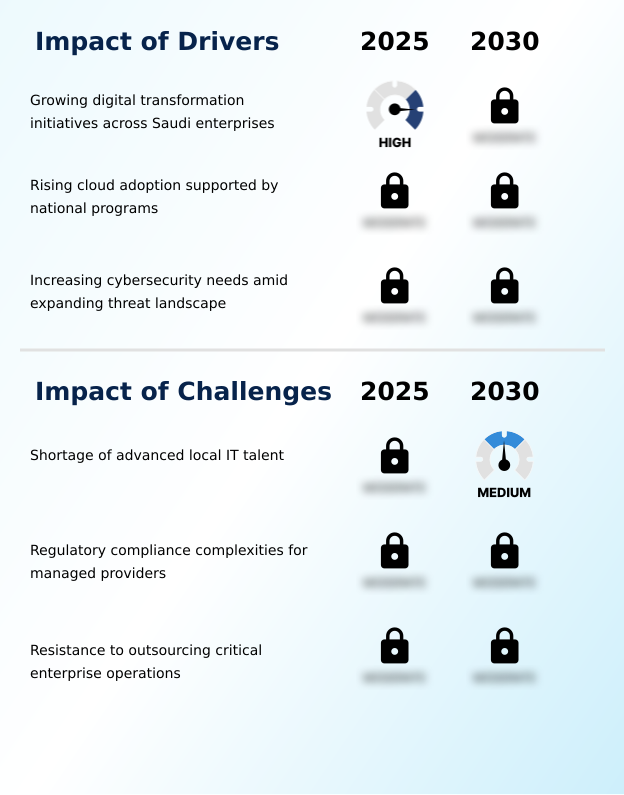

- The market's growth is primarily driven by widespread digital transformation initiatives across enterprises in Saudi Arabia.

- The market's momentum is primarily fueled by national digital transformation programs that compel enterprises to modernize operations. Organizations are shifting to automated, data-informed environments, increasing their reliance on providers for scalable round the clock assistance.

- The adoption of advanced tools for remote asset monitoring and data driven asset management accelerates project delivery by 30%. This technology driven economic structure supports large-scale IT investments and long-term partnerships.

- The push for a national data center strategy further stimulates demand for managed infrastructure capabilities.

- As enterprises prioritize higher operational agility and reduced administrative burden, they turn to providers for managed backup and recovery services, which helps reduce operational overhead by 20% and ensures that newly deployed technologies perform optimally while maintaining security and compliance.

What are the market trends shaping the Saudi Arabia Managed Services Industry?

- A notable market trend is the rising demand for industry-specific managed solutions. This shift reflects a growing need for specialized expertise aligned with vertical-specific regulatory and operational requirements.

- A significant trend shaping the market is the move toward highly specialized, verticalized service offerings. As organizations pursue digital transformation initiatives, generic outsourcing is being replaced by industry-specific solutions that address unique workflow and regulatory compliance pressures. This is particularly evident in sectors where data sensitivity is high, leading to partnerships that provide contextual security and cloud management.

- The adoption of proactive analytics and mobile device management within these specialized services helps reduce downtime by up to 30%. This focus on industry alignment enhances cross industry adoption of advanced platforms.

- Service providers that offer deep domain expertise in areas like managed security are gaining a competitive edge, as enterprises now demand a service level agreement that guarantees outcomes tied to specific business objectives, improving compliance adherence by 25%.

What challenges does the Saudi Arabia Managed Services Industry face during its growth?

- A key challenge affecting industry growth is the persistent shortage of advanced local IT talent required to support rapid technological adoption.

- The primary challenge for the market is the acute shortage of advanced local IT talent, which struggles to keep pace with rapid technological change. This gap in specialized skills for cloud architecture, security operations, and AI-driven automation forces managed service providers to compete for a limited pool of professionals, increasing recruitment costs by over 35%.

- The push for digital sovereignty and data residency requirements further strains recruitment by mandating local capability building. This talent shortage can lead to project delays averaging 15%, impacting service quality and limiting the complexity of offerings like managed print services.

- Addressing this issue requires long-term collaboration to build a sustainable and qualified workforce capable of handling mission critical enterprise environments and supporting the expanding managed services landscape.

Exclusive Technavio Analysis on Customer Landscape

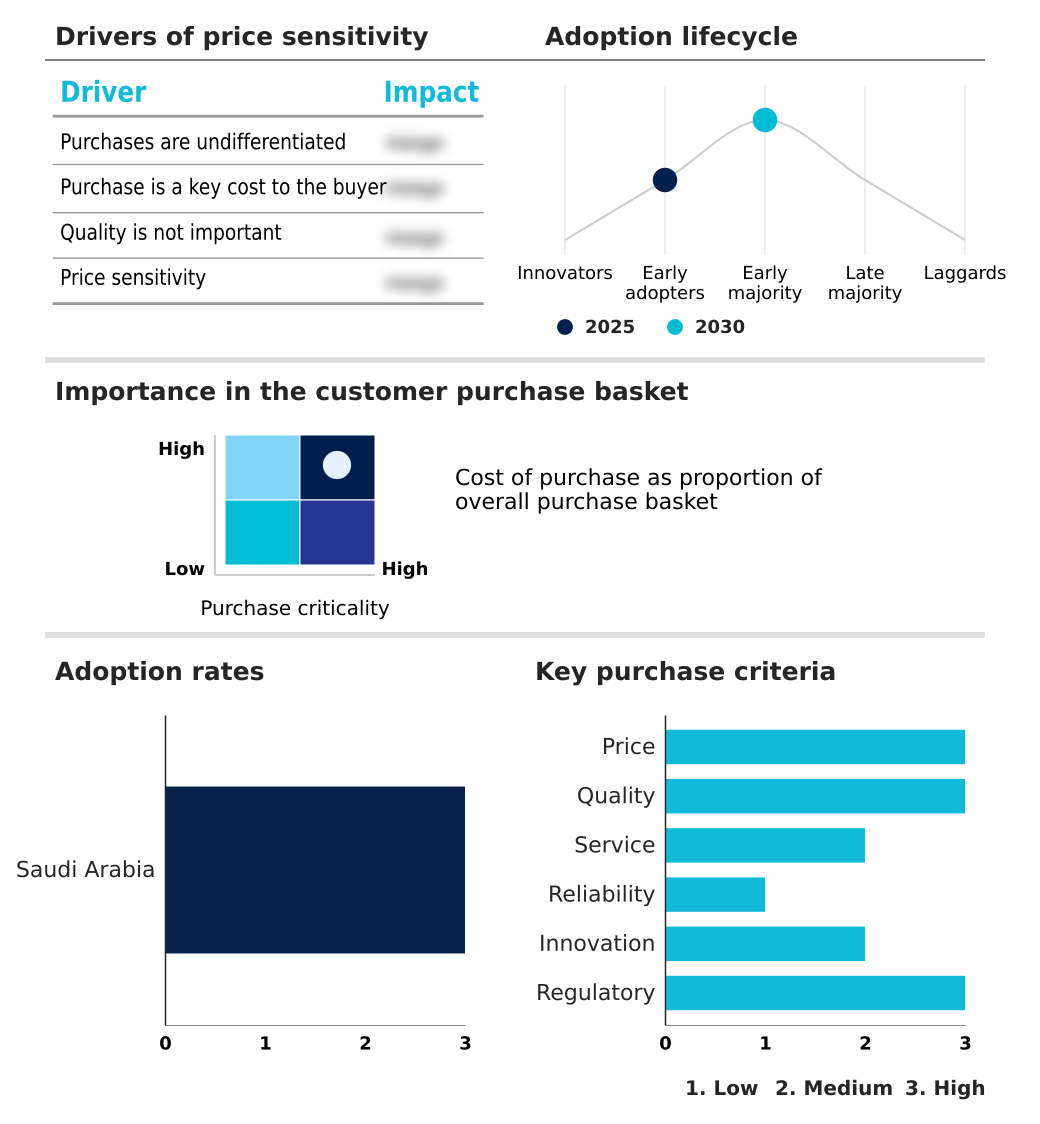

The saudi arabia managed services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the saudi arabia managed services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Saudi Arabia Managed Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, saudi arabia managed services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Provides managed IT, cloud, and infrastructure services, enabling enterprise digital transformation, operational support, and strategic modernization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- Cognizant Technology Solution

- Detecon Al Saudia Co. Ltd.

- DXC Technology Co.

- Ejada Systems Co. Ltd.

- HCL Technologies Ltd.

- IBM Corp.

- Infosys Ltd.

- Kyndryl Inc.

- LTIMindtree Ltd.

- Moammar Information Systems

- Nippon Telegraph and Corp.

- Nour Communications Co Ltd.

- Orange SA

- Saudi Business Machines

- Tata Consultancy Services

- Tech Mahindra Ltd.

- Wipro Ltd.

- Zain KSA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Saudi arabia managed services market

- In September 2025, IBM Corp. announced an expansion of its collaboration with AWS to create a Riyadh-based innovation hub focused on generative AI and secure cloud services.

- In June 2025, the Saudi Arabian government, through its Ministry of Communications and Information Technology, launched the National Data Center Strategy to advance sovereign cloud solutions.

- In March 2025, Zain KSA finalized a comprehensive cloud-based overhaul of its business support systems to bolster its managed IoT and cloud computing services.

- In February 2025, Saudi Business Machines entered into a strategic partnership with IFS to provide advanced industrial AI and cloud-based software solutions to clients.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Saudi Arabia Managed Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 198 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.9% |

| Market growth 2026-2030 | USD 1135.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.4% |

| Key countries | Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The managed services market in saudi arabia 2026-2030 is defined by a strategic shift towards proactive monitoring and intelligent automation to manage increasingly complex hybrid cloud environments. Organizations are leveraging managed services for comprehensive infrastructure management, including workload migration and it infrastructure management, to enhance performance.

- A critical boardroom consideration is adherence to data sovereignty regulations, which directly influences infrastructure investment and provider selection. The integration of zero-trust architectures and managed detection and response is now standard, driven by the need for continuous threat monitoring.

- Service providers are delivering value through automated infrastructure optimization and cloud cost optimization, with some enterprises achieving a 40% reduction in manual intervention for routine tasks. Offerings such as managed data center services, unified communications management, and managed network services are integral to digital transformation.

- This is complemented by a focus on lifecycle management, real-time payment platforms, and the adoption of cloud native solutions to ensure agility and a strong security posture.

What are the Key Data Covered in this Saudi Arabia Managed Services Market Research and Growth Report?

-

What is the expected growth of the Saudi Arabia Managed Services Market between 2026 and 2030?

-

USD 1.14 billion, at a CAGR of 6.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (MDS, MNS, MSS, MMS, and Others), Deployment (Cloud, and On premises), End-user (Government, Financial services, Healthcare, Oil and gas, and Others) and Geography (Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing digital transformation initiatives across Saudi enterprises, Shortage of advanced local IT talent

-

-

Who are the major players in the Saudi Arabia Managed Services Market?

-

Accenture Plc, Atos SE, Cognizant Technology Solution, Detecon Al Saudia Co. Ltd., DXC Technology Co., Ejada Systems Co. Ltd., HCL Technologies Ltd., IBM Corp., Infosys Ltd., Kyndryl Inc., LTIMindtree Ltd., Moammar Information Systems, Nippon Telegraph and Corp., Nour Communications Co Ltd., Orange SA, Saudi Business Machines, Tata Consultancy Services, Tech Mahindra Ltd., Wipro Ltd. and Zain KSA

-

Market Research Insights

- Market dynamics are increasingly shaped by strategic outsourcing and a focus on core business competencies. Organizations adopting this model report up to a 20% improvement in operational agility. The emphasis on local capability building is reshaping provider strategies, with investments in service innovation and client relationship management leading to customer retention gains of over 15%.

- This shift is supported by government-led digital citizen services and hybrid workplace management initiatives, which create sustained demand. The adoption of multi-company and open-source solutions is also influencing the landscape, compelling providers to offer more flexible and integrated service models.

- As a result, IT budget allocation is shifting from capital expenditure to operational expenditure, reflecting a broader acceptance of the as-a-service economy.

We can help! Our analysts can customize this saudi arabia managed services market research report to meet your requirements.

RIA -

RIA -