Video Managed Services Market Size 2024-2028

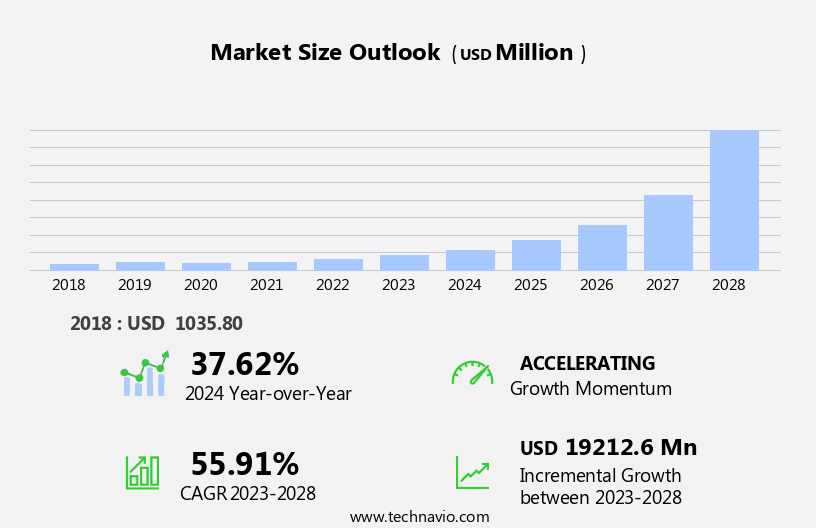

The video managed services market size is forecast to increase by USD 19.21 billion at a CAGR of 55.91% between 2023 and 2028.

What will be the Size of the Video Managed Services Market During the Forecast Period?

How is this Video Managed Services Industry segmented and which is the largest segment?

The video managed services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Enterprises

- Government

- Geography

- North America

- Canada

- US

- Europe

- Germany

- APAC

- China

- India

- South America

- Middle East and Africa

- North America

By End-user Insights

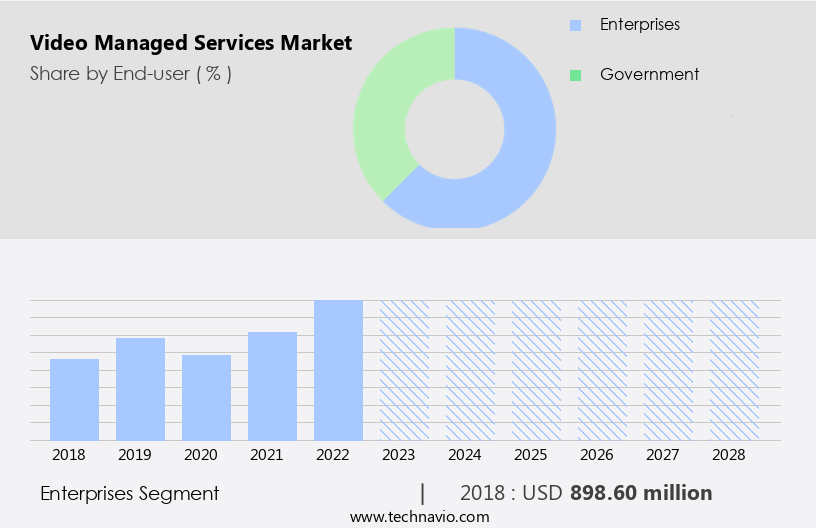

- The enterprises segment is estimated to witness significant growth during the forecast period.

The enterprise sector is expected to lead the market due to the need to manage large deployments of video conferencing systems and audio-visual meeting rooms. Businesses encounter technical challenges, including inconsistent user experiences caused by a lack of standardization and complexity in meeting rooms. Decentralized purchasing methods allow companies to design overly elaborate rooms, leading to unnecessary expenses. These issues will drive market growth as enterprises seek solutions to streamline and optimize their video conferencing infrastructure. The market encompasses various components, including software, hardware, and services, as well as cloud-based solutions, OTT platforms, and visual collaboration tools. Key verticals include large enterprises, SMEs, government organizations, educational institutions, healthcare, and manufacturing industries.

Video managed services enable productivity enhancements through applications such as telemedicine, connectivity tools, and security agencies. Additionally, video surveillance techniques and AI/ML environments are integral to the market, as are networking equipment and electronic components. ICT spending, cyber assaults, and smart city projects are significant factors influencing market trends.

Get a glance at the Video Managed Services Industry report of share of various segments Request Free Sample

The Enterprises segment was valued at USD 898.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

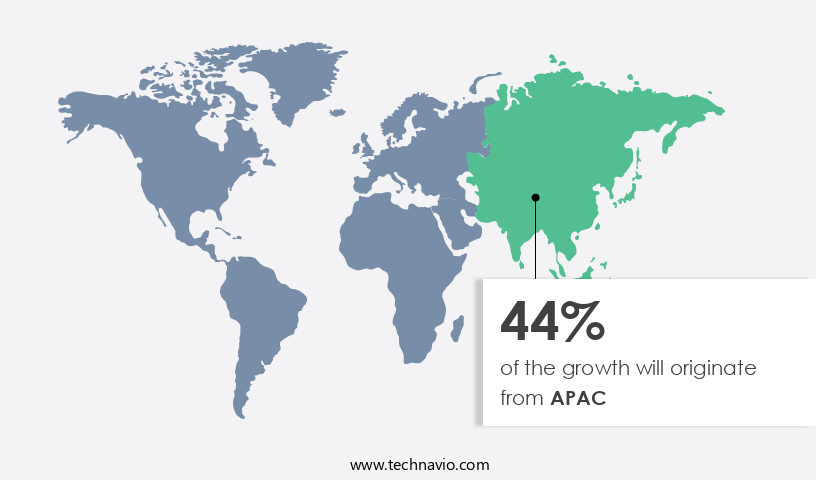

- APAC is estimated to contribute 44% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market for video managed services is thriving due to the region's advanced technology adoption in industries such as industrial, retail, and BFSI. With some of the world's most developed economies, there is a significant demand for managed services like data processing, outsourcing, and internet services. Moreover, the integration of cloud-based services, automation solutions, and AI into operational and supply chain processes is leading to the emergence of new intelligent video managed services. Compliance with government regulations, particularly in response to increasing cyberattacks on hosted servers, is another factor fueling growth in North American countries like the US and Canada.

Key components of video managed services include cloud videoconferencing, huddle room technology, visual collaboration, unified conferencing, and video surveillance techniques. The market encompasses software, hardware, business-to-business, business-to-consumer, SMEs, IT operations, big data analytics, AI/ML environments, MSPs, RMM software, PSA software, cloud-based solutions, OTT platforms, VOD, D2C OTT, electronic components, networking equipment, ICT spending, and security agencies, among others.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Video Managed Services Industry?

Need to focus on core competencies and improve efficiency is the key driver of the market.

What are the market trends shaping the Video Managed Services Industry?

Increasing automation in managed services is the upcoming market trend.

What challenges does the Video Managed Services Industry face during its growth?

System integration and interoperability issues is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The video managed services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the video managed services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, video managed services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Adtech Systems LLC - The company specializes in providing video managed services, encompassing Audio Visual and Video Endpoint management, as well as Third Party Multipoint Control Unit (MCU) management. These offerings ensure optimal performance and seamless integration of video conferencing solutions for businesses.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adtech Systems LLC

- Applied Global Technologies

- AT and T Inc.

- AVI SPL LLC

- BT Group Plc

- Cameo Global Inc.

- Cinos Ltd.

- Cisco Systems Inc.

- Gurusons Communications Pvt. Ltd.

- ideyaLabs

- Internet MegaMeeting LLC

- Macro Technologies

- Nippon Telegraph And Telephone Corp.

- Plantronics Inc.

- Premiere Global Services Inc.

- Radio Technical Services Ltd.

- Sota Solutions Ltd.

- TELUS Corp.

- Vega Technology Ltd.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of solutions designed to facilitate the effective management and delivery of video-based services. These offerings cater to various sectors, including large enterprises, government organizations, educational institutes, healthcare verticals, and others. The market is characterized by continuous innovation and growth, driven by the increasing demand for visual collaboration and communication tools. Video managed services span various applications, including cloud videoconferencing, huddle room technology, and unified conferencing. The adoption of these solutions is fueled by the need for productivity enhancement and cost savings, particularly in business-to-business (B2B) and business-to-consumer (B2C) environments. In the realm of IT operations, video managed services play a crucial role in enabling large corporations to streamline their internal processes and improve communication between teams.

The integration of big data analytics and artificial intelligence (AI) environments further enhances the functionality of these solutions, enabling advanced features such as content development cost reduction and productivity rate optimization. The market for video managed services is diverse, encompassing both software and hardware offerings. Managed service providers (MSPs) and remote monitoring software (RMM) and professional services automation (PSA) software companies are key players in this landscape, providing cloud-based solutions and over-the-top (OTT) platforms to cater to the evolving needs of their clients. The adoption of video managed services extends beyond traditional sectors and applications. For instance, In the manufacturing and retail industries, these solutions are used to optimize supply chain management and enhance customer engagement, respectively.

In the public sector, video managed services are employed in smart city projects, city surveillance networks, and security agencies to ensure public safety and maintain order. The growth of the market is underpinned by several factors, including the increasing importance of connectivity tools in various industries and the rising demand for telemedicine services in healthcare verticals. Furthermore, the integration of AI and machine learning (ML) environments in video management solutions has led to advancements in video surveillance techniques, enabling more efficient and effective security measures in various settings. Despite the numerous benefits of video managed services, challenges persist.

Cyber assaults and data breaches pose significant risks to organizations, necessitating robust security measures to protect sensitive information. Additionally, the increasing use of video managed services in various applications raises concerns regarding content development costs and the potential for misuse in public spaces, such as educational institutes and religious places. In conclusion, the market is a dynamic and evolving landscape, driven by the growing demand for visual collaboration and communication tools in various industries and applications. The integration of AI and ML environments, cloud deployment, and advanced security features are key trends shaping the future of this market. However, challenges related to data security and cost management must be addressed to ensure the continued growth and adoption of video managed services.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 55.91% |

|

Market growth 2024-2028 |

USD 19212.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

37.62 |

|

Key countries |

US, China, India, Canada, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Video Managed Services Market Research and Growth Report?

- CAGR of the Video Managed Services industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the video managed services market growth of industry companies

We can help! Our analysts can customize this video managed services market research report to meet your requirements.

RIA -

RIA -