RF Components Market for Consumer Electronics Market Size 2024-2028

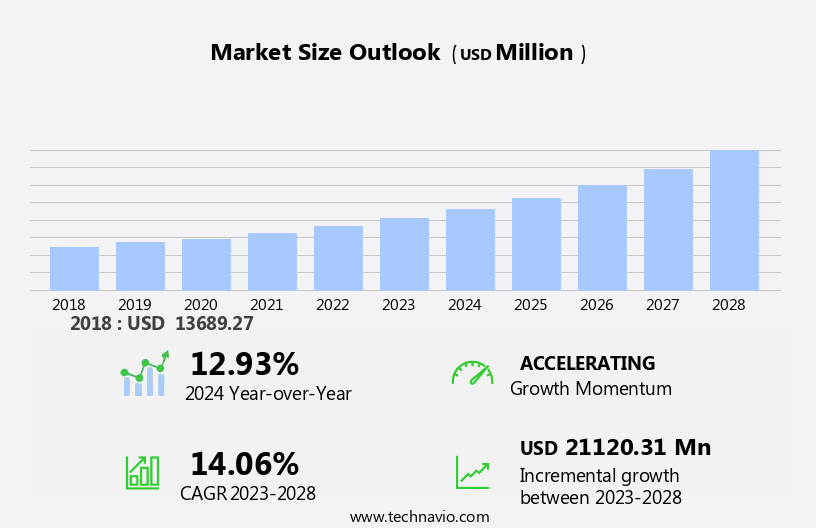

The RF components market for consumer electronics market size is forecast to increase by USD 21.12 billion at a CAGR of 14.06% between 2023 and 2028. The RF components market for consumer electronics is experiencing significant growth due to several driving factors. One of the primary factors is the increasing demand for RF technology in various consumer devices, such as laptops, tablets, and smart home accessories. Another factor is the integration of advanced technologies like artificial intelligence (AI) and voice recognition into these devices, which require strong RF transmission systems for seamless control and automation solutions. Moreover, the emergence of 5G technology is fueling the growth of the market, as it offers faster connectivity features and improved baseband signals for various applications, including music systems, location trackers, navigation systems, and central locking systems. However, challenges such as RF interference and spectrum congestion remain concerns for market participants. Additionally, the RF components market is witnessing significant growth in the automotive sector, where RF technology is being used for automation solutions, voice recognition systems, and connectivity features in vehicles. Overall, the market is expected to continue its growth trajectory, driven by these trends and challenges.

What will be the Size of the Market During the Forecast Period?

The RF components market plays a crucial role in the consumer electronics industry, enabling wireless connectivity and advanced functionality in various devices. This market is driven by the increasing demand for mobile handsets, IoT solutions, and smart devices. RF technology, including LTE-advanced, Bluetooth, and Wi-Fi technology, is essential for wireless connectivity in consumer electronics. RF engineering and spectrum management are key considerations in designing and manufacturing these components. The consumer electronics landscape is diverse, encompassing cellular phones, smartphones, IoT applications, home robots, smart wearables, and more. Each application zone has unique requirements in terms of RF components and engineering.

For instance, cellular phones necessitate high-performance RF components to ensure strong wireless connectivity and support for 4G and other advanced cellular technologies. In contrast, IoT applications require low-power ICs and optimized RF design to extend battery life and minimize power consumption. Security level requirements and regulatory considerations are essential factors influencing the RF components market for consumer electronics. With the growing importance of wireless connectivity in various applications, ensuring secure wireless communication and adhering to regulatory standards becomes increasingly critical. Moreover, the military sector also relies on RF technology for electronic warfare and communication systems. However, the focus of this analysis is on the consumer electronics market.

Moreover, RF components are integral to semiconductor technology, which is the backbone of modern electronics. As the demand for wireless connectivity and advanced functionality continues to grow, the RF components market is expected to expand, offering significant opportunities for innovation and growth. In conclusion, the RF components market for consumer electronics is a dynamic and evolving landscape, driven by the increasing demand for wireless connectivity and advanced functionality in various applications. RF engineering and spectrum management are essential considerations in designing and manufacturing RF components for consumer electronics. Security level requirements and regulatory considerations also play a crucial role in shaping the market. The future of RF components in consumer electronics is promising, with opportunities for innovation and growth in various application zones.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Digital components

- Analog components

- Mixed signal components

- Others

- Deployment

- Power amplifier

- Antenna

- Switches

- Multiplexer

- Others

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

By Technology Insights

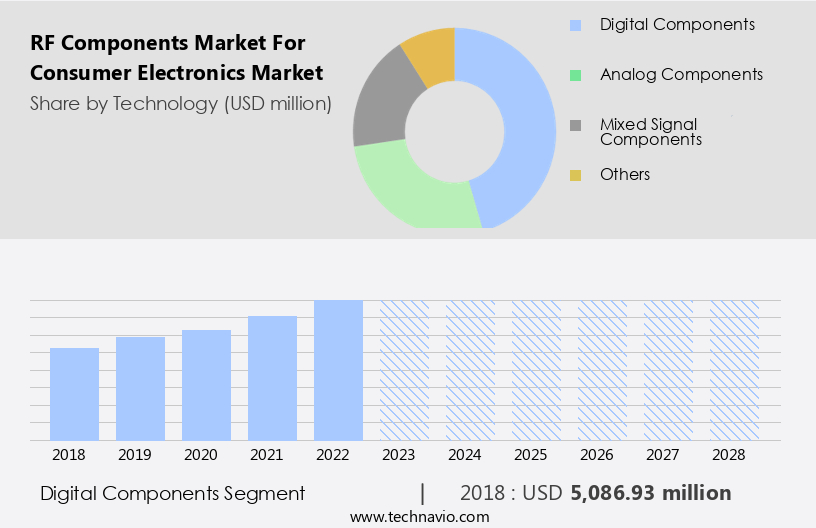

The digital components segment is estimated to witness significant growth during the forecast period.RF components play a crucial role in the consumer electronics industry, particularly in applications such as wireless communication, automotive consumer electronics, and Electronic Warfare Technology. Components, including duplexers, RF amplifiers, RF switches, modulators and demodulators, mixers, and synthesizers, are essential for enabling wireless connectivity in devices such as cellular phones, radios, Bluetooth, and Wi-Fi technology. The advancements in RF technology have led to the development of more sophisticated RF components, such as digital RF components. Digital RF components, including digital signal processors (DSPs), digital-to-analog converters (DACs), analog-to-digital converters (ADCs), and digital frequency synthesizers, are increasingly being adopted due to their small form factors, low power consumption, and high integration capabilities.

Moreover, the proliferation of the Internet of Things (IoT) and the growing demand for smart sensors and connected systems have fueled the need for digital RF components. These components enable efficient wireless connectivity, data acquisition, and sensor interfacing in various IoT applications, such as smart homes, industrial automation, healthcare monitoring, and environmental sensing. Moreover, energy efficiency and environmental sustainability considerations are increasingly influencing the choice of RF components in consumer electronics, infrastructure, and industrial applications. The scalability and configurability of digital RF components support diverse IoT use cases and deployment scenarios, making them an ideal solution for the rapidly evolving consumer electronics market.

Get a glance at the market share of various segments Request Free Sample

The digital components segment was valued at USD 5.09 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

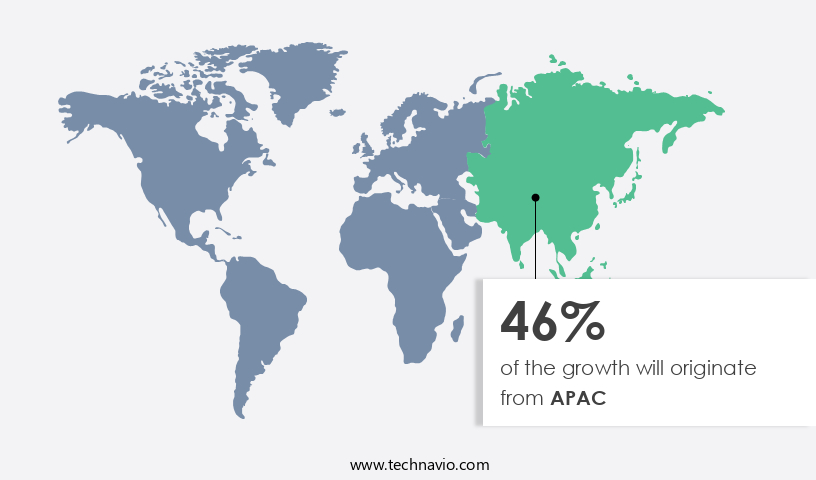

APAC is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the consumer electronics market, driven by the increasing popularity of smartphones, wearables, and audio devices, fuels the demand for RF components such as power amplifiers, filters, and antennas. The shift towards advanced technologies like 5G is further boosting this trend, as telecommunication providers, infrastructure companies, and government agencies invest heavily in network infrastructure expansion. The deployment of 5G networks necessitates the use of high-performance RF solutions for base stations, small cells, antennas, and RF equipment. RF component suppliers in North America stand to benefit significantly from this growing demand, as their products enable seamless connectivity across urban and rural areas.

Moreover, the military and security sectors in North America have unique application zones with stringent security level requirements and regulatory considerations. These sectors require RF components that offer high reliability, long product life, and short lead times for availability. Antennas and transceivers play a crucial role in ensuring secure communication channels in these sectors. As a result, RF component suppliers must prioritize secure design and adherence to industry standards to meet the specific needs of these markets. In summary, the RF components market in North America is witnessing significant growth due to the increasing adoption of consumer electronics, the expansion of 5G networks, and the unique requirements of military and security sectors. RF component suppliers must focus on delivering high-performance, reliable, and secure solutions to meet the evolving needs of these markets.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The emergence of 5G technology is the key driver of the market. The consumer electronics market is witnessing a significant shift towards wireless sensors and IoT technologies, driven by the increasing demand for convenience, energy efficiency, and interoperability. Central hubs for temperature and lighting control, as well as mobile device users' growing reliance on 4G LTE networks, are fueling this trend. In response, the RF components market is experiencing increased demand for components that support these applications. At the heart of this trend is the adoption of 5G technology, which operates at higher frequency bands and requires RF components capable of handling millimeter-wave frequencies. Antenna switches, in particular, are in high demand due to their role in enabling seamless switching between different frequency bands and improving signal quality.

Moreover, to meet the performance targets of 5G-enabled devices, RF components such as filters, amplifiers, and transceivers must be optimized for high-speed data transmission. This includes small, energy-efficient solutions that can be easily integrated into consumer electronics. As consumer spending on technology continues to grow, driven in part by disposable income, the demand for these advanced RF components is expected to remain strong. In summary, the RF components market for consumer electronics is poised for growth due to the increasing adoption of wireless sensors, IoT technologies, and 5G networks. Antenna switches, filters, amplifiers, and transceivers are all key components that must be optimized for high-speed data transmission and energy efficiency to meet the demands of these applications.

Market Trends

Advancements in RF front-end modules (RF FEMs) are the upcoming trends in the market. RF Front-End Modules (FEMs) integrating various RF components, such as power amplifiers, low-noise amplifiers, filters, switches, and antenna tuning circuits, into a single module have gained significant traction in the consumer electronics industry. These integrated solutions offer numerous benefits, including a reduced RF front-end footprint, simplified device design, and enhanced overall performance. The miniaturization of RF FEMs enables manufacturers to create smaller, lighter, and more compact consumer electronic devices.

Additionally, advancements in RF FEM technology have led to modules with higher efficiency, lower power consumption, and improved linearity. These performance enhancements enable better signal reception, transmission, and processing in consumer electronics, resulting in improved wireless connectivity, data rates, and battery life. Moreover, modern consumer electronic devices support multiple wireless standards, including Wi-Fi, Bluetooth, LTE, and 5G. The integration of RF FEMs facilitates the implementation of these standards in a single device, making it a preferred choice for manufacturers.

Market Challenge

Concerns associated with RF interference and spectrum congestion is a key challenge affecting the market growth. RF interference, also known as electromagnetic interference (EMI), is a common issue that affects the performance of electronic devices and communication systems operating in the RF spectrum. This interference can cause degradation in consumer electronic devices, leading to issues with wireless connectivity, data transmission speeds, and signal quality. The increasing use of RF components in devices such as laptops, tablets, smart home accessories, set-top boxes, voice recognition systems, and automotive sector components, among others, exacerbates the problem of RF interference. Spectrum congestion, caused by multiple devices operating on the same frequency bands, further complicates the issue, resulting in decreased reliability and throughput.

In conclusion, consumers demand seamless connectivity and high-performance electronic devices. RF interference can disrupt wireless communication, leading to dropped connections, slow internet speeds, and poor audio/video quality. To mitigate these issues, RF transmission systems and baseband signals must be designed to minimize interference and ensure optimal signal strength. Effective RF management solutions are essential for delivering reliable and high-quality performance in consumer electronics, including music systems, location trackers, navigation systems, central locking systems, automation solutions, and more. By implementing advanced RF filtering techniques, shielding, and other interference mitigation strategies, manufacturers can improve the reliability and performance of their RF components and devices.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Broadcom Inc. - The company offers RF components for consumer electronics, such as advanced RF components for wireless and microwave systems and highly differentiated wireless connectivity solutions for LTE, Wi-Fi, Bluetooth, and GNSS applications.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adolf Wurth GmbH and Co. KG

- Analog Devices Inc.

- Cyrus Audio Ltd.

- Infineon Technologies AG

- Johanson Technology

- Microchip Technology Inc.

- Murata Manufacturing Co. Ltd.

- NXP Semiconductors NV

- Qorvo Inc.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Silicon Laboratories Inc.

- Skyworks Solutions Inc.

- STMicroelectronics International NV

- TAIYO YUDEN Co. Ltd.

- TDK Corp.

- Telefonaktiebolaget LM Ericsson

- Texas Instruments Inc.

- TTM Technologies Inc.

- Yageo Corp.

- Kyocera Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

RF components play a crucial role in the consumer electronics market, powering various applications from mobile handsets to IoT solutions and automotive consumer electronics. With the rise of LTE-advanced, 5G networks, and IoT applications, the demand for RF components has grown. These components are integral to wireless communication technologies such as Bluetooth, Wi-Fi, and cellular phones, enabling mobile internet connectivity and broadband services. The RF technology landscape is vast, encompassing RF engineering, RF spectrum management, and RF components like filters, duplexers, RF amplifiers, RF switches, modulators and demodulators, mixers, and synthesizers. The automotive sector is a significant consumer of RF components, with RF-based vehicle systems offering passenger-oriented functionality, automotive radar, and 5G communication modules.

In summary, the RF components market caters to diverse application zones, including smartphones, smart wearables, home robots, self-driving cars, and satellite communications. The economic downturn has impacted consumer spending, but the interest in wireless technologies remains high. Semiconductors, secure design, and high reliability are essential considerations for RF components, ensuring long product life and availability. The consumer electronics segment, including laptops, tablets, smart home devices, and set-top boxes, is a significant contributor to the RF components market. Rising advances in 4G, 5G, and AI integration have fueled innovation, leading to energy-efficient solutions and interoperability among various devices. The future of RF components lies in enabling seamless wireless connectivity across various applications and industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.06% |

|

Market growth 2024-2028 |

USD 21.12 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.93 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 46% |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Adolf Wurth GmbH and Co. KG, Analog Devices Inc., Broadcom Inc., Cyrus Audio Ltd., Infineon Technologies AG, Johanson Technology, Microchip Technology Inc., Murata Manufacturing Co. Ltd., NXP Semiconductors NV, Qorvo Inc., Qualcomm Inc., Renesas Electronics Corp., Silicon Laboratories Inc., Skyworks Solutions Inc., STMicroelectronics International NV, TAIYO YUDEN Co. Ltd., TDK Corp., Telefonaktiebolaget LM Ericsson, Texas Instruments Inc., TTM Technologies Inc., Yageo Corp., and Kyocera Corp. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -