Semiconductor Capital Equipment Market Size 2024-2028

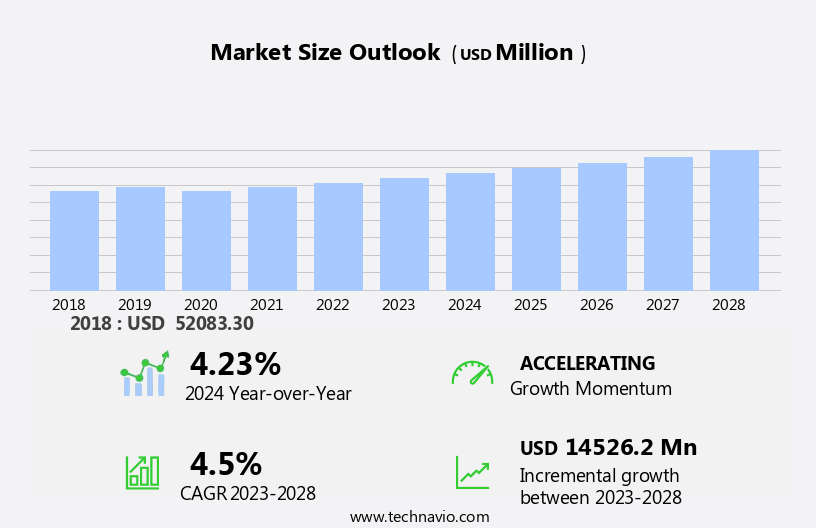

The semiconductor capital equipment market size is forecast to increase by USD 14.53 billion at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing number of semiconductor fabrication plants worldwide. This trend is fueled by the ongoing digital transformation and the rising demand for advanced electronics. Another key factor propelling market growth is the continuous advances in wafer size, leading to increased production efficiency. The semiconductor industry is also witnessing the rise of fixed wireless access and the Internet of Things, leading to an increased demand for wafer fabrication capacity from foundries and memory manufacturers. The semiconductor industry is undergoing significant technological changes, with the adoption of 5G services, AI-machine learning, robotics arms, and automated test equipment. However, the market faces challenges such as the shortage of skilled and trained personnel, which can hinder market growth. This shortage is due to the complex nature of semiconductor manufacturing and the high level of expertise required. To mitigate this challenge, companies are investing in training programs and partnerships with educational institutions to develop a skilled workforce. Overall, the market is poised for continued growth, driven by these market trends and challenges.

What will be the Size of the Semiconductor Capital Equipment Market During the Forecast Period?

- The market is experiencing significant growth due to the increasing demand for advanced electronic devices, such as smartphones and other wireless technology applications. Technological changes, including the adoption of 5G services and the integration of augmented reality and mission-critical services, are driving the need for semiconductor production expansion. Additionally, the integration of cloud computing, digital data, artificial intelligence, and integrated device manufacturers into various industries is fueling the market's growth.

- The panel display and semiconductor chip industries are also experiencing significant advancements, requiring innovative semiconductor production methods and system-level packaging solutions. Overall, the market is poised for continued expansion as technological innovation and the demand for low-cost semiconductors drive growth in various industries.

How is this Semiconductor Capital Equipment Industry segmented and which is the largest segment?

The semiconductor capital equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

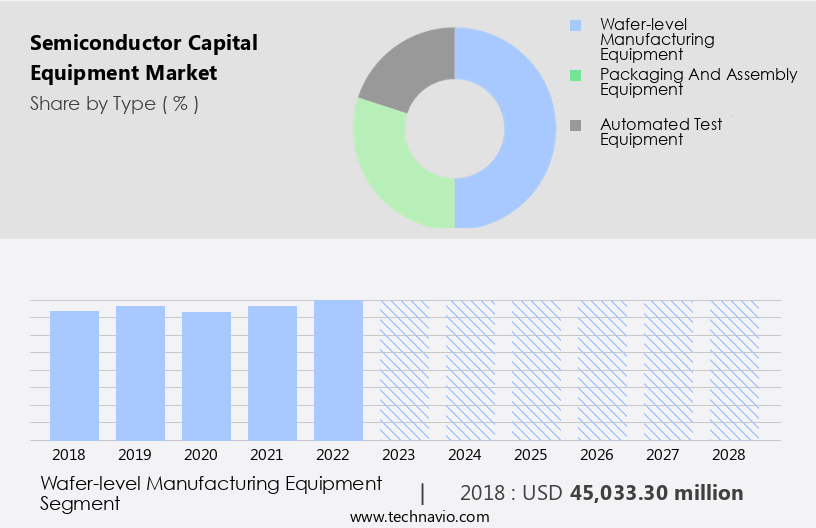

- Wafer-level manufacturing equipment

- Packaging and assembly equipment

- Automated test equipment

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- South America

- Middle East and Africa

- APAC

By Type Insights

- The wafer-level manufacturing equipment segment is estimated to witness significant growth during the forecast period.

Semiconductor manufacturing equipment encompasses front-end processes, such as deposition, lithography/photolithography, photomasking, and etching, which purify silicon wafers for IC production. Wafer processing begins with cutting 640 µm thick wafers from silicon ingots. Subsequently, chemical and mechanical planarization techniques, including polishing, remove surface impurities. Photomasking follows, with IC designs imprinted onto the wafer via photolithography, using a photoresist layer. This equipment is essential for the production of advanced electronic devices, including smartphones, tablets, laptops, wearable devices, machine learning devices, and IoT sensors. Additionally, it supports the manufacturing of industrial screens, advanced processing components, and memory solutions for data centers, automotive sectors, and industrial verticals.

Furthermore, the integration of heterogeneous materials, such as GaN and SiC, and next-generation process nodes, like EUV lithography systems, are driving innovation. Equipment investments are crucial for companies In the technology, medical, IT, telecommunication, and manufacturing industries to remain competitive.

Get a glance at the market report of share of various segments Request Free Sample

The wafer-level manufacturing equipment segment was valued at USD 45.03 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

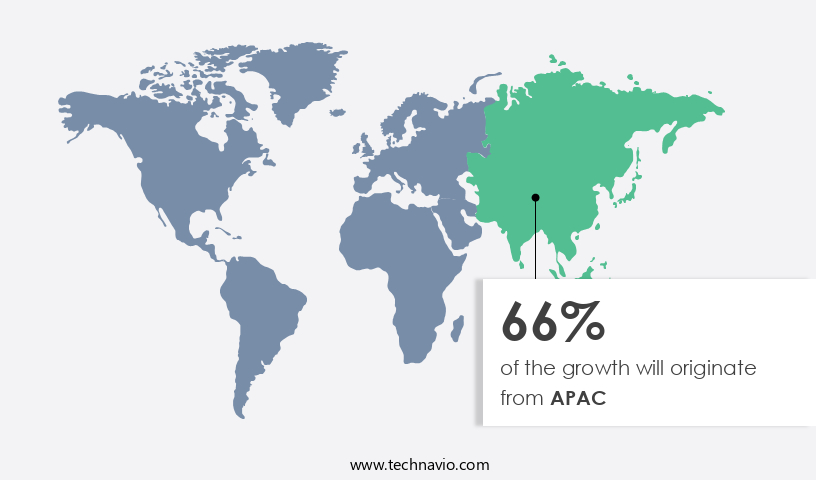

- APAC is estimated to contribute 66% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in APAC is experiencing significant growth, driven by the growth in demand for advanced electronic devices, particularly smartphones, In the region. FinFET technology, a key semiconductor component, is witnessing increased adoption due to its energy efficiency and high performance. In 2023, the demand for semiconductor capital equipment, including wafer processing, surface conditioning, and advanced packaging solutions, increased in APAC to support the production of ICs for smartphones. Chinese smartphone manufacturers, such as Huawei, Lenovo, OnePlus, and OPPO, are leading this growth due to their competitive pricing and high-quality offerings. Furthermore, technological changes, including the adoption of 5G services, wireless technology, and the Internet of Things (IoT), are fueling the demand for semiconductor components in various industries, including consumer electronics, industrial verticals, and data centers.

The technological landscape is evolving rapidly, with emerging trends in areas such as artificial intelligence (AI), machine learning, and automotive electrification. Semiconductor manufacturing investments are expected to continue, driven by the need for advanced processing, etching, ion implantation, wafer back grinding, chemical evaporation, polishing, and other manufacturing processes. Equipment suppliers are responding with new offerings, including AI-machine learning, robotics arms, assembly equipment, automated test equipment, and software solutions for process control and multi-step inspection. The semiconductor industry is also facing challenges, including the global semiconductor crisis and the need for a skilled workforce. Despite these challenges, the future looks bright, with opportunities in areas such as 5G technology, microchips, transistors, copper, and various industrial applications.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Semiconductor Capital Equipment Industry?

The rising number of semiconductors fabs is the key driver of the market.

- The market is experiencing significant growth due to the increasing demand for advanced electronic devices, such as smartphones, tablets, laptops, and wearable devices, driven by technological changes and the adoption of 5G services and wireless technology. The semiconductor industry is also witnessing a growth In the demand for low-cost semiconductors for mission-critical services, industrial verticals, IoT, and digitization. To meet this demand, semiconductor manufacturing is undergoing technological advancements, including the use of AI-machine learning, robotics arms, automated test equipment, and advanced packaging solutions. Wafer processing techniques, such as etching, ion implantation, wafer back grinding, chemical evaporation, polishing, chemical mechanical planarization, chemical vapor deposition, and electronics manufacturing, are essential In the production of semiconductor chips, transistors, and other components.

- The semiconductor market is highly competitive, with companies continually investing in new equipment to maintain a technological edge. The need for high-performance computing, data storage solutions, and sensor market applications is driving the demand for semiconductor production, including foundries and memory manufacturers. Additionally, the automotive sector's electrification and autonomous driving trends, energy efficiency, and smart cities' development require advanced lithography systems and next-generation process nodes, such as EUV lithography systems and GaN, SiC, and advanced lithography. The semiconductor manufacturing landscape is undergoing significant changes, with a focus on semiconductor scaling, heterogeneous integration, system-level packaging, and advanced packaging solutions.

- Equipment suppliers are providing software solutions, process control, multi-step inspection, retrofits, and maintenance services to optimize production and improve efficiency. The global semiconductor crisis highlights the importance of a skilled workforce and the need for continuous innovation and investment in equipment and technology.

What are the market trends shaping the Semiconductor Capital Equipment Industry?

The advances in wafer size is the upcoming market trend.

- The market is experiencing significant technological changes driven by the demand for advanced electronic devices, such as smartphones and tablets, as well as the adoption of 5G services and the Internet of Things (IoT). This shift is leading to increased investments in semiconductor production, particularly In the areas of wafer processing, surface conditioning, and advanced packaging solutions. Key processes, such as etching, ion implantation, wafer back grinding, chemical evaporation, polishing, and chemical mechanical planarization, are essential In the production of semiconductor components, including microchips, transistors, and copper. Moreover, the integration of AI-machine learning, robotics arms, assembly equipment, and automated test equipment is crucial for high-performance computing, data storage solutions, and sensor market applications.

- The semiconductor industry's technological landscape is evolving, with next-generation process nodes, such as EUV lithography systems, GaN, SiC, and advanced lithography, becoming increasingly important. Additionally, the automotive sector's electrification and autonomous driving trends are driving demand for semiconductor components in this industry. Industrial verticals, including data centers, manufacturing processes, and industrial screens, are also significant consumers of semiconductor capital equipment. The medical industry, including medical and healthcare, diagnostic tools, imaging devices, health wearables, and implantable devices, is another growing area for semiconductor components. The semiconductor manufacturing sector requires a skilled workforce and substantial investments in equipment maintenance, retrofits, and software solutions for process control and multi-step inspection.

- The global semiconductor crisis has highlighted the importance of continuous innovation and the need for advanced packaging solutions, such as system-level packaging and heterogeneous integration. Thus, the market is undergoing significant changes, driven by technological advancements and the increasing demand for advanced electronic devices, 5G services, and IoT applications. Companies are investing in larger wafer sizes, such as 300-mm and potentially 450-mm, to cut costs and improve efficiency. The market will continue to evolve, with a focus on advanced processing, energy efficiency, and the development of next-generation process nodes.

What challenges does the Semiconductor Capital Equipment Industry face during its growth?

Shortage of skilled and trained personnel is a key challenge affecting the industry growth.

- The market is experiencing significant changes due to the increasing demand for advanced electronic devices, such as smartphones and tablets, as well as the adoption of 5G services and wireless technology. This technological landscape is driving the need for low-cost semiconductors, advanced processing, and specialized equipment for manufacturing processes, including etching, ion implantation, wafer back grinding, chemical evaporation, polishing, and AI-machine learning. Industrial verticals, including the Internet of Things (IoT), data centers, and industrial screens, are also fueling the demand for semiconductor components and equipment. The digitization of industries and the integration of AI-machine learning, robotics arms, and automated test equipment are essential for manufacturing processes and system-level packaging in advanced packaging solutions.

- Moreover, the semiconductor industry is undergoing scaling and heterogeneous integration, leading to the development of next-generation process nodes, such as EUV lithography systems, and advanced lithography. The automotive sector, with its focus on electrification and autonomous driving trends, is also a significant contributor to the market. The lack of a skilled workforce is a major challenge for the semiconductor manufacturing sector, with the retirement of experienced baby boomers creating a gap In the industry. To address this issue, equipment investments in areas like high-performance computing, data storage solutions, and sensor markets are essential. Additionally, foundries, memory manufacturers, and integrated device manufacturers are investing in semiconductor production and cloud computing to meet the growing demand for digital data and artificial intelligence.

Exclusive Customer Landscape

The semiconductor capital equipment market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the semiconductor capital equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, semiconductor capital equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Fabrication Equipment Inc

- Advantest Corp.

- Applied Materials Inc.

- ASM International NV

- ASML

- Hitachi Ltd.

- II VI Inc.

- KLA Corp.

- Kulicke and Soffa Industries Inc.

- Lam Research Corp.

- Nikon Corp.

- Onto Innovation Inc.

- Planar Systems Inc.

- Screen Holdings Co. Ltd

- Teradyne Inc.

- Tokyo Electron Ltd.

- Tokyo Seimitsu Co. Ltd.

- Veeco Instruments Inc.

- Vicky Electrical Contractors India Pvt. Ltd.

- Voltabox AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing demand for advanced electronic devices and technological changes in various industries. The adoption of wireless technology and 5G services is driving the need for low-cost semiconductors and advanced processing capabilities. The integration of augmented reality and mission-critical services in industries such as telecommunication, medical, and IT is also fueling the market's expansion. The technological landscape is continuously evolving, with digitization and automation becoming essential in manufacturing processes. Semiconductor components are integral to the production of consumer electronics, from smartphones and tablets to laptop computers and wearable devices. In addition, the medical industry is leveraging semiconductors in diagnostic tools, imaging devices, health wearables, and implantable devices.

The semiconductor market is also expanding In the industrial sector, with applications in data centers, automotive, and IoT. The demand for high-performance computing, data storage solutions, and sensor market is driving the need for advanced semiconductor production equipment. Foundries and memory manufacturers are investing in semiconductor production to meet the increasing demand for microchips and transistors. The semiconductor industry is undergoing significant changes, with the focus shifting towards advanced processing techniques such as FinFET, 3D NAND, and EUV lithography systems. Energy efficiency is also a critical factor In the market, with next-generation process nodes and GAA (Gate-All- Around) technologies gaining popularity. The semiconductor manufacturing process involves various stages, including etching, ion implantation, wafer back grinding, chemical evaporation, polishing, and surface conditioning. AI-machine learning, robotics arms, assembly equipment, automated test equipment, and wafer processing equipment are essential in optimizing these stages and ensuring the production of high-quality semiconductors. The semiconductor industry is undergoing a global crisis due to the shortage of skilled workforce and equipment investments.

Equipment maintenance, retrofits, and software solutions are becoming increasingly important to improve process control and efficiency. The market is also witnessing a trend towards system-level packaging and advanced packaging solutions to address the challenges of semiconductor scaling and heterogeneous integration. The automotive sector is a significant consumer of semiconductors, with electrification and autonomous driving trends driving the demand for advanced semiconductor components. The semiconductor industry is also witnessing significant growth In the areas of AI-machine learning devices, smart cities, and smart sensors. Thus, the market is experiencing significant growth due to the increasing demand for advanced electronic devices and technological changes in various industries. The market is undergoing significant changes, with a focus on energy efficiency, advanced processing techniques, and automation. The market is also witnessing a global crisis due to the shortage of skilled workforce and equipment investments, and there is a growing trend towards system-level packaging and advanced packaging solutions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

154 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 14.53 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

South Korea, Taiwan, China, US, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Semiconductor Capital Equipment Market Research and Growth Report?

- CAGR of the Semiconductor Capital Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the semiconductor capital equipment market growth of industry companies

We can help! Our analysts can customize this semiconductor capital equipment market research report to meet your requirements.

RIA -

RIA -